Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:11

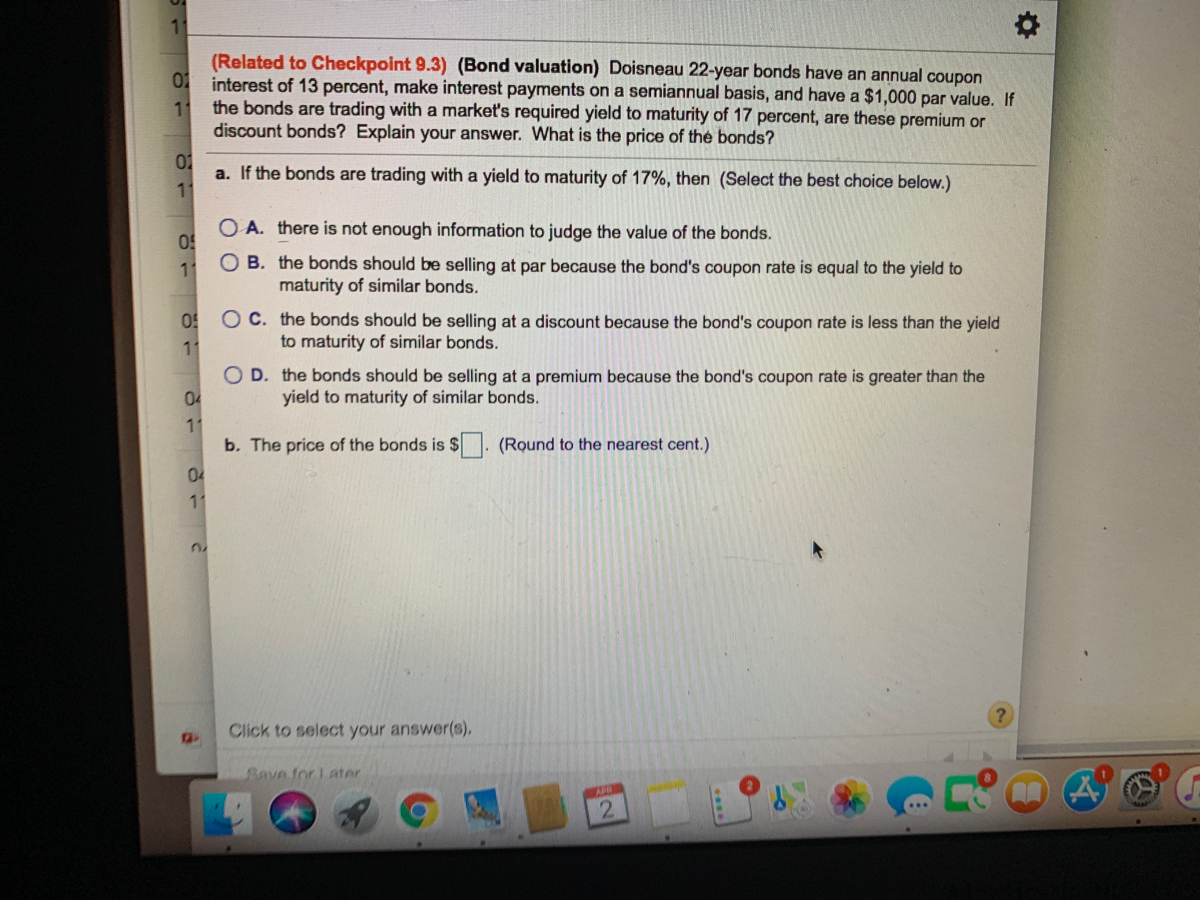

(Related to Checkpoint 9.3) (Bond valuation) Doisneau 22-year bonds have an annual coupon

01

interest of 13 percent, make interest payments on a semiannual basis, and have a $1,000 par value. If

11

the bonds are trading with a market's required yield to maturity of 17 percent, are these premium or

discount bonds? Explain your answer. What is the price of the bonds?

01

a. If the bonds are trading with a yield to maturity of 17%, then (Select the best choice below.)

11

O A. there is not enough information to judge the value of the bonds.

O B. the bonds should be selling at par because the bond's coupon rate is equal to the yield to

maturity of similar bonds.

11

O! O C. the bonds should be selling at a discount because the bond's coupon rate is less than the yield

11

to maturity of similar bonds.

O D. the bonds should be selling at a premium because the bond's coupon rate is greater than the

yield to maturity of similar bonds.

11

b. The price of the bonds is $. (Round to the nearest cent.)

04

11

Click to select your answer(s),

Save for L ater

APR

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You are considering an investment in 20-year bonds issued by Moore Corporation. The bonds have no special covenants. The Wall Street Journal reports that 1-year T - bills are currently earning 0.50 percent. Your broker has determined the following information about economic activity and Moore Corporation bonds:Real risk-free rateDefault risk premiumLiquidity 0.41% = 1.05 % = 0.90% = 0.75% risk premiumMaturity risk premium = a. What is the inflation premium?b. What is the fair interest rate on Moore Corporation 20-year bonds?arrow_forward9. Interest Rate Risk. Suppose that you are a fixed income portfolio manager at Bourbon Street Capital. You have the following bonds issued by Royal, Inc. and Chartres, LLC in your portfolio and you want to understand the risk profile of your portfolio. Given that both bonds pay semiannual coupons, answer the following questions. (Remember to convert your answer to units of full years.) Coupon Yield to maturity Maturity (years) Royal, Inc. Chartres, LLC. Bond A Bond B 9% 8% 5 $100.00 $104.055 8% 8% 2 Par $100.00 Price $100.00 (a) What is the DV01 (at current prices) for bonds A and B? (b) What are the Macaulay Durations (at current prices) for the two bonds? (c) What are the modified durations for the two bonds? (d) What is the convexity of the two bonds?arrow_forwardDoisneau20-year bonds have an annual coupon interest of8 percent, make interest payments on a semiannual basis, and have a $1,000par value. If the bonds are trading with a market's required yield to maturity of18 percent, are these premium or discount bonds? Explain your answer. What is the price of the bonds?arrow_forward

- A plot of the yields on bonds with different terms to maturity but the same risk, liquidity, and tax considerations is known as O A. a yield curve. B. a risk-structure curve. OC. a term-structure curve. 5- O D. an interest-rate curve. Suppose people expect the interest rate on one-year bonds for each of the next four years to be 3%, 6%, 5%, and 6%. If the expectations theory of the term structure of interest rates is correct, then the implied interest rate on bonds with a maturity of four years is nearest whole number). %. (Round your response to the 2- Refer to the figure on your right. Suppose the expected interest rates on one-year bonds for each of the next four years are 4%, 5%, 6%, and 7%, respectively. 1. 1.) Use the line drawing tool (once) to plot the yield curve generated. 3 Term to Maturity in Years 2.) Use the point drawing tool to locate the interest rates on the next four years. 5. 3- Interest Rate .....arrow_forwardConsider two types of bonds: A 10 year to maturity corporate bond and a 10 year to maturity Treasury bond. We know that Corporate Bonds have default risk. Discuss the impact on the markets for these two type of bonds & on the risk premium when there is a FALL in the risk of corporate default? Provide a DISCUSSION of the impact and ILLUSTRATE the impact graphically using two diagrams, one for corporate bonds and one for Treasuries. The diagrams should show the impact on each yield and the impact on the risk premium [label your diagram clearly to illustrate the old premium vs. the new premium]. hint: draw your diagrams side by side, so you can show the risk premiums as done in lecture.arrow_forwardam. 49.arrow_forward

- A BBB-rated corporate bond has a yield to maturity of 9.8%. A U.S. Treasury security has a yield to maturity of 8.4%. These yields are quoted as APRS with semiannual compounding. Both bonds pay semiannual coupons at an annual rate of 9.1% and have five years to maturity. a. What is the price (expressed as a percentage of the face value) of the Treasury bond? b. What is the price (expressed as a percentage of the face value) of the BBB-rated corporate bond? c. What is the credit spread on the BBB bonds? a. What is the price (expressed as a percentage of the face value) of the Treasury bond? The price of the Treasury security as a percentage of face value is ☐ %. (Round to two decimal places.)arrow_forward(Related to Checkpoint 9.2 and Checkpoint 9.3) (Bond valuation) The 11-year $1,000 par bonds of Vail Inc. pay 14 percent interest. The market's required yield to maturity on a comparable-risk bond is 11 percent. The current market price for the bond is $1,100. a. Determine the yield to maturity. b. What is the value of the bonds to you given the yield to maturity on a comparable-risk bond? c. Should you purchase the bond at the current market price? Question content area bottom Part 1 a. What is your yield to maturity on the Vail bonds given the current market price of the bonds? enter your response here% (Round to two decimal places.) Part 2 b. What should be the value of the Vail bonds given the yield to maturity on a comparable risk bond? $enter your response here (Round to the nearest cent.) Part 3 c. You ▼ should should not purchase the Vail bonds at the current market price because they are currently ▼ underpriced…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education