Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

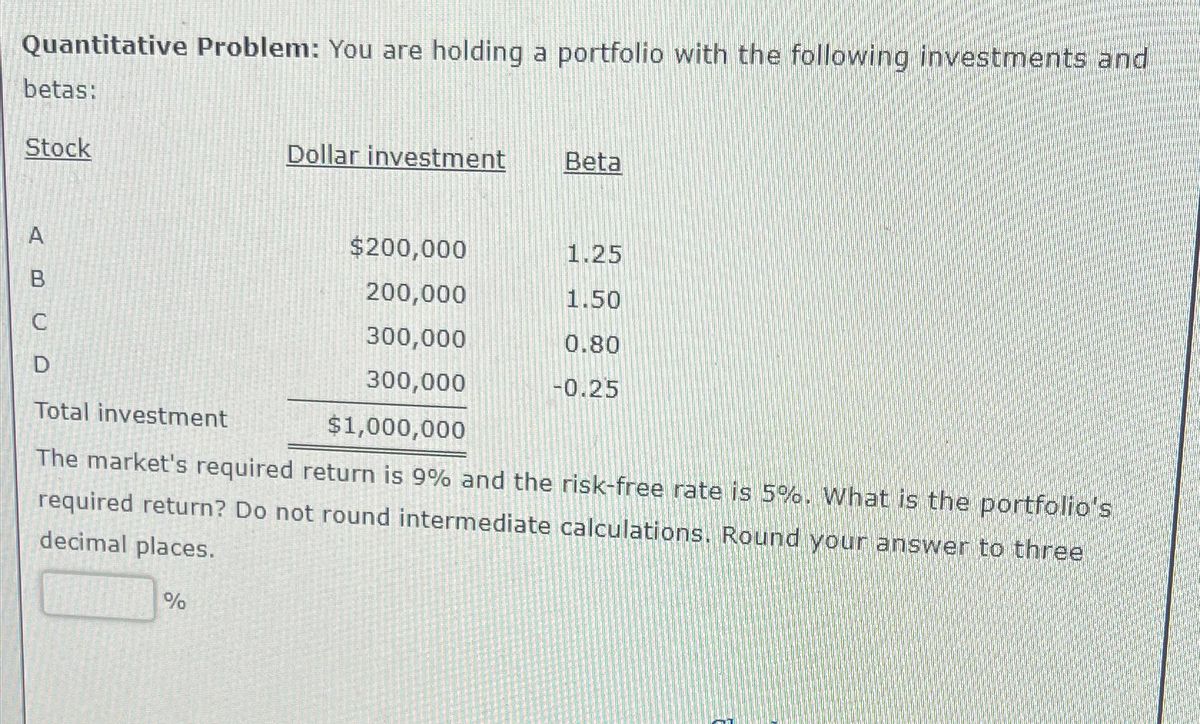

Transcribed Image Text:Quantitative Problem: You are holding a portfolio with the following investments and

betas:

Stock

A

B

C

D

Dollar investment

%

$200,000

200,000

300,000

300,000

Beta

1.25

1.50

0.80

-0.25

Total investment

$1,000,000

The market's required return is 9% and the risk-free rate is 5%. What is the portfolio's

required return? Do not round intermediate calculations. Round your answer to three

decimal places.

SAVE

AI-Generated Solution

info

AI-generated content may present inaccurate or offensive content that does not represent bartleby’s views.

Unlock instant AI solutions

Tap the button

to generate a solution

to generate a solution

Click the button to generate

a solution

a solution

Knowledge Booster

Similar questions

- Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free rate, rƒ. The characteristics of two of the stocks are as follows: Stock Expected Return Standard Deviation A 8% 55% B 4% 45% Correlation = −1 Required: a. Calculate the expected rate of return on this risk-free portfolio? (Hint: Can a particular stock portfolio be formed to create a “synthetic” risk-free asset?) (Round your answer to 2 decimal places.) b. Could the equilibrium rƒ be greater than rate of return?arrow_forwardAn investor is forming a portfolio by investing $50,000 in stock A which has a beta of 2.40, and $50,000 in stock B which has a beta of 0.60. The return on the market is equal to 8% and treasure bonds have a yield of 3% (rRF). What’s the portfolio beta? 0.60 1.30 1.50 1.80 Using the information in Question 41, calculate the required rate of return on the investor’s portfolio 11.0% 15.0% 12.0% 10.5% A retail store is offering a diamond ring for sale for 36 months at $128 per month. The retail price of the ring is $4,000. What is the interest rate on this offer? 9.43% 11.20% 11.98% 12.11%arrow_forwardCurrently the risk-free rate equals 5% and the expected return on the market portfolio equals 11%. An investment analyst provides you with the following information: Stock A Beta 1.33 Expected Return 12% Stock B Beta 0.7 Expected Return 10% (a) Calculate the reward-to-risk ratios of stock A, stock B and in market equilibrium. Are stock A and stock B overvalued, undervalued or fairly valued? Briefly explain. [within 150 words] (b) You want a portfolio with the same risk as the market. Calculate the weights of stock A and B respectively. (please show me steps and round the final answer to 2 decimal places, thanks)arrow_forward

- Assume CAPM holds. What is the correlation between an efficient portfolio and market portfolio? a. 1 b.-1 c.0 d. Not enough information Assume CAPM holds. The risk-free rate is 1% and the expected return on the portfolio is 5%. What is the expected return of a stock with a beta of 2? 70%arrow_forwardVijayarrow_forwardQuestion 1: Assume that you manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 27%. The T-bill rate is 7%. Your client chooses to invest 70% of a portfolio in your fund and 30% in a T-bill money market fund. Stock A Stock B Stock C 1. Calculate the client expected return on the complete portfolio 2. Calculate the reward-to-variability ratio (Sharpe ratio): Part B A three-asset portfolio has the following characteristics: Expected Return Asset X Y Z 15% 10 6 Standard Deviation What is the expected return on this three-asset portfolio? 27% 33% 40% 22% 8 3 Weight 0.50 0.40 0.10arrow_forward

- Start with A-C and I will submit seperately for D! Thank you :)arrow_forwardParts A-C have already been answered, looking for answer D.arrow_forwardConsider following information on a risky portfolio, risk-free asset and the market index. What is the Sharpe ratio of the market index? Risky portfolio Risk-free asset Market index Average return 8.2% 2% 6% Std. Dev. 26% 20% Residual std. dev. 10% Alpha 1.4% Beta 1.2arrow_forward

- Consider following information on a risky portfolio, risk-free asset and the market index. What is the M2 of the risky portfolio? Risky portfolio Risk-free asset Market index Average return 8.2% 2% 6% Std. Dev. 26% 20% Residual std. dev. 10% Alpha 1.4% Betaarrow_forwardBased on this image, how many stocks does it take to eliminate most of the diversifiable risk?arrow_forwardUse the expected return-beta equation from the CAPM. What is the expected return for a stock if the risk-free rate is 4%, beta 0.9 and the expected return for the market portfolio is 6%? What is the risk-free rate if beta is 1.1, the expected return 6.3% and the expected return for the market portfolio is 6%? What is beta if the risk-free rate is 4%, the expected return 11% and the expected return for the market is 6%? What is the expected return for the market if the risk-free rate is 4%, beta 0.9 and the expected return 11%?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education