FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

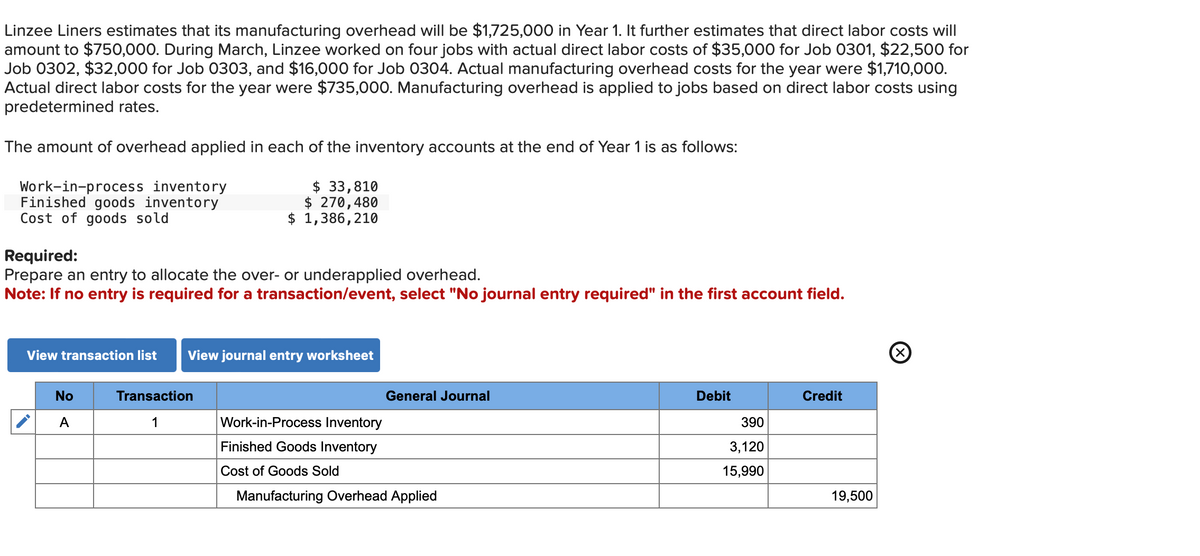

Transcribed Image Text:Linzee Liners estimates that its manufacturing overhead will be $1,725,000 in Year 1. It further estimates that direct labor costs will

amount to $750,000. During March, Linzee worked on four jobs with actual direct labor costs of $35,000 for Job 0301, $22,500 for

Job 0302, $32,000 for Job 0303, and $16,000 for Job 0304. Actual manufacturing overhead costs for the year were $1,710,000.

Actual direct labor costs for the year were $735,000. Manufacturing overhead is applied to jobs based on direct labor costs using

predetermined rates.

The amount of overhead applied in each of the inventory accounts at the end of Year 1 is as follows:

Work-in-process inventory

Finished goods inventory

Cost of goods sold

Required:

Prepare an entry to allocate the over- or underapplied overhead.

Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field.

$ 33,810

$ 270,480

$ 1,386,210

View transaction list View journal entry worksheet

No

A

Transaction

1

General Journal

Work-in-Process Inventory

Finished Goods Inventory

Cost of Goods Sold

Manufacturing Overhead Applied

Debit

390

3,120

15,990

Credit

19,500

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

Transcribed Image Text:Linzee Liners estimates that its manufacturing overhead will be $1,725,000 in Year 1. It further estimates that direct labor costs will

amount to $750,000. During March, Linzee worked on four jobs with actual direct labor costs of $35,000 for Job 0301, $22,500 for

Job 0302, $32,000 for Job 0303, and $16,000 for Job 0304. Actual manufacturing overhead costs for the year were $1,710,000.

Actual direct labor costs for the year were $735,000. Manufacturing overhead is applied to jobs based on direct labor costs using

predetermined rates.

The amount of overhead applied in each of the inventory accounts at the end of Year 1 is as follows:

Work-in-process inventory

Finished goods inventory

Cost of goods sold

Required:

Prepare an entry to allocate the over- or underapplied overhead.

Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field.

No

A

$ 33,810

$ 270,480

$ 1,386,210

Transaction

1

X Answer is not complete.

General Journal

Work-in-Process Inventory

Finished Goods Inventory

Cost of Goods Sold

Manufacturing Overhead Applied

Debit

390

3,120

15,990

Credit

19,500

Solution

by Bartleby Expert

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

Transcribed Image Text:Linzee Liners estimates that its manufacturing overhead will be $1,725,000 in Year 1. It further estimates that direct labor costs will

amount to $750,000. During March, Linzee worked on four jobs with actual direct labor costs of $35,000 for Job 0301, $22,500 for

Job 0302, $32,000 for Job 0303, and $16,000 for Job 0304. Actual manufacturing overhead costs for the year were $1,710,000.

Actual direct labor costs for the year were $735,000. Manufacturing overhead is applied to jobs based on direct labor costs using

predetermined rates.

The amount of overhead applied in each of the inventory accounts at the end of Year 1 is as follows:

Work-in-process inventory

Finished goods inventory

Cost of goods sold

Required:

Prepare an entry to allocate the over- or underapplied overhead.

Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field.

No

A

$ 33,810

$ 270,480

$ 1,386,210

Transaction

1

X Answer is not complete.

General Journal

Work-in-Process Inventory

Finished Goods Inventory

Cost of Goods Sold

Manufacturing Overhead Applied

Debit

390

3,120

15,990

Credit

19,500

Solution

by Bartleby Expert

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Cavy Company estimates that the factory overhead for the following year will be $1,788,000. The company has decided that the basis for applying factory overhead should be machine hours, which is estimated to be 29,800 hours. The machine hours for the month of April for all of the jobs were 4,770. If the actual factory overhead for April totaled $280,190, determine the over- or underapplied amount for the month. Enter the amount as a positive number.arrow_forwardHarris Fabrics computes its plantwide predetermined overhead rate annually on the basis of direct labor-hours. At the beginning of the year, it estimated that 43,000 direct labor-hours would be required for the period's estimated level of production. The company also estimated $537,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $2.00 per direct labor-hour, Harris's actual manufacturing overhead cost for the year was $702,019 and its actual total direct labor was 43,500 hours. Required: Compute the company's plantwide predetermined overhead rate for the year. (Round your answer to 2 decimal places.) Predetermined overhead rate per DLHarrow_forwardCullumber Company estimates that annual manufacturing overhead costs will be $768,000. Estimated annual operating activity bases are: direct labor cost $588,800, direct labor hours 40,000 and machine hours 80,000. The actual manufacturing overhead cost for the year was $769,280 and the actual direct labor cost for the year was $583,680. Actual direct labor hours totaled 39,800 and machine hours totaled 79,000. Cullumber applies overhead based on direct labor hours. Compute the predetermined overhead rate and determine the amount of manufacturing overhead applied. Determine if overhead is over- or underapplied and the amount. (Round predetermined overhead rate to 2 decimal places, e.g. 15.25 and all other answers to O decimal places, e.g. 1,525.) Predetermined overhead rate $ Manufacturing overhead applied $ $ per direct labor hourarrow_forward

- Richey Company uses an actual cost accounting system that applies overhead on the basis of direct labor hours. At the beginning of the year, management estimated that during the year, the company would work 26,000 direct labor hours and budgeted $1,300,000 for MOH. The company actually worked 24,000 direct labor hours and incurred the following actual manufacturing costs: Direct materials used in production $1,240,000 Direct labor 1,800,000 Indirect labor 300,000 Indirect materials 220,000 Insurance 150,000 Utilities 190,000 Repairs and Maintenance 180,000 Depreciation 320,000 Determine the amount of underapplied or overapplied overhead for the year.arrow_forwardThe Vinta Company estimates its factory overhead for the next period at P2,500,000. It is estimated that 40,000 units will be produced at a material costs of P1,600,000 and will require 100,000 direct labor hours at an estimated cost of P2,500,000. The machine will run about 320,000 hours. What is the predetermined factory overhead rate based on direct labor cost? * P7.8125 156.25% 100.00% O P25.00 O P62.50arrow_forwardDelph Company uses job-order costing with a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, the company estimated that 54,000 machine-hours would be required for the period’s estimated level of production. It also estimated $1,000,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $4.00 per machine-hour. Because Delph has two manufacturing departments—Molding and Fabrication—it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following information to enable calculating departmental overhead rates: Molding Fabrication Total Machine-hours 23,000 31,000 54,000 Fixed manufacturing overhead cost $ 760,000 $ 240,000 $ 1,000,000 Variable manufacturing overhead cost per machine-hour $ 4.00 $ 1.00 During the year, the company had no beginning or ending inventories and it started,…arrow_forward

- Harris Fabrics computes its plantwide predetermined overhead rate annually on the basis of direct labor-hours. At the beginning of the year, it estimated that 20,000 direct labor-hours would be required for the period’s estimated level of production. The company also estimated $94,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $2.00 per direct labor-hour. Harris's actual manufacturing overhead cost for the year was $123,900 and its actual total direct labor was 21,000 hours. Required: Compute the company's plantwide predetermined overhead rate for the year. Note: Round your answer to 2 decimal places.arrow_forwardCavy Company estimates that the factory overhead for the following year will be $2,829,000. The company has determined that the basis for applying factory overhead will be machine hours, which is estimated to be 34,500 hours. There are 4,690 machine hours for all of the jobs in the month of April. What amount will be applied to all of the jobs for the month of April?arrow_forwardDelph Company uses job-order costing with a plantwide predetermined overhead rate based on machine-hours. At the beginning of the year, the company estimated that 54,000 machine-hours would be required for the period's estimated level of production. It also estimated $1,040,000 of fixed manufacturing overhead cost for the coming period and variable manufacturing overhead of $5.00 per machine-hour. Because Delph has two manufacturing departments-Molding and Fabrication-it is considering replacing its plantwide overhead rate with departmental rates that would also be based on machine-hours. The company gathered the following information to enable calculating departmental overhead rates: Machine-hours Fixed manufacturing overhead cost Variable manufacturing overhead cost per machine-hour Job D-70 Direct materials cost Direct labor cost Machine-hours Job C-200 Direct materials cost Direct labor cost Machine-hours During the year, the company had no beginning or ending inventories and it…arrow_forward

- Captain Pickles Pet Products computes its predetermined overhead rate annually on the basis of direct labor hours. At the beginning of the year, it estimated that 40,000 direct labor-hours would be required for the period’s estimated level of production. The company also estimated P586,000 manufacturing overhead expenses for the coming period. Captain Pickles’s actual manufacturing overhead for the year was P713,400 and its actual total direct labor was 41,000 hours. Compute the company’s predetermined overhead rate for the year. P14.29 per direct labor hour P14.65 per direct labor hour P17.84 per direct labor hour P17.40 per direct labor hourarrow_forwardWinston Company estimates that total factory overhead for the following year will be $1,347,500. The company has decided that the basis for applying factory overhead should be machine hours, which are estimated to be 38,500 hours. The actual total machine hours for the year were 54,300 hours. The actual factory overhead for the year was $1,927,000. Enter the amount as a positive number. a. Determine the total factory overhead applied. Round to the nearest dollar. b. Compute the over- or underapplied factory overhead for the year. c. Journalize the entry to transfer the over- or underapplied factory overhead to cost of goods sold. If an amount box does not require an entry, leave it blank.arrow_forwardhe Thomlin Company forecasts that total overhead for the current year will be $11,385,000 with 164,000 total machine hours. Year to date, the actual overhead is $7,616,000 and the actual machine hours are 93,000 hours. If the Thomlin Company uses a predetermined overhead rate based on machine hours for applying overhead, as of this point in time (year to date), the overhead is Round the factory overhead rate to the nearest dollar before multiplying by the number of hours.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education