ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

{kind=link}

Question

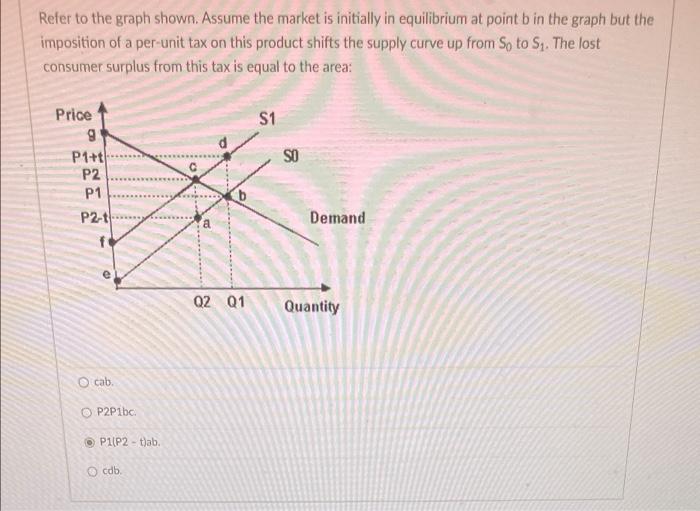

Transcribed Image Text:Refer to the graph shown. Assume the market is initially in equilibrium at point b in the graph but the

imposition of a per-unit tax on this product shifts the supply curve up from So to S1. The lost

consumer surplus from this tax is equal to the area:

Price

S1

P1+t

SO

P2

P1

P2-t

Demand

Q2 Q1

Quantity

O cab.

O P2P1bc.

P1(P2 - tjab.

O cdb.

O- .........

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The figure shows the market for buckets of golf balls at the driving range. A new leisure time tax is placed on suppliers in this market, shifting the supply curve from So to S₁. The amount of this tax per bucket of golf balls. IS QA. $2 OB. $2.50 O C. $4 OD. $1 OE. $3arrow_forwardPlease give me detail answerarrow_forwardThe following questions pertain to analysis of the supply and demand scenario derived from the schedules below: Candy Canes QD QS 20 2. 14 14 21 4 28 Create a graph of the supply and curves from this chart for use in your analysis. 19. What would be the result of a government-imposed price celling orn candy canes set at the price of 1 dollar? O a A surplus of candy canes would occur, and this is evident because of the quantity of candy canes supplied at the price of 1 dollar is much greater than the quantity of candy canes demanded. A shortage of candy canes would occur, and this is evident because the quantity of candy canes d is much greater than the quantity of candy canes supplied. There would be no result. The price ceiling is set above equilibrlum and is therefore not binding. O b ...arrow_forward

- Suppose the market for a product is given by the following S+D functions. price 100 80 60 40 20 20 Demand 40 60 80 100 120 140 How much DWL does a $10 tax create? O a. zero Ob. 200 O c. 600 O d. 400 Supplyarrow_forward1. Consider a market where the demand is given by Q = 120 –P and supply is %3D given by QS = P. What are the consumer and producer surplus? Р. %3D a) Consumer surplus is 120 arnd producer surplus is 600. b) Consumer surplus is 600 and producer surplus is 1200. c) Consumer surplus is 240 and producer surplus is 300. d) Consumer surplus is 1200 and producer surplus is 240.arrow_forwardUsing Supply and Demand to Analyze Markets-End of Chapter Problem Increases in demand generally result in increases in consumer surplus. However, this is not always the case. Of the following scenarios, which one is most likely to result in a decrease in consumer surplus? Supply is relatively elastic, and demand becomes highly inelastic when it increases. Supply and demand are both unit elastic and demand increases. Supply is inelastic, and demand becomes highly elastic when it increases. O Supply is relatively elastic, and demand becomes highly elastic when it increases.arrow_forward

- l Verizon 10:55 PM ncuone.ncu.edu Instructions Assume that the City Council in Prescott, Arizona is considering implementing price ceilings on rental units based on the number of bedrooms in the unit. The demand function for rental units (on a single bedroom equivalent basis) is given by Qp = 120 – 4P and the supply function is given by Qs = 2P, where P is price and Q is quantity. The Council is considering imposing a ceiling price on rental units of Pmax = 16. 1. Using the given functions, draw a corresponding demand curve and a supply curve. Properly label the equilibrium price and quantity. Then show what will happen to equilibrium if the City Council imposes a price ceiling at 16. NOTE: There are numerous guides online that demonstrate how to draw supply and demand curves; most are done in Excel. To create the demand curves that you need for this assignment, create an Excel file with a price column, including prices from $1 to $30. Using the formulas, compute the quantity demanded…arrow_forwardDROP OFF BU rEDAY @UPM 27 9. DEADWEIGHT LOSS WITH PRICE CONTROLS If an equilibrium position is less than perfectly efficient, the loss in total surplus (CS + PS) is termed "deadweight loss." If D and S are linear, then DWL is measured as the area a triangle, the "loss triangle." The area of a triangle is half of (base X height). > Suppose that demand and supply equations in a competitive market are: Demand: P = 30 – 0.6Q Supply: P = 6 + 0.4Q a. Compute the market equilibrium. (Q*, P*) = ( b. Calculate consumer surplus and producer surplus at the market equilibrium. Producer surplus (PS) is the area above the supply curve and below the price. CS* = PS* = C. Suppose that a price floor of Pr = 24 is imposed by the government. Find the equilibrium quantity with the price floor. Then calculate consumer surplus, producer surplus, and deadweight loss at the regulated equilibrium. CSt = PS = DWL =arrow_forwardConsider a market where demand and supply satisfy the following equationsQd = 12 – 2 P,QS = 2P.a)Find the current equilibrium price and quantity. b)What is the total producer surplus if the market is in equilibrium? The government is considering a minimum price policy to increase producer surplus.c)Explain by means of graphs how the introduction of a price floor can increase producer surplus. d)Find the (optimal) price floor that maximizes producer surplus. hi, can you answer part c and part d for this question please, thanksarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education