ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

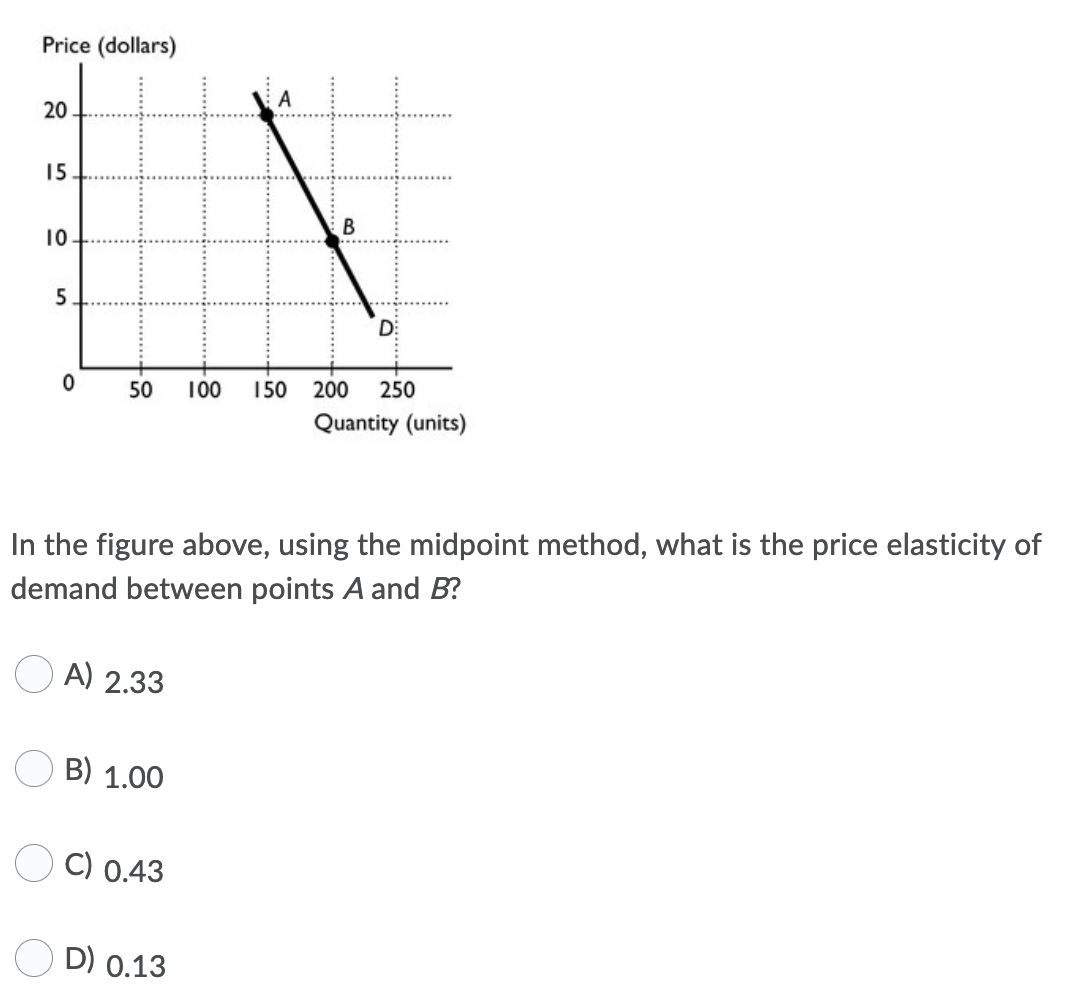

Transcribed Image Text:Price (dollars)

15

B

10

5

D

50

100

150 200

250

Quantity (units)

In the figure above, using the midpoint method, what is the price elasticity of

demand between points A and B?

A) 2.33

B) 1.00

C) 0.43

D) 0.13

20

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- please see the attached1arrow_forwardUsing the table below calculate the cross-price elasticity of flour with respect torice P1 P2 Q1 Q2Flour $9 $12 40 25Rice $4.45 $6.75 150 125arrow_forward11.) In the market for cars, the price elasticity of supply is +1.5, and the price elasticity ofdemand is -0.8. The equilibrium price is $ 30 thousand, and quantity is 120 million.(a) Assuming supply and demand are linear, reconstruct and draw the supply and demandcurves. Label the intercepts.(b) To reduce traffic, the government imposes a $400 tax on cars. What are PB and PS after thetax? What is the new equilibrium quantity? Illustrate them on the same graph.(c) How big is the change in consumer surplus, producer surplus, government revenue, anddeadweight loss?arrow_forward

- only typed solutionarrow_forwardBack to Assignment Keep the Highest 1/2 4. Elastic, inelastic, and unit-elastic demand The following graph shows the demand for a good. Attempts 1 ❖ PRICE (Dollars per unit) 350 225 175 50 0 Region Between W and X Between X and Y Between Y and Z 1 QUANTITY (Units) True False W Demand For each of the regions listed in the following table, use the midpoint method to identify if the demand for this good is elastic, (approximately) unit elastic, or inelastic. Elastic Inelastic Unit Elastic ? True or False: The slope of the demand curve is not equal to the value of the price elasticity of demand.arrow_forwardPoint on Demand Curve: A B C D E F G H I Price (P): $40 $35 $30 $25 $20 $15 $10 $5 $0 Quantity Demanded (QD): 0 5 10 15 20 25 30 35 40 b) Calculate the price elasticity of demand between each set of points on the demand curve (i.e., between A and B, B and C, C and D, D and E, etc.) (c) explain how and why the price elasticity of demand changes as you move along this demand curve. how and why the effect of price changes on total revenue is tied to elasticity.arrow_forward

- If the absolute value of elasticity of demand for chocolate is 0.64 then the demand for chocolate is considered: a. elastic b. inelastic c. unit elastic d. yummy elasticarrow_forwardUsing the midpoint formula and the graph below, calculate the following:i. The price elasticity of demand when the price changes from 9 to 15; andii. The price elasticity of supply when the price changes from $4 to $9arrow_forwardUsing the midpoint method, the price elasticity of demand for jackfruit between point A and point B is approximately. This indicates that demand for jackfruit is between points A and B. The options for the second part are: elastic or inelastic PRICE (Dollars per pound) 3 2 1 12 11 10 B 9 A 8 Demand 0 0 10 20 30 40 50 60 70 80 90 100 110 QUANTITY (Thousands of pounds of jackfruit) Using the midpoint method, the price elasticity of demand for jackfruit between point A and point B is approximately demand for jackfruit is between points A and B. This indicates thatarrow_forward

- the % change in price of spaghetti between prices of $18 and $20 is 10.53. the elasticity of demand between the prices of $18 and $20 is -1.69. So, what is the % change in the quantity of spaghetti when the price changes from $18 to $20?arrow_forwardNonearrow_forwardPrice (dollars per unit) 92 91 90 68 88 D 5 6 7 Quantity (units per day) 2 4 The figure shows a demand curve. Using the midpoint formula, the elasticity of demand moving from point A to point Bequals A) 1.00. B) 0.033. C) 2.00. D) 30arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education