FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

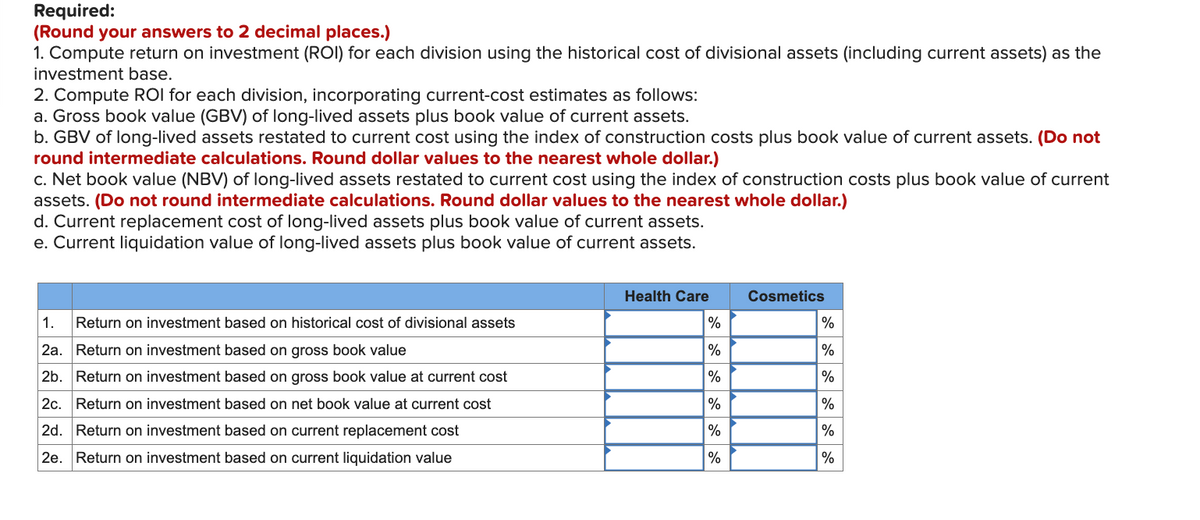

Transcribed Image Text:Required:

(Round your answers to 2 decimal places.)

1. Compute return on investment (ROI) for each division using the historical cost of divisional assets (including current assets) as the

investment base.

2. Compute ROI for each division, incorporating current-cost estimates as follows:

a. Gross book value (GBV) of long-lived assets plus book value of current assets.

b. GBV of long-lived assets restated to current cost using the index of construction costs plus book value of current assets. (Do not

round intermediate calculations. Round dollar values to the nearest whole dollar.)

c. Net book value (NBV) of long-lived assets restated to current cost using the index of construction costs plus book value of current

assets. (Do not round intermediate calculations. Round dollar values to the nearest whole dollar.)

d. Current replacement cost of long-lived assets plus book value of current assets.

e. Current liquidation value of long-lived assets plus book value of current assets.

1. Return on investment based on historical cost of divisional assets

2a. Return on investment based on gross book value

2b. Return on investment based on gross book value at current cost

2c. Return on investment based on net book value at current cost

2d. Return on investment based on current replacement cost

2e. Return on investment based on current liquidation value

Health Care

%

%

%

%

%

%

Cosmetics

%

%

%

%

%

%

Transcribed Image Text:Ready Products Incorporated operates two divisions, each with its own manufacturing facility. The accounting system reports the

following data for 2022:

HEALTH CARE PRODUCTS DIVISION

Income Statement

For the Year Ended December 31, 2022

Revenues

Operating costs

Operating income

COSMETICS DIVISION

Income Statement

For the Year Ended December 31, 2022

Revenues

Operating costs

$1,500

730

$770

Operating income

Year

2016

2017

2018

2019

2020

2021

2022

Ready estimates the useful life of each manufacturing facility to be 21 years. As of the end of 2022, the plant for the health care

division is 4 years old, while the manufacturing plant for the cosmetics division is 6 years old. Each plant had the same cost at the time

of purchase, and both have useful lives of 21 years with no salvage value. The company uses straight-line depreciation and the

depreciation charge is $106,000 per year for each division. The manufacturing facility is the only long-lived asset of either division.

Current assets are $330,000 in each division.

An index of construction costs, replacement costs, and liquidation values for the manufacturing facilities for the period that Ready has

been operating is as follows:

$2,100

1,220

$ 880

Cost

Index

80

82

84

89

94

96

100

Replacement

Cost

$ 1,000,000

1,000,000

1,100,000

1,150,000

1,200,000

1,250,000

1,300,000

Liquidation Value

Health Care Cosmetics

$ 800,000 $ 800,000

800,000

800,000

600,000

600,000

600,000

700,000

700,000

700,000

600,000

800,000

800,000

900,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Divisional Income Statements with Support Department Allocations Horton Technology has two divisions, Consumer and Commercial, and two corporate support departments, Tech Services and Purchasing. The corporate expenses for the year ended December 31, 20Y7, are as follows: Tech Services Department $905,200 Purchasing Department 380,000 Other corporate administrative expenses 553,000 Total expense $1,838,200 The other corporate administrative expenses include officers’ salaries and other expenses required by the corporation. The Tech Services Department allocates costs to the divisions based on the number of computers in the department, and the Purchasing Department allocates costs to the divisions based on the number of purchase orders for each department. The services used by the two divisions are as follows: Tech Services Purchasing Consumer Division 450 computers 5,300 purchase orders Commercial Division 280 9,900 Total 730 computers 15,200 purchase…arrow_forwardCrane Company has four operating divisions. During the first quarter of 2022, the company reported aggregate income from operations of $ 210,600 and the following divisional results. Division I II III IV Sales $ 245,000 $ 197,000 $ 504,000 $ 450,000 Cost of goods sold 200,000 192,000 301,000 249,000 Selling and administrative expenses 72,400 63,000 58,000 50,000 Income (loss) from operations $ ( 27,400) $ ( 58,000) $ 145,000 $ 151,000 Analysis reveals the following percentages of variable costs in each division. I II III IV Cost of goods sold 73 % 91 % 82 % 75 % Selling and administrative expenses 39 59 50 61 Discontinuance of any division would save 50% of the fixed costs and expenses for that division.Top management is very concerned about the unprofitable divisions (I and II). Consensus is that one or both of the…arrow_forwardJansen Company reports the following for its ski department for the year 2019. All of its costs are direct, except as noted. Sales $ 605,000 Cost of goods sold 430,000 Salaries 112,000 ($25,600 is indirect) Utilities 17,200 ($5,100 is indirect) Depreciation 45,000 ($17,100 is indirect) Office expenses 22,800 (all indirect) 1. Prepare a departmental income statement for 2019.2. & 3. Prepare a departmental contribution to overhead report for 2019. Based on these two performance reports, should Jansen eliminate the ski department?arrow_forward

- Cost Department Allocations In divisional income statements prepared for Demopolis Company, the Payroll Department costs are charged back to user divisions on the basis of the number of payroll distributions, and the Purchasing Department costs are charged back on the basis of the number of purchase requisitions. The Payroll Department had expenses of $34,760, and the Purchasing Department had expenses of $15,660 for the year. The following annual data for Residential, Commercial, and Government Contract divisions were obtained from corporate records: Sales Number of employees: Weekly payroll (52 weeks per year) Monthly payroll Number of purchase requisitions per year Number of payroll checks: Weekly payroll x 52 Monthly payroll x 12 Total Residential $ 327,000 Support department allocations: Payroll Department Purchasing Department 175 32 2,300 Total Commercial $ 434,000 Required: a. Determine the total amount of payroll checks and purchase requisitions processed per year by the…arrow_forwardTerra Company has two divisions, the Retail Division and the Wholesale Division. The following information was gathered for the two divisions for the current year: Operating income Operating assets Retail Division $ 7,200,000 $37,200,000 Wholesale Division $ 3,700,000 $17,200,000 Assuming that these are the only divisions of Terra Company, what is the ROI for the company as a whole?arrow_forwardwant correct answer for this questionarrow_forward

- The sales, gross profit, and direct and indirect operating expenses of Departments A and B of Cardoba Inc. are as follows: Dept. A Dept. B Total Sales $420,000 $290,000 $710,000 Gross profit 243,000 197,000 440,000 Direct operating expenses 205,000 118,000 323,000 Indirect operating expenses 160,000 Help compute the departmental direct operating margin and direct operating margin percentage for each department.arrow_forwardDengararrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education