ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

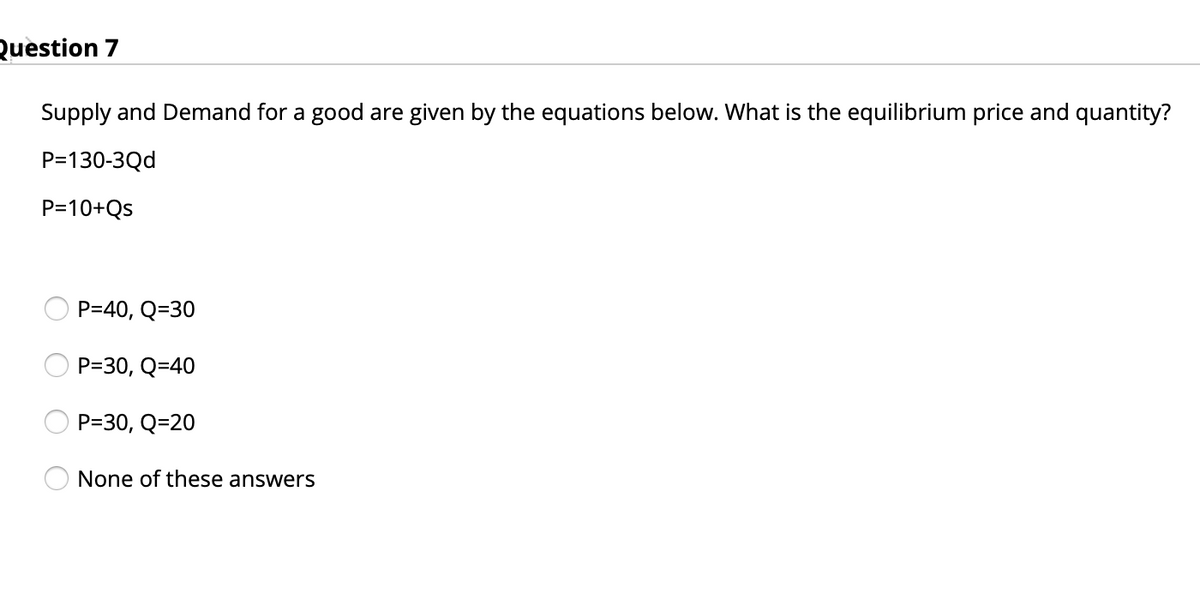

Transcribed Image Text:Question 7

Supply and Demand for a good are given by the equations below. What is the equilibrium price and quantity?

P=130-3Qd

P=10+Qs

P=40, Q=30

P=30, Q=40

P=30, Q=20

None of these answers

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- In the market for hats, demand decreases and supply increases. If you know nothing else about happens in the market for hats, what would you predict would happen to the equilibrium price? The equilibrium price decreases The equilibrium price stays the same The equilibrium price increases There is not enough information to determine how the equilibrium price will changearrow_forwardWhat will happen to Demand(D), Supply(S), new Equilibrium Price(P*), and new Equilibrium Quantity(Q*) when the market condition changes as the following. Explain the reason and draw relevant graphs supporting your analysis. A. Market: Plywood in Florida Event: The Hurricane Center increases the probability of Hurricane to make a landfall in Florida B. Market: Skateboards Event: The price of fiberglass rises (Fiberglass is a substance used for making skateboards) C. Market: Chicken Event 1. Avian flu spreads fast hurting chicken producers AND, simultaneously, Event 2. Beef prices fall a lot, making beef more affordable to consumers (Chicken and beef are substitutes)arrow_forwardSuppose the supply and demand equation are given as follow: Demand: Qd=112-3*p Supply: Qs=22+1*p What's the equilibrium quantity?arrow_forward

- Using the supply and demand functions below, derive the demand and supply curves if Y=$55,000 and pc=$9. What is the equilibrium price and quantity of coffee? Part 2 The demand function for coffee is Q=8.5−p+0.01Y, where Q is the quantity of coffee in millions of pounds per year, p is the price of coffee in dollars per pound, and Y is the average annual household income in high-income countries in thousands of dollars. The coffee supply function is Q=9.6+0.5p−0.2pc, where pc is the price of cocoa in dollars per pound.arrow_forwardEquilibrium Scenarios On a separate piece of paper, use an appropriately labeled supply/demand graph to answer the following questions. For each question, you need to a) state the determinant of demand (TRIPE)/supply (NICEJAG) that caused the change, b) graph the change, and c) tell me what happens to equilibrium price and quantity. 1. What would be the effect of an increase in automobile worker wages on the market for automobiles? 2. What would be the effect of a decline in the price of personal computers on the market for software? 3. What would be the effect of an increase in the price of Budweiser beer on the market for Coors beer? 4. What would be the effect of a governmental subsidy on the market for AIDS research? 5. What would be the effect of a decline in the price of irrigation equipment on the market for corn? 6. What would be the effect of the government subsidizing the growers of watermelons on the market for watermelons? 7. What would be the effect on the market for Big…arrow_forwardSuppose that the demand curve for corn has the equation p = -0.29q+6.265 and the supply curve for corn has the equation p = 0.2q +2.1, where p is the price per bushel in dollars and q is the quantity (demanded or produced) in billions of bushels. (a) Find the quantities supplied and demanded when the price of corn is $3.40 per bushel. (b) Determine the quantity of corn that will be produced and the price at which it will sell. (a) The quantity supplied when the price of corn is $3.40 is (Round to the nearest whole number as needed.) billion bushels.arrow_forward

- Using the supply and demand functions below, derive the demand and supply curves if Y=$55,000 and pc=$13. What is the equilibrium price and quantity of coffee? Part 2 The demand function for coffee is Q=8.5−p+0.01Y, where Q is the quantity of coffee in millions of pounds per year, p is the price of coffee in dollars per pound, and Y is the average annual household income in high-income countries in thousands of dollars. The coffee supply function is Q=9.6+0.5p−0.2pc, where pc is the price of cocoa in dollars per pound. Part 3 The equilibrium price of coffee is p=$enter your response here per pound and the equilibrium quantity is Q=enter your response here millions of pounds per year. (Enter your responses rounded to two decimal places.)arrow_forwardQuestion 33 Consider the following series of shifts in Supply and Demand. Complete the following table, indicating in each of the 9 cells whether equilibrium price and equilibrium quantity go up, down, or stay the same. (Note: To reproduce the table for this question, you may make an exception to the usual 'no cutting and pasting' requirement for this test.) No Change in Supply An Increase in Supply A Decrease in Supply No Change in Demand An Increase in Demand A Decrease in Demandarrow_forwardSuppose that more people have opened their own e-business because they wanted to be their own bosses, but the demand for e-products has grown even faster as the economy recovered from the pandemic. How would this affect the equilibrium price and quantity of meals sold by restaurants? (reperesnt this in graph)arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education