ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

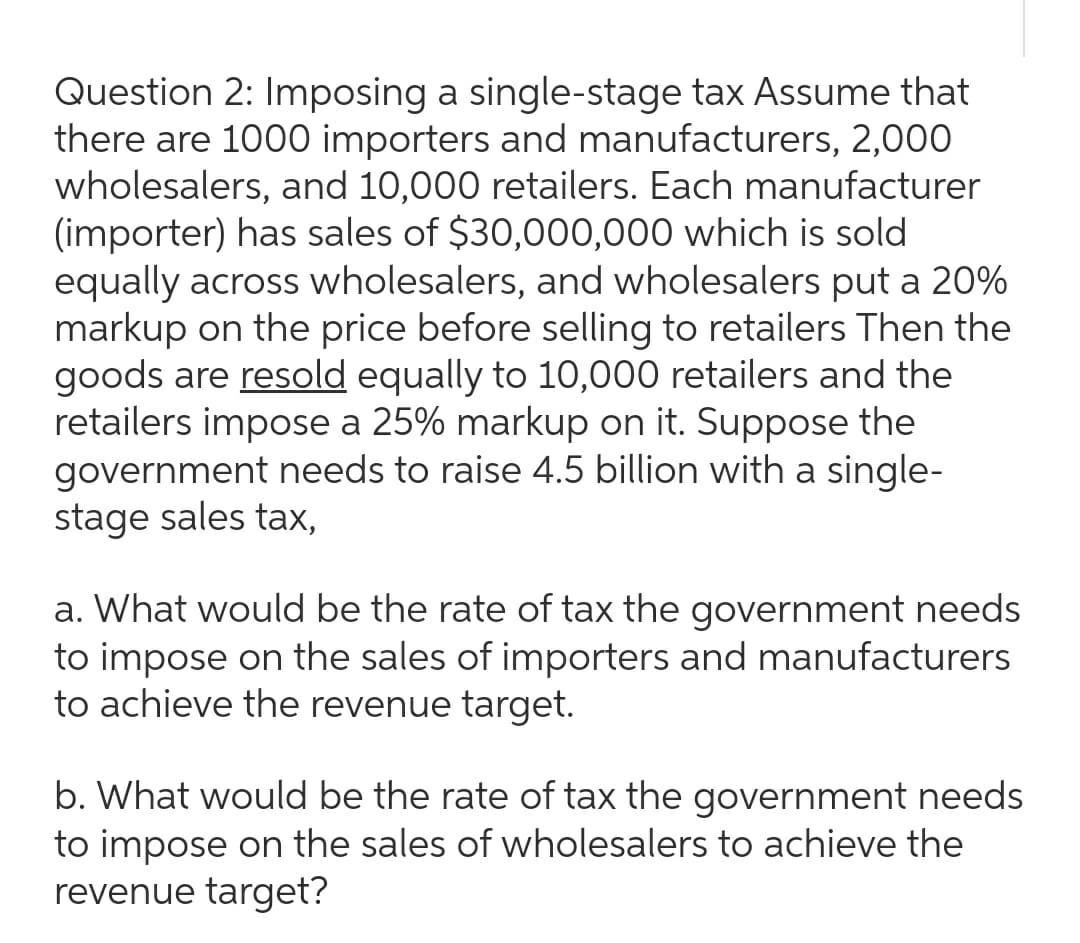

Transcribed Image Text:Question 2: Imposing a single-stage tax Assume that

there are 1000 importers and manufacturers, 2,000

wholesalers, and 10,000 retailers. Each manufacturer

(importer) has sales of $30,000,000 which is sold

equally across wholesalers, and wholesalers put a 20%

markup on the price before selling to retailers Then the

goods are resold equally to 10,000 retailers and the

retailers impose a 25% markup on it. Suppose the

government needs to raise 4.5 billion with a single-

stage sales tax,

a. What would be the rate of tax the government needs

to impose on the sales of importers and manufacturers

to achieve the revenue target.

b. What would be the rate of tax the government needs

to impose on the sales of wholesalers to achieve the

revenue target?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Question 2iarrow_forwardIn Figure 3.7, applying a $1.05 specific tax causes the equilibrium price to rise by 70¢ and the equilibrium quantity to fall by 14 million kg of pork per year. Using the pork supply function and the original and after-tax demand functions, derive these results using algebra. Figure 3.7arrow_forwardPrice (dollars per pizza) 20 16 14 10 8 6 4 2 S+ tax on sellers S D 0 10 20 30 40 50 60 70 80 90 100 Quantity (thousands of pizzas) The figure above shows the pizza market in the city of Pepperoniville. If the government imposes the sales tax shown in the figure on sellers, then the price the buyer pays for pizza is $ and the price the seller receives for the pizza is $ Just enter value. Do not include the "$" sign.arrow_forward

- If the demand for a product is inelastic but the supply is elastic, the ________ will bear the tax incidence. Question 43 options: a) the local government b) the producer c) the consumer d) the federal governmentarrow_forwardSuppose demand is represented by P = 100 - 2Q, and supply is represented by P = 5 + 3Q. If the government imposes a $5 per unit tax, to be collected from the sellers, what is the price elasticity of demand between the pre- and post-tax equilibriums? 0.5 0.63 1 ( 1.7 油arrow_forwardThe inverse demand function is p = 10q, where q is the number of units sold. The inverse supply function is defined by p = 2 + q. A tax of $2 is imposed on suppliers for each unit that they sell. After the tax is imposed, the equilibrium quantity with taxes is. 0 1 07 O 3 04 09arrow_forward

- Refer to Figure 2. It shows the imposition of a per-unit tax on the market for cigarettes. S = Market Supply Curve; D = Market Demand Curve; S+Tax = Market Supply Curve with per-unit tax imposed. The total tax collected can be represented by: A) Triangle ABFB) Rectangle PTaxC) Rectangle PTaxECAD) Rectangle P0 ECBarrow_forwardNonearrow_forward1) Describe in detail how taxes impact consumer and producer surplus. In your discussion, also show graphically, the before and after-tax impact.arrow_forward

- Doyle and Samphantharak (2008) find that when a 5% gas tax is implemented, prices consumers pay for gas increase by about 4%. What role does demand elasticity play in determining the size of this price change? That is, under what demand elasticity cases would the price change be closer to 5%, or closer to 0%? Illustrate and explain using supply-and-demand graph(s)..arrow_forwardNote: use of chat gpt or Google bard is strictly prohibited.arrow_forward18. Suppose that corporate income tax in Japan is 30% for large enterprises. And one of them is Nissan Japan. Assume that Nissan Japan places its electric vehicles (EV) factory in California, USA by setting up Nissan America. California charges enterprises with a 10% corporate (flat) income tax rate. Suppose the demand of Nissan EV in Japan is p=220-2Q (p: price in one hundred thousand yen, Q is number of EV per week). Costs of transporting EV cars from California to Japanese customers and taxes and fees related to export-import activities are assumed to be zero. Its production cost in California is constant at 20 per unit. If Nissan American sells EVS produced in California to Nissan Japan at its production cost, what are the combined net profits of all Nissans and total corporate income tax the Nissan Japan has to pay (per week)? (Note: Nissan Japan will use the transfer price as its marginal cost.) ONet profit=5000; Sum of corporate tax=1500 Net profit=3500; Sum of corporate…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education