FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

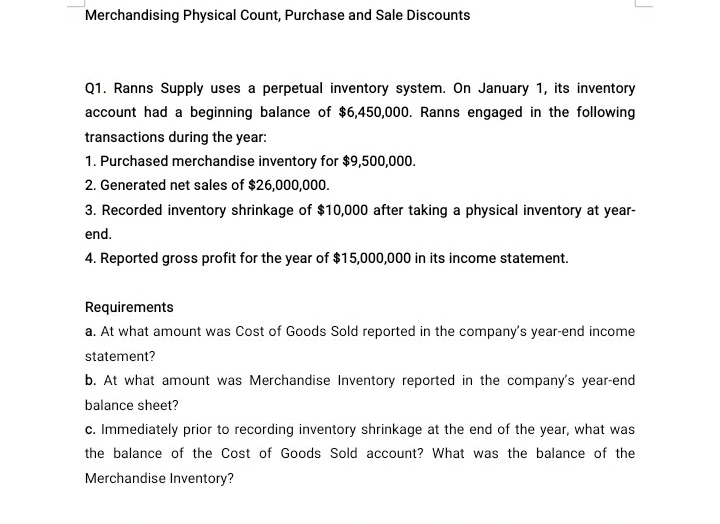

Transcribed Image Text:Merchandising Physical Count, Purchase and Sale Discounts

Q1. Ranns Supply uses a perpetual inventory system. On January 1, its inventory

account had a beginning balance of $6,450,000. Ranns engaged in the following

transactions during the year:

1. Purchased merchandise inventory for $9,500,000.

2. Generated net sales of $26,000,000.

3. Recorded inventory shrinkage of $10,000 after taking a physical inventory at year-

end.

4. Reported gross profit for the year of $15,000,000 in its income statement.

Requirements

a. At what amount was Cost of Goods Sold reported in the company's year-end income

statement?

b. At what amount was Merchandise Inventory reported in the company's year-end

balance sheet?

c. Immediately prior to recording inventory shrinkage at the end of the year, what was

the balance of the Cost of Goods Sold account? What was the balance of the

Merchandise Inventory?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- If a company understates its inventory, what are the effects on cost of goods sold and net income for the current year?arrow_forwardHelp asaparrow_forwardIn recording the cost of goods sold based on data available from perpetual inventory records, the journal entry is a a. debit to Merchandise Inventory and a credit to Cost of Merchandise Sold b. debit to Accounts Receivable and a credit to Merchandise Inventory . debit to Cost of Merchandise Sold and a credit to Sales d. debit to Cost of Merchandise Sold and a credit to Merchandise Inventoryarrow_forward

- Sales revenue Purchases Net income as a percent of sales revenue Beginning inventory Expenses including income taxes Tax rate a. Required a. Prepare the company's single-step income statement. b. Prepare the journal entry at period-end to eliminate beginning inventory and to record ending inventory. Note: Do not use negative signs with your answers. Income Statement Sales revenue Cost of goods sold: Beginning inventory Plus: Purchases Cost of goods available for sale Less: Ending inventory Cost of goods sold Gross margin Expenses Income before taxes Income taxes Net income $ $ $440,000 $308,000 $ 15% $55,000 $99,000 25% 440,000 55,000 308,000 X 0 x 0 x 0 x x 0 x 0 x 0 xarrow_forwardpetermine the gross profit, cost of merchandise sold, and ending inventory on July 31 using the (a) first-in, first-out, (b) last-in, first-out, and (c) average cost flow methods.arrow_forwardIf each purchase and sale of merchandise is recorded in the inventory and the cost of merchandise sold accounts, the method of accounting for merchandise inventory is the: A perpetual method. B) periodic method. C) gross profit method. D) administrative method.arrow_forward

- How do retail companies correctly match expenses with revenue for the period to get an accurate net income? a. With a modern POS system. b. With the consistency principle. c. With a goods-on-hand estimate from the Controller. d. With a physical inventory. According to the Home Depot’s financial statement example provided by the author, which is the predominant method of inventory valuation used by the company? a. FIFO b. LIFO c. NRV d. LCM please provide me a coerrect answer explains tep by steparrow_forward[The following information applies to the questions displayed below.] A company reports inventory using the lower of cost and net realizable value (NRV). Below is information related to its year-end inventory. Inventory Quantity Unit Cost Unit NRV Furniture 170 $ 82 $ 97 Electronics 47 370 285 Record the adjustment for inventory. Note: Enter debits before credits. Transaction General Journal Debit Credit 1 Cost of Goods Sold Inventoryarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education