Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

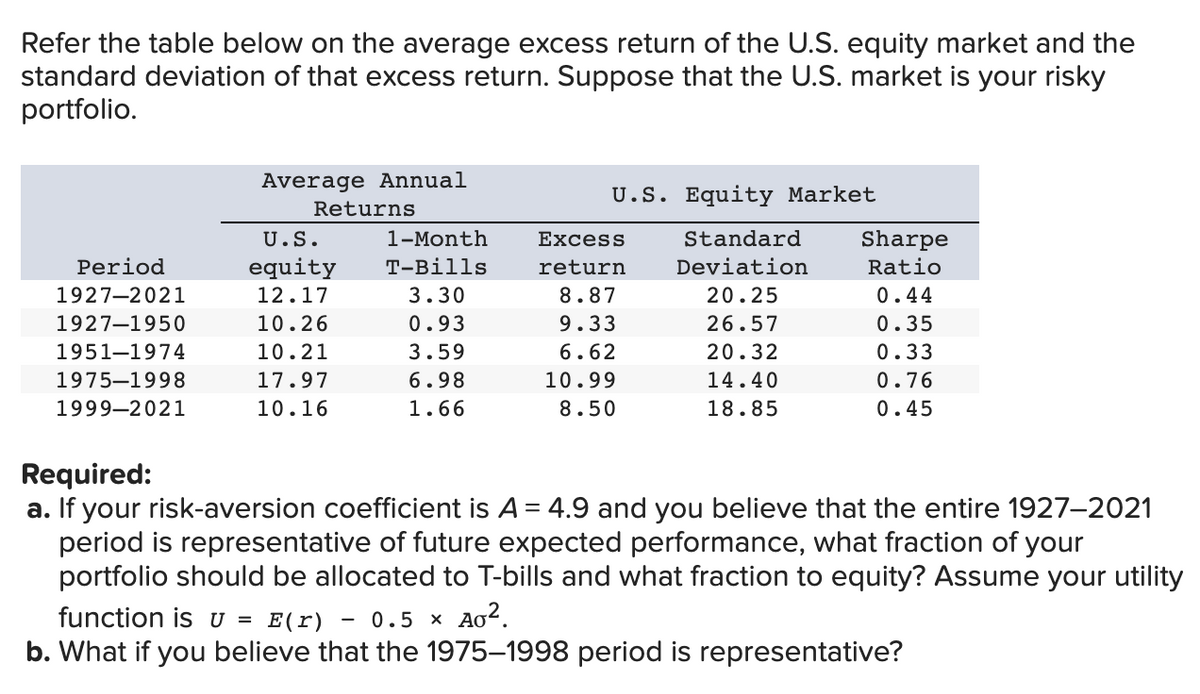

Transcribed Image Text:Refer the table below on the average excess return of the U.S. equity market and the

standard deviation of that excess return. Suppose that the U.S. market is your risky

portfolio.

Period

1927-2021

1927-1950

1951-1974

1975-1998

1999-2021

Average Annual

Returns

U.S.

equity

12.17

10.26

10.21

17.97

10.16

1-Month

T-Bills

3.30

0.93

3.59

6.98

1.66

U.S.

Excess

return

8.87

9.33

6.62

10.99

8.50

Equity Market

Standard

Deviation

20.25

26.57

20.32

14.40

18.85

Sharpe

Ratio

0.44

0.35

0.33

0.76

0.45

Required:

a. If your risk-aversion coefficient is A = 4.9 and you believe that the entire 1927-2021

period is representative of future expected performance, what fraction of your

portfolio should be allocated to T-bills and what fraction to equity? Assume your utility

function is u = E(r) 0.5 × Ao².

b. What if you believe that the 1975-1998 period is representative?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- 4. Explain what the Capital Asset Pricing Model (CAPM) is and calculate and explain the result of the CAPM based on the following data. a. Expected Return: 8% b. Risk-free rate: 4% c. Beta of the investment: 1.2 ER=Rf+B(ERm - Rf) where: ER = expected return of investment Rf risk-free rate B;= beta of the investment - (ERm - Rf) = market risk premiumarrow_forwardWhat is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation (SDi), covariance (COVij), and asset weight (Wi) are as shown below? Asset (A) E(R₂) = 25% SDA = 18% WA = 0.75 COVA, B = -0.0009 Select one: A. 13.65% B. 20 U ODN 20.0% C. 18.64% D. 22.5% Asset (B) E(R₂) = 15% SDB = 11% WB = 0.25arrow_forwardAssume a utility function of ? = ?[?] − 1 ?? 2. Which statement(s) is/are correct about investors with this utility function? [I] An investor with a higher degree of risk aversion chooses the optimal portfolio with a higher risk premium [II] An investor with a higher degree of risk aversion chooses the optimal portfolio with lower risk [III] An investor with a higher degree of risk aversion chooses the optimal portfolio with a higher sharpe ratio [IV] The extent to which the investor dislikes risk is captured by ? 2 A. [II] only B. [I], [II] only C. [III] , [IV] only D. [II], [IV] only E. [I], [II], [III] onlyarrow_forward

- If you plot the relationship between portfolio expected return and portfolio beta, what is the slope of the line that results? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) | Slope of the line %arrow_forwardDraw the profit diagram of the portfolio just drawn (and clearly state any assumptions you make). The profit is equal to the difference between the payoff of the portfolio at expiry (maturity) date and the cost of the portfolio. Is the cost of the portfolio positive?arrow_forwardSuppose the utility function is U = E(r) - 0.5Ao2. Draw the indifference curve corresponding to a utility level of 0.2 for an investor with a risk aversion coefficient of 3. Please note the vertical line indicates expected return, and plot standard deviation on the horizontal line.arrow_forward

- Bhagiarrow_forwardWhen, if ever, will the geometric average return exceed the arithmetic average return for a given set of returns? Never When the set of returns includes only risk-free rates. When all of the rates of return in the set of returns are equal to each other.arrow_forwardSuppose you have an investment portfolio with fraction x invested in a market portfolio and (1-x) in a risk- free asset. Increasing fraction x invested in the market portfolio and consequently decreasing (1-x) invested in the risk-free asset shall (select any correct answer, if there are multiple correct answers) Select one or more: O decrease the Sharpe ratio of the resulting portfolio O decrease the expected return of the resulting portfolio increase the Sharpe ratio of the resulting portfolio increase the expected return of the resulting portfolio Dincrease the risk of the resulting portfolioarrow_forward

- need helparrow_forward2. The following table gives information on the return and variance of assets A and B, whose covariance is 0.0003: A B 0} 0,0009 0,0012 E (R₂) 0,05 0,06 a. Does the portfolio (1/3 of A and 2/3 of B) dominate the portfolio (2/3 of A and 1/3 of B)? b. Does the portfolio (1/2, 1/2) belong to the efficient frontier? c. If there were the possibility of lending and borrowing at 2%, would the portfolio (1/2, 1/2) belong to the new efficient frontier?arrow_forwardCalculate the optimal risky portfolio for the following cases when short-sales are allowed. Compute its expected return and the standard deviation of its returns. 1. Two risky assets: Rp = 3, R' = [6, 9], and 4 5 5 20 2. Three risky assets: Rp = 4, R' = [5,9, 8], and [10 0 0 E=0 40 0 0 20 3. Three risky assets: Rp = 5, R' = [12, 9, 8], and 40 10 -5] E= 10 20 0 5 0 30 4. Five risky assets: Rp = 2, R' = [5, 3, 18, 9, 2], and %3D 2 16 0. -12 5 -12 20 16 10 7 14 27 14 9. -13 8. 7 27 13arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education