ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

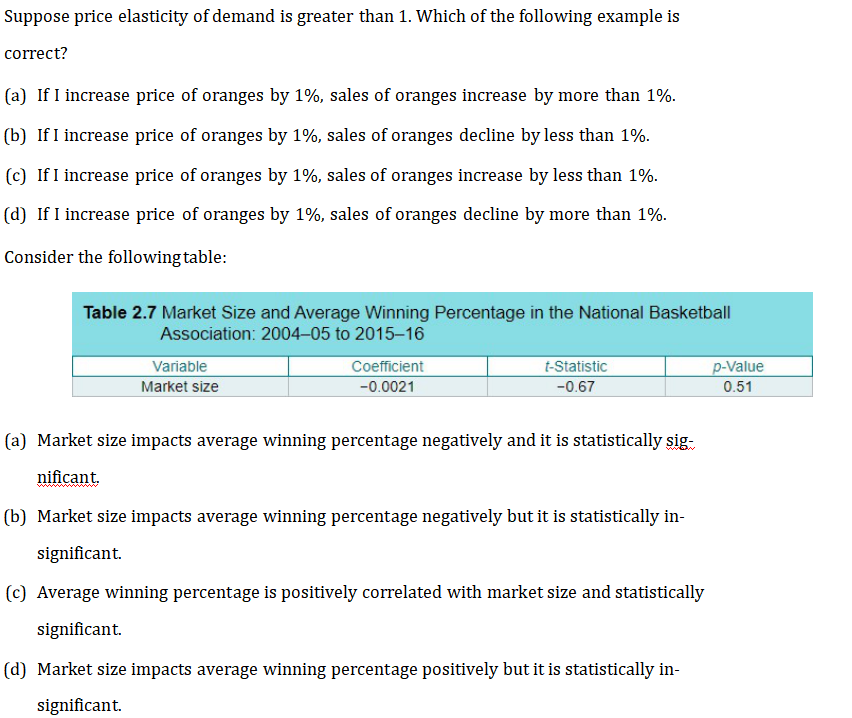

Transcribed Image Text:Suppose price elasticity of demand is greater than 1. Which of the following example is

correct?

(a) If I increase price of oranges by 1%, sales of oranges increase by more than 1%.

(b) If I increase price of oranges by 1%, sales of oranges decline by less than 1%.

(c) If I increase price of oranges by 1%, sales of oranges increase by less than 1%.

(d) If I increase price of oranges by 1%, sales of oranges decline by more than 1%.

Consider the following table:

Table 2.7 Market Size and Average Winning Percentage in the National Basketball

Association: 2004-05 to 2015-16

Variable

Market size

Coefficient

-0.0021

t-Statistic

-0.67

(a) Market size impacts average winning percentage negatively and it is statistically sig

nificant.

(b) Market size impacts average winning percentage negatively but it is statistically in-

significant.

(c) Average winning percentage is positively correlated with market size and statistically

significant.

(d) Market size impacts average winning percentage positively but it is statistically in-

significant.

p-Value

0.51

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- For a good with the following demand: Quantity Demanded Price 6000 $20 14,000 $15 (a) Calculate the price elasticity of demand using the Midpoint Method. (b) Is the demand for this good considered elastic or inelastic? (c) Do you think it is more likely that the average consumer will consider this good a necessity or a luxury? How did you determine your answer? (d) If sellers' production costs rise, will they be able to pass these higher costs onto the buyers in the form of higher prices? Explain.arrow_forwardhi please only help with ( 1 d ) NOTHING ELSEarrow_forwardQuestion 7 It is a rainy day in the village and we are selling Umbrellas. Here is the following data we have on demand. At a sale price of $10, demand is 130 Umbrellas. At a sale price of $12, demand is 110 Umbrellas. (a) Using the percentage method and $10 as your base value, what is the price elasticity of demand for Umbrellas? (b) At a price of $8, by how many dollars would revenue fall by? (c) Would it increase revenue to raise your price to $16?arrow_forward

- 23) Suppose the price elasticity of demand for a product is 1.8. If a supplier wants to increase revenue, they shoud (increase or decrease price- SELECT ONE) increase 24) Goods that are considered luxuries tend to be more (price elastic or price inelastic- SELECT ONE)price elastic 25) When the price is increased and total revenues increase, the elasticity of demand is (price elastic or price inelastic- SELECT ONE)price inelasticarrow_forwardM10arrow_forward5) A certain product has an (own) price elasticity that is elastic, and there is a decrease inthe revenue received. What change in the quantity demanded of a product is necessary to meet theconditions of each situation when there is a 15% increase in the price of that product? Be specific (andsuggest a number).arrow_forward

- (a) Due to the increase in the demand for video games, the equilibrium price of video games increases by 10 percent, and the equilibrium quantity increases by 5 ercent. Is the price elasticity of demand for video games elastic, inelastic, or indeterminate? Explain your answer (with calculation if possible). Is the price elasticity of supply of video games elastic, inelastic, or indeterminate? Explain your answer (with calculation if possible). (b) Suppose Marcus produces chocolate with two inputs: factory and labor. If the workers become more productive with better training, state whether the average fixed cost, average variable cost, average total cost, and marginal cost will rise or fall? (c) After one month of operation, OU Café determined to shorten its business hours and close on weekends. What costs, fixed or variable, should OU Café have considered when it made the dearrow_forwardB. Calculate the price elasticity of demand for large drinks. (Show your work) Last month= $6.00 with 150 quantity This month= $5.50 with 161 quantity Elasticity of demand = Q2-Q1 161/150 divided by (Q1+02) 150+161=311 divided by 2 = 155.5arrow_forwardI need answer typing clear urjent no chat gpt i will give 10 upvotesarrow_forward

- 6) Your income rises from $2,000a year to $10,000 and your purchases of beer change from 10 to 40. What number below most closely approximates your income elasticity over this range? A) 1 B) 1.25 C) 0.75 D) 0.25arrow_forward2. Suppose you have an elasticity of - 2 and the CMg of $ 15.45 per unit. Determine the pricing. CMg (marginal cost)arrow_forwardNonearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education