ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

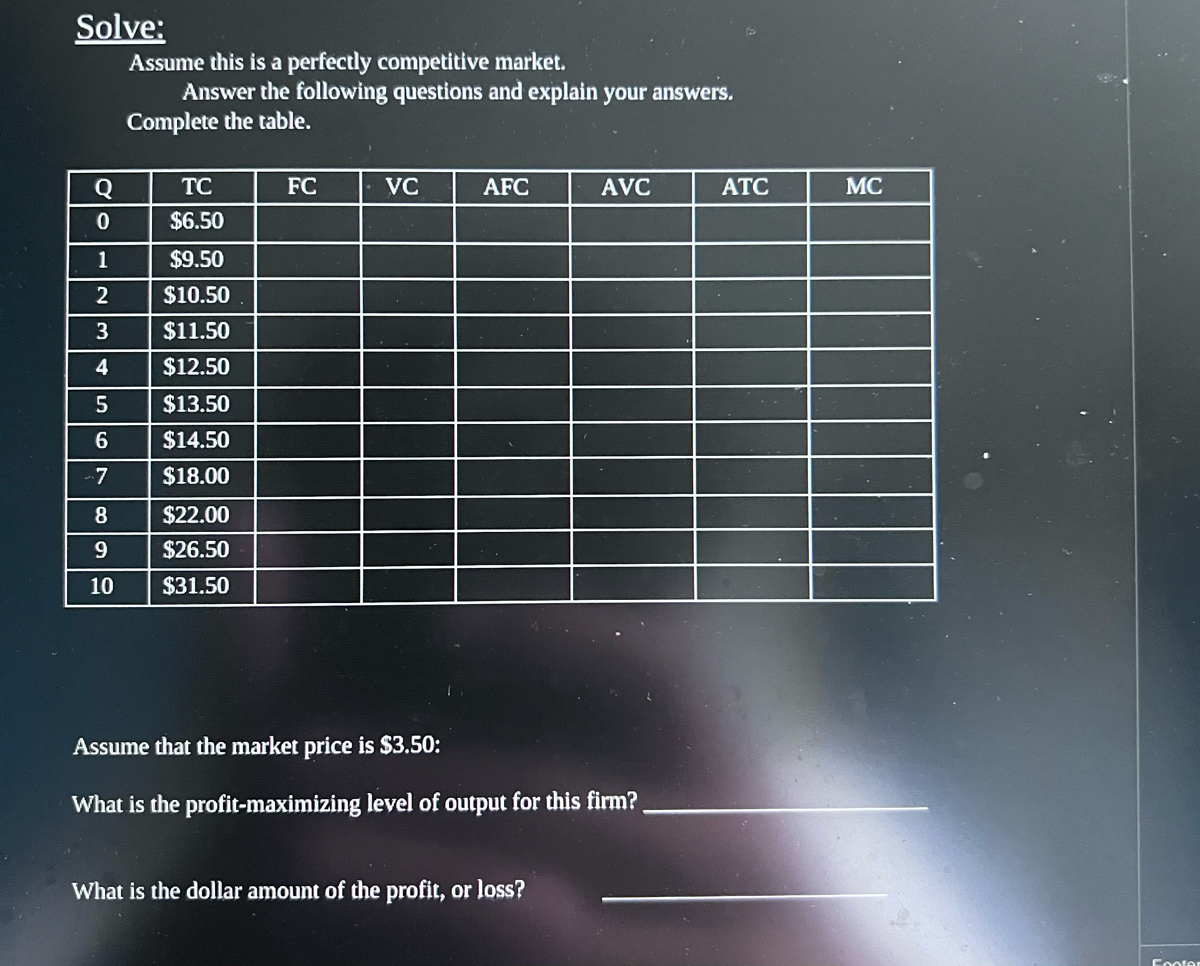

Transcribed Image Text:Solve:

Assume this is a perfectly competitive market.

Answer the following questions and explain your answers.

Complete the table.

Q

TC

FC

VC

AFC

AVC

ATC

MC

0

$6.50

1

$9.50

2

$10.50

3

$11.50

4

$12.50

5

$13.50

67

$14.50

$18.00

8

$22.00

9

$26.50

10

$31.50

Assume that the market price is $3.50:

What is the profit-maximizing level of output for this firm?

What is the dollar amount of the profit, or loss?

Canter

Transcribed Image Text:What would happen with the number of firms in this market if the price drops to $3.00? Why?

What would be the economic profit, or loss, for this firm if the fixed cost increases by $1.50 and

the market price remains at $3.50?

What is the long-run equilibrium price for this company?

What is the shut-down price for this company?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- What are the three conditions for a market to be perfectly competitive? For a market to be perfectly competitive, there must be A. many buyers and sellers, with all firms selling identical products, and no barriers to new firms entering the market. B. many buyers and nothingsellers, with all firms selling identical products, and substantial barriers to new firms entering the market. C. many buyers and sellers, with firms selling similar but not identical products, with low barriers to new firms entering the market. D. many buyers and one seller, with the firm producing a product that has no close substitutes, and barriers to new firms entering the market.arrow_forwardATC MC Z AVC V. W $13 $10 T $7 $4 N 5 7 9 10 12 144 The graph above shows cost curves of a firm in a competitive market. Several points are marked on the graph to allow tracing curves. Some of them can also be used to indicate various prices. Refer to the graph to answer the following questions: 1. The short-run supply of the firm can be traced by connecting points 2. If the market price is $4 then in the short-run the firm would supply units. At this price the firm would 3. If the market price is $10 then in the short-run the firm would supply units. At this price the firm would 4. If the market price is $7 then in the short-run the firm would supply units. At this price the firm would 5. In the short run, the firm is better off continuing to operate (i.e. Q>0) despite losses if the price is in the interval above and below %24arrow_forwardSuppose that the market for polos is a competitive market. The following graph shows the daily cost curves of a firm operating in this market. Esc 50 PRICE (Dollars per polo) 78°F Sunny 45 40 F1 35 30 25 20 15 10 5 0 + 0 + 2 F2 MC -0- + 4 ATC AVC 6 8 10 12 14 QUANTITY (Thousands of polos) F3 0+ F4 69 16 18 F5 20 a F6 i I F7 4- F8 Q+ H F9 F10 FO F11 F12 Fn Lock Insarrow_forward

- Costs and revenue per case 50% a $14 $12 $22 $16 $13 Question 6 Costs and revenue 22 24 30 30 @ 300 The perfectly competitive price would be: MR 22 24 30 3 ATC Demand Quantly (cases) ATC Demand Quantity In the above graph, the firm would earn: $0 in economic profit and break even $44 economic profit $88 economic profit $22 economic loss $44 economic lossarrow_forwardExplain whether a perfectly competitive market is more efficient for buyers to buy or sellers to sell things inarrow_forwardUse the information in the graphs below to answer the following questions SAb $/gal 25- S1 25 H MC ATC 20 20 15 15 P1 10 10 P2 5 4 6 8 10 2. Thousands of gal/week 1 3 Millions of gal/week What is the long-run equilibrium price in this market? Please enter your answers as whole numbers with and do not type out your answer in words (ie. $5 or $5.00 not "Five dollars"). How many gallons per week will the individual firm produce to maximize profits in equilibrium? Please enter your answers as whole numbers with no extra words (ie. 5000 not "5000 gallons/week"). What is the individual firm's long run economic profit?arrow_forward

- 1. Define market power and explain why firms in a perfectly competitive market have none.arrow_forwardFarmer Jones grows sugar. The total revenue, marginal revenue, total cost, and marginal cost of producing various quantities of sugar (bushels in 1000s) are presented in the table below Marginal Output (bushels in 1000s) Total Revenue Marginal Total Revenue Cost Cost 0 $0 0 1 86 86 120 120 2 172 86 200 80 258 86 240 40 344 86 320 80 5 430 86 480 160 516 86 680 200 Suppose the market for sugar is perfectly competitive. To maximize profits, farmer Jones should produce At that level of output, farmer Jones will earn profit of S thousand bushels of sugar. (Enter a numeric response using an integer)arrow_forwardNot use excelarrow_forward

- The figures below show (on the left) two possible demand curves and (on the right) two possible supply curves in the perfectly competitive hamburger market. Price per hamburger 0 A B D₂ D₁ Hamburgers per month Price per hamburger 0 Select one: a. Movement along D₁ from Point A to Point B. b. Demand shifts from D₁ to D₂. F c. Movement along S₁ from Point F to Point G. d. Demand shifts from D₂ to D₁. G Hamburgers per month Assume that people consume either hamburgers or hot dogs. What will be the result of a decrease in the price of hot dogs? Hint: Are hamburgers and hotdogs complements or substitutes? S₂ S₁arrow_forwardNeed help with graphing and understanding problemsarrow_forward8. Refer to the information in the table below to answer the following questions: TVC €0 10 15 Quantity of fruit baskets 0 1 2 3 4 5 6 TFC €50 50 50 50 50 50 50 21 31 46 68 TC MC -- 10 5 6 10 15 22 a) The firm sells fruit baskets in a perfectly competitive market. Calculate the firm's total cost for each level of production and complete the table. b) Assume that the market price of a fruit basket is €15. To maximize profit, how many fruit baskets should the firm sell? c) At the profit-maximizing quantity, what is the profit?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education