FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

answer question 3

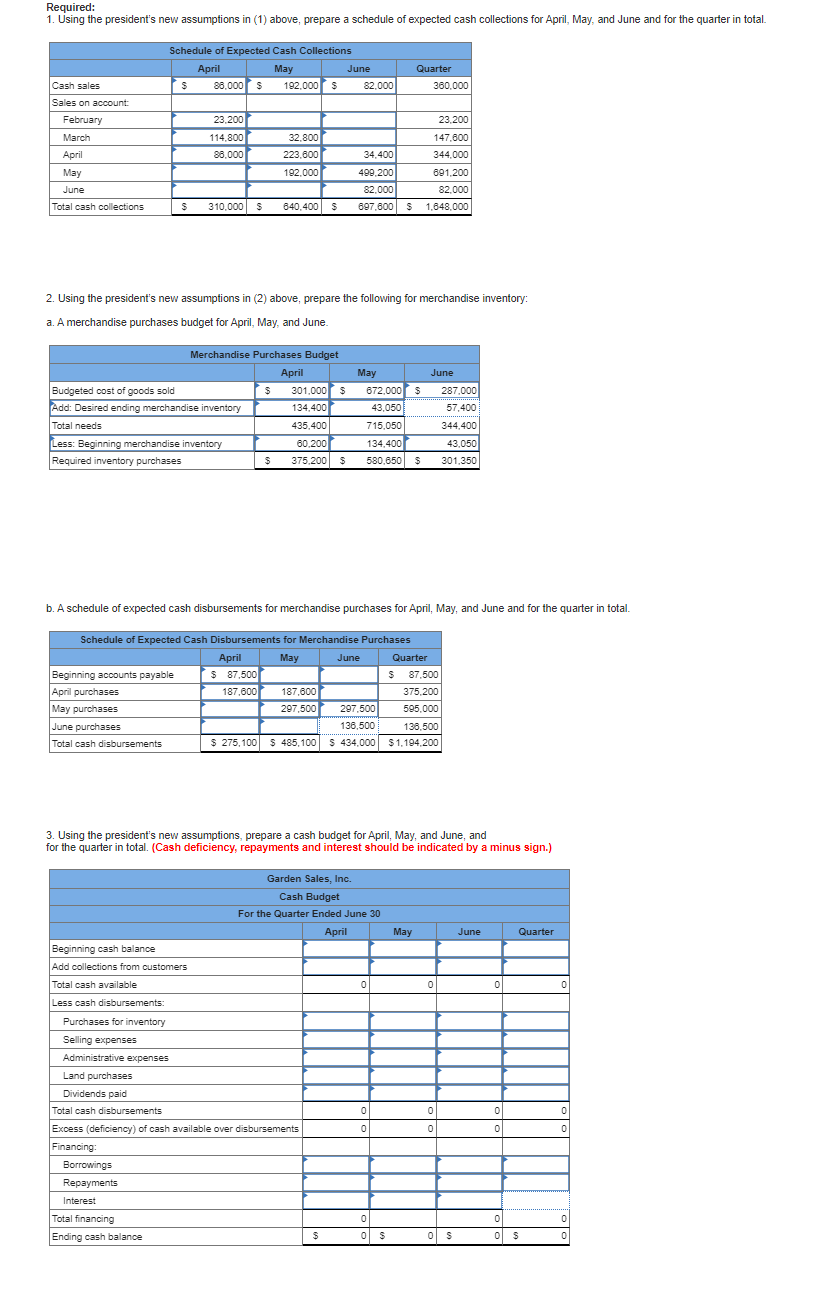

Transcribed Image Text:Required:

1. Using the president's new assumptions in (1) above, prepare a schedule of expected cash collections for April, May, and June and for the quarter in total.

Schedule of Expected Cash Collections

April

May

June

Quarter

Cash sales

88,000 s

192,000s

82,000

360,000

Sales on account:

February

23,200

23,200

32,800

223,600

March

114,800

147,600

April

88.000

34,400

344,000

May

192,000

499,200

691,200

June

82,000

82,000

Total cash collections

310.000 s

640,400 S

697.600 $ 1,648,000

2. Using the president's new assumptions in (2) above, prepare the following for merchandise inventory:

a. A merchandise purchases budget for April, May, and June.

Merchandise Purchases Budget

April

May

June

301.000 $

134,400

287,000

Budgeted cost of goods sold

Add: Desired ending merchandise inventory

672,000

43,050

57,400

Total needs

435,400

715,050

344,400

Less: Beginning merchandise inventory

60,200

134,400

43,050

Required inventory purchases

375,200 S

580,650 $

301,350

b. A schedule of expected cash disbursements for merchandise purchases for April, May, and June and for the quarter in total.

Schedule of Expected Cash Disbursements for Merchandise Purchases

April

May

June

Quarter

Beginning accounts payable

$ 87,500

87,500

187,600

297,500

April purchases

187,600

375,200

May purchases

297,500

595,000

June purchases

136,500

136,500

Total cash disbursements

$ 275, 100

$ S 434,000

$ 485,100

$1,194,200

3. Using the president's new assumptions, prepare a cash budget for April, May, and June, and

for the quarter in total. (Cash deficiency, repayments and interest should be indicated by a minus sign.)

Garden Sales, Inc.

Cash Budget

For the Quarter Ended June 30

April

May

June

Quarter

Beginning cash balance

Add collections from customers

Total cash available

Less cash disbursements:

Purchases for inventory

Selling expenses

Administrative expenses

Land purchases

Dividends paid

Total cash disbursements

Excess (deficiency) of cash available over disbursements

Financing:

Borrowings

Repayments

Interest

Total financing

Ending cash balance

Transcribed Image Text:$ 430,000

301,000

129,000

$ 960,000

672,000

$ 410,000

287,000

123,000

$ 310,000

217,000

93,000

Sales

Cost of goods sold

Gross margin

Selling and administrative expenses:

Selling expense

Administrative expense*

Total selling and administrative expenses

Net operating income

288,000

83,000

40,500

52,000

32,600

84,600

$ 38,400

31,000

29,000

60,000

$ 33,000

91,000

53,600

123,500

5,500

144,600

$ 143,400

*Includes $13,000 of depreciation each month.

b. Sales are 20% for cash and 80% on account.

c. Sales on account are collected over a three-month period with 10% collected in the month of sale; 70% collected in the first month following the month of sale; and the remaining 20% collected in the second month following the

month of sale. February's sales totaled $145,000, and March's sales totaled $205,000.

d. Inventory purchases are paid for within 15 days. Therefore, 50% of a month's inventory purchases are paid for in the month of purchase. The remaining 50% is paid in the following month. Accounts payable at March 31 for inventory

purchases during March total $87,500.

e. Each month's ending inventory must equal 20% of the cost of the merchandise to be sold in the following month. The merchandise inventory at March 31 is $60,200.

f. Dividends of $21,000 will be declared and paid in April.

g. Land costing $29,000 will be purchased for cash in May.

h. The cash balance at March 31 is $43,000; the company must maintain a cash balance of atleast $40,000 at the end of each month.

i. The company has an agreement with a local bank that allows the company to borrow in increments of $1,000 at the beginning of each month, up to a total loan balance of $200,000. The interest rate on these loans is 1% per month

and for simplicity we will assume that interest is not compounded. The company would, as far as it is able, repay the loan plus accumulated interest at the end of the quarter.

The company's president is interested in knowing how reducing inventory levels and collecting accounts receivable sooner will impact the cash budget. He revises the cash collection and ending inventory assumptions as follows:

1. Sales continue to be 20% for cash and 80% on credit. However, credit sales from April, May, and June are collected over a three-month period with 25% collected in the month of sale, 65% collected in the month following sale, and 10%

in the second month following sale. Credit sales from February and March are collected during the second quarter using the collection percentages specified in the main section.

2. The company maintains its ending inventory levels for April, May, and June at 15% of the cost of merchandise to be sold in the following month. The merchandise inventory at March 31 remains $60,200 and accounts payable for

inventory purchases at March 31 remains $87,500.

Required:

1. Using the president's new assumptions in (1) above, prepare a schedule of expected cash collections for April, May, and June and for the quarter in total.

Schedule of Expected Cash Collections

April

May

June

Quarter

Cash sales

$

86,000

$

192,000 $

82,000

360,000

Sales on account:

February

23,200

23,200

March

114,800

32,800

147,600

April

86,000

223,600

34,400

344,000

Мay

192,000

499,200

691,200

June

82,000

82,000

Total cash collections

$

310,000

$

640,400 $

697,600

$

1,648,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 6 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Can you answer part 4arrow_forwardcan you solve by ansewring the question'a in a fromual.arrow_forwardProblem 9-25 Fudge factors An oil company executive is considering investing $10.1 million in one or both of two wells: well 1 is expected to produce oil worth $3.01 million a year for 10 years; well 2 is expected to produce $2.01 million for 15 years. These are real (inflation-adjusted) cash flows. The beta for producing wells is 0.91. The market risk premium is 9%, the nominal risk-free interest rate is 7%, and expected inflation is 3%. The two wells are intended to develop a previously discovered oil field. Unfortunately there is still a 21% chance of a dry hole in each case. A dry hole means zero cash flows and a complete loss of the $10.1 million investment. Ignore taxes and make further assumptions as necessary. a. What is the correct real discount rate for cash flows from developed wells? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Real discount rate b. The oil company executive proposes to add 20 percentage points to the…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education