ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

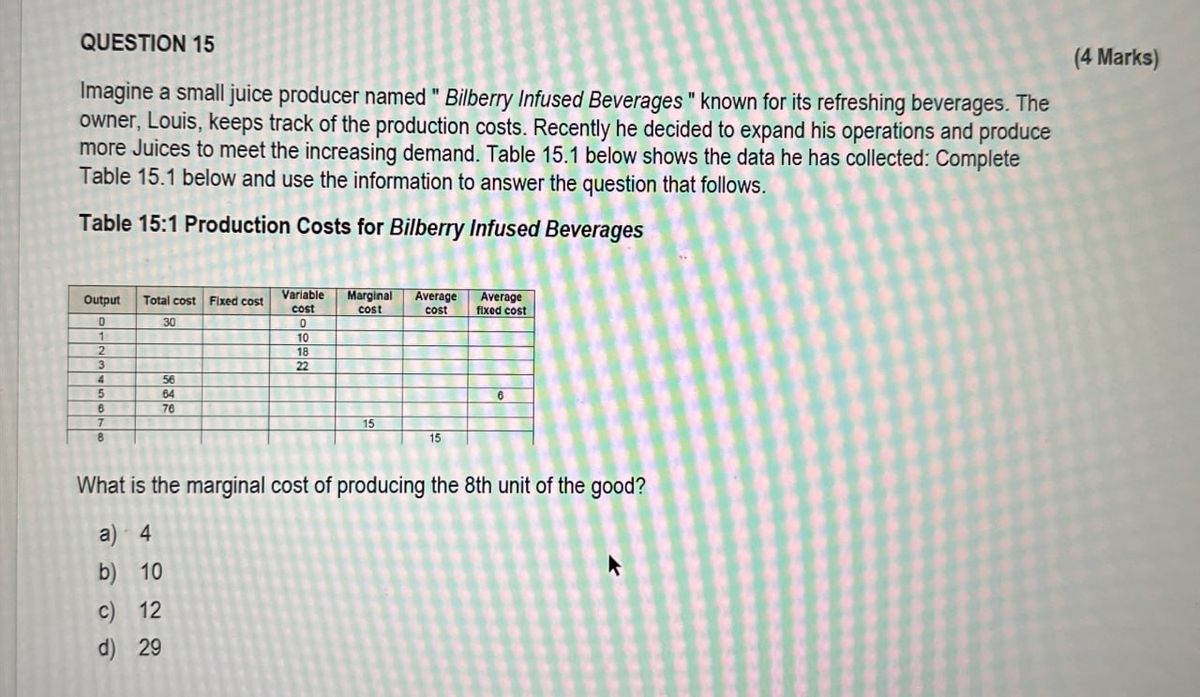

Transcribed Image Text:QUESTION 15

Imagine a small juice producer named "Bilberry Infused Beverages" known for its refreshing beverages. The

owner, Louis, keeps track of the production costs. Recently he decided to expand his operations and produce

more Juices to meet the increasing demand. Table 15.1 below shows the data he has collected: Complete

Table 15.1 below and use the information to answer the question that follows.

Table 15:1 Production Costs for Bilberry Infused Beverages

(4 Marks)

Output

0

Total cost

30

Fixed cost

Variable

cost

Marginal Average

cost

Average

cost

fixed cost

0

1

10

18

3

22

4

56

5

64

6

B

76

7

8

15

15

What is the marginal cost of producing the 8th unit of the good?

a) 4

b) 10

c) 12

d) 29

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Problem 05-06 A firm's fixed costs for 0 units of output and its average total cost of producing different output levels are summarized in the table below. Complete the table to find the fixed cost, variable cost, total cost, average fixed cost, average variable cost, and marginal cost at all relevant levels of output. Instruction: Enter your responses for Average Fixed Cost (AFC) and Average Variable Cost (AVC) rounded to two decimal places. All other responses should be entered as whole numbers. If you are entering a negative number, use a negative sign (-) where appropriate. Q AVC ATC MC 150 300 75 200 H50 175 225 30 325 25 400 FC VC TC AFC 0 $ 15,000 0 100 15000 200 15000 300 15000 400 15000 500 15000 600 15000arrow_forwardQ15arrow_forwardplease only solve part g!arrow_forward

- Question 1 Include correctly labeled diagrams, if useful or required, in explaining your answers. A correctly labeled diagram must have all axes and curves clearly labeled and must show directional changes. If the question prompts you to "Calculate," you must show how you arrived at your final answer. Quantity of Output Total Cost $12 1 $14 2 $18 $24 4 $32 5 $42 6 $54 7 $68 The table above shows the total cost function for a typical firm producing hats in a perfectly competitive market. The market price for hats is $9 per hat. (a) Calculate the average variable cost of the fifth unit. Show your work. (b) What is the firm's profit-maximizing quantity of hats? Explain using marginal analysis. (c) Draw a correctly labeled graph showing the firm's demand and marginal cost curves, and show the profit-maximizing quantity of hats determined in part (b). (d) If the rent of the building the firm occupies increases, what will happen to the firm's profit-maximizing quantity of output in the short…arrow_forwardQUESTION 15 Imagine a small juice producer named " Bilberry Infused Beverages" known for its refreshing beverages. The owner, Louis, keeps track of the production costs. Recently he decided to expand his operations and produce more Juices to meet the increasing demand. Table 15.1 below shows the data he has collected: Complete Table 15.1 below and use the information to answer the question that follows. Table 15:1 Production Costs for Bilberry Infused Beverages (4 Marks) Output Total cost Fixed cost Variable Marginal Average cost cost cost Average fixed cost 0 30 O 1 10 2 18 3 22 4 5 64 B 832 8 76 7 8 15 15 What is the marginal cost of producing the 8th unit of the good? a) 4 b) 10 c) 12 d) 29arrow_forwardAnswer the following questions in your own words. Start a new thread while replying. 1. What are the determinants of price elasticity of demand? Explain the determinants. 2. What is the difference between inelastic demand and elastic demand? Provide an example of each from real life. 3. Refer to the graph below: Price 22 20 + 18 +- 16 + 14 B 12 10 + 4 Demand +++ 100 200 300 400 500 600 700 800 900 Buaxtity From the graph above calculate: a. Price elasticity of demand from point A to point B (use the mid-point method). Is it an elastic situation or an inelastic situation? b. Price elasticity of demand from point B to point C (use the mid-point method). Is it an elastic situation or an inelastic situation?arrow_forward

- Consider the production of hamburgers. The average total cost (ATC) and average fixed cost (AFC) of producing hamburgers are illustrated in the graph to the right Use the four-point curve drawing tool to graph the average variable cost of producing one, two, three, and four thousand hamburgers. Properly label this curve Carefully follow the instructions above, and only draw the required objects. Cost (cente per unit) 26 24- 22- 20 18- 16 14- 12- 10 B 6 4- 2 ATC AFG Quantity of hamburgers (in 1000s) Q duarrow_forwardQuestion 15 (i) Which of the following is(are) correct about how accountants and economists consider costs? Accountants consider only implicit costs Economists consider both explicit and implicit costs A: 1 only B: 2 only C: Both 1 and 2 D: Neither 1 nor 2 (ii) Which of the following statements is(are) correct for a monopoly firm and a competitive firm? Both firms earn economic profit in the long run. Both firms aim to maximize profit and produce at P = MC. A: 1 only B: 2 only C: Both 1 and 2 D: Neither 1 nor 2arrow_forwardpart Earrow_forward

- Costs and Profit Maximization: Work It Out 1 Suppose Margie decides to lease a photocopier and open up a black-and-white photocopying service in her dorm room for use by faculty and students. Her total cost, as a function of the number of copies she produces per month, is given in the table. Number of Photocopies Per Month Total Cost Fixed Cost Variable Cost Total Revenue Profit 0 $100 1,000 $110 2,000 $125 3,000 $145 4,000 $175 5,000 $215 6,000 $285 a. Fill in the missing numbers in the table, assuming that Margie can charge 6 cents per black-and-white copy. Margie's fixed cost is: $ Variable cost, 0 photocopies/month: $ Variable cost, 1,000 photocopies/month: $ Variable cost, 2,000 photocopies/month: $ Variable cost, 3,000 photocopies/month: $ Variable cost, 4,000 photocopies/month: $…arrow_forwardThe following is a cost schedule for A & E Manufacturing Company Ltd for product X. Quantity (Q) Fixed Cost Variable Cost Total Cost Marginal Cost Average Fixed Cost Average Variable Cost Average Total Cost 0 100 1 30 2 25 3 60 4 100 18 Required: Calculate the missing costs and complete the schedule. On one diagram, plot and label the Marginal Cost curve, the Average Fixed Cost curve, Average Variable Cost Curve and the Average Total Cost curve. Explain the relationship which exists between the Marginal Cost Curve and the Average Total Cost Curve. What accounts for the ‘U’ shape of the Average Total Cost Curve?arrow_forwardHelparrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education