ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

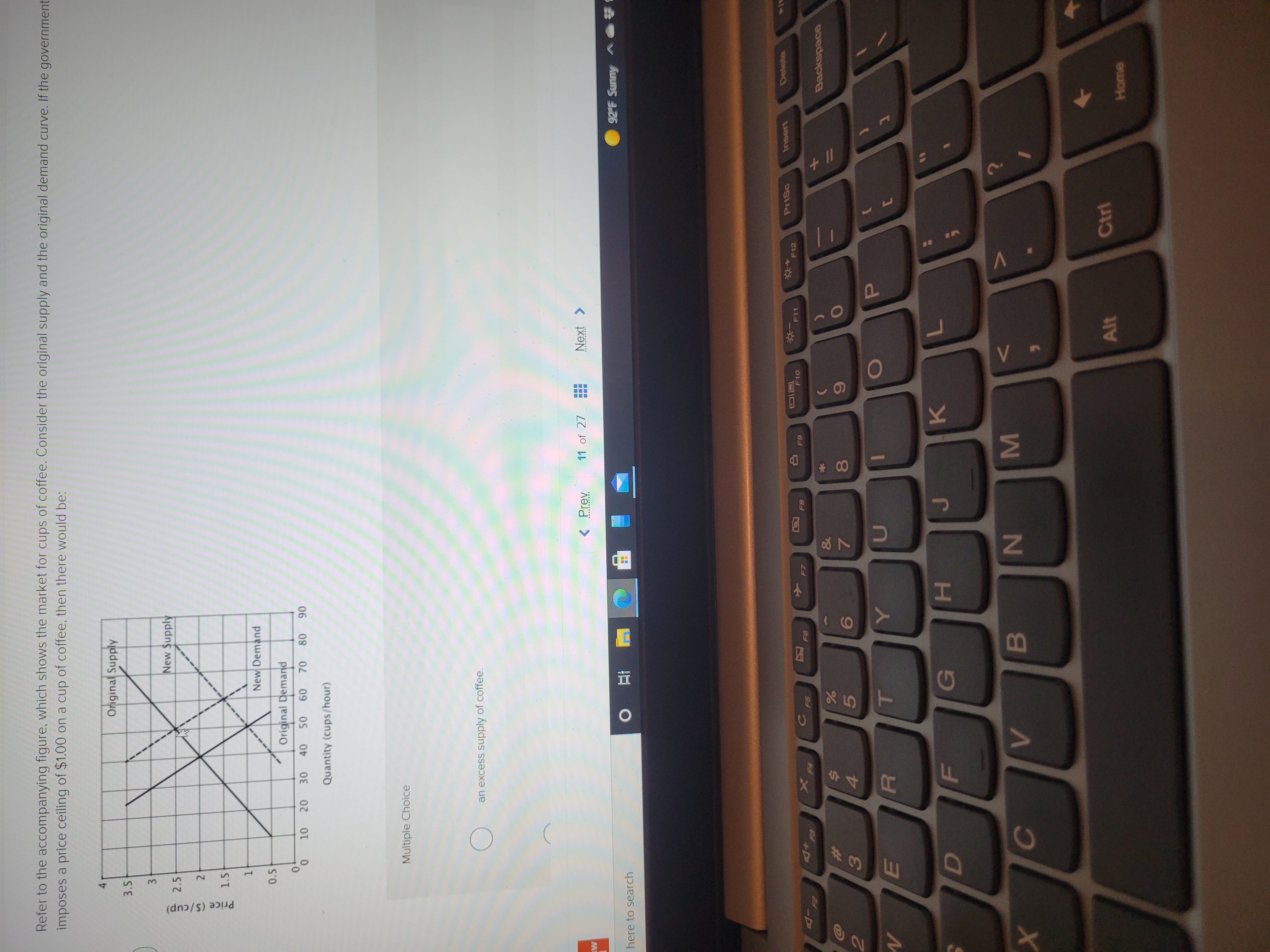

Transcribed Image Text:The image shows a graph that represents the market for cups of coffee. There are two supply curves and two demand curves.

1. **Axes**:

- The vertical axis represents the price of coffee per cup, ranging from $0 to $4.

- The horizontal axis represents the quantity of coffee cups per hour, ranging from 0 to 90.

2. **Curves**:

- **Original Supply (S1)**: An upward-sloping line originating near the bottom left and extending towards the top right.

- **New Supply (S2)**: Another upward-sloping line, indicating a shift to the right of the original supply curve, which suggests an increase in supply.

- **Original Demand (D1)**: A downward-sloping line from top left to bottom right.

- **New Demand (D2)**: Another downward-sloping line that indicates a shift to the right of the original demand curve, showing an increase in demand.

3. **Scenario**:

The problem states: "Consider the original supply and the original demand curve. If the government imposes a price ceiling of $1.00 on a cup of coffee, then there would be:"

4. **Multiple Choice**:

- An option suggesting "an excess supply of coffee."

This implies examining the intersection of the original curves (S1 and D1) with the imposed price ceiling at $1.00, likely resulting in a different equilibrium situation.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- (35) Consumers who gain the highest marginal benefit from a good supplied by a perfectly price-discriminating producer will pay the least pay the most pay the same as the good's other consumers be unable to purchase the good consume all the available units of the goodarrow_forwardHomework (Ch 05) 80, 2 Demand 10 20 30 40 50 60 70 90 100 QUANTITY (Thousands of pounds of tomatoes) According to the midpoint method, the price elasticity of demand for tomatoes between point X and point Y is approximately which suggests that the demand for tomatoes is between points X and Y. RICE (Dollars per pound)arrow_forwardWhat is the slope of the given demand curve?arrow_forward

- Please answer 1 and 2arrow_forwardConsider the weekly supply of gasoline in Figure 1. How much gasoline will producers wish to sell if the price of a gallon of gasoline is $1.20? A) 100K gallons b) 140K gallons C) 236K gallons D) 308K gallonsarrow_forwardSuppose the demand for a product is given by D (p) = - elasticity of demand at a price of $27. Elasticity what price do you have unit elasticity? (Round your answer to the nearest penny.) Price 5p+227. A) Calculate the == (Round to three decimal places.) B) At = $arrow_forward

- In a particular market, demand and supply curves are defined by the following equations: P=50 – 0.5QD QS= -20 + 2P where, P is the price in pounds, QS is the quantity supplied and QD is the quantity demanded. 1. What is the equilibrium price and quantity? 2. What is the price elasticity at a price of £35? 3. What do you expect will happen to total expenditure on this good if the price increases from £35 to £40? Is this expectation confirmed if you calculate the total revenue for each price?arrow_forwardThe task I am struggling with. Thank you.arrow_forwardA particular commodity has a price-demand equation given by p = √18,444 - 417x, where x is the amount in pounds of the commodity demanded when the price is p dollars per pound. (a) Find consumers' surplus if the equilibrium quantity is 40 pounds. (Round your answer to the nearest cent if necessary.) (b) Find consumers' surplus if the equilibrium price is 17 dollars. (Round your answer to the nearest cent if necessary.) $arrow_forward

- Suppose that the government has a goal to reduce the demand for cigarettes in support of a health program. Given this, the government decided to impose a per-unit tax of 40 centavos per pack that is levied on the sellers or placed on the sale of cigarettes by the government. This causes a shift of the market supply of cigarettes from S to S' as shown. Price ($ per pack) S 1.50 1.40 1.30 1.15 D₂ Quantity (Millions of pack) 3 4 5 Answer the following questions regarding this case. 1. Determine the deadweight loss to society caused by the imposition of the tax. (3 points) Interpret the result. (3 points) 1 2. What tax revenue is expected to be collected by the government? (4 points) 1.25 + 1 1 D₁arrow_forward*4* When the price of product "X" is (P1=) $42, Shyanne purchases 20 units of product "X" and when the price of product "X" is (P2=) $38, she purchases 30 units of product "X". Shyanne's "arc" price elasticity of demand for product "X" is (Ex,x =): O" -0.25 " and the demand for "X" is relatively elastic. -4.00 " and the demand for "X" is relatively inelastic. O"-0.25 " and the demand for "X" is relatively inelastic. O " -4.00 " and the demand for "X" is relatively elastic. -0.25 " and "X" is a "normal" good. Save & Continue Continue without savingarrow_forwardIf price elasticity of supply is 1.5 and price increases by 3 percent, quantity supplied will Increase by ((Click to select) :arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education