Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

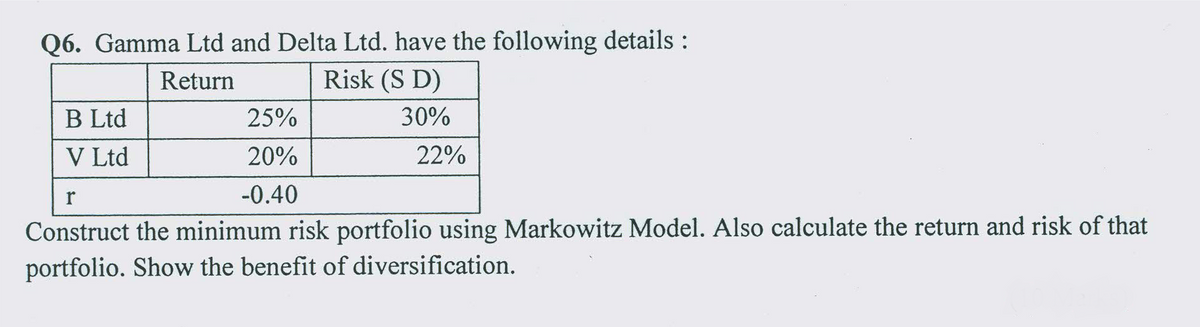

Transcribed Image Text:Q6. Gamma Ltd and Delta Ltd. have the following details:

Risk (S D)

Return

B Ltd

25%

30%

V Ltd

20%

22%

-0.40

Construct the minimum risk portfolio using Markowitz Model. Also calculate the return and risk of that

portfolio. Show the benefit of diversification.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- PLEASE PUT IT IN EXCEL, IT HAS TO BE IN EXCEL NO OTHER WAY OTHER THEN IN EXCEL. USE EXCEL! Question 2: Consider two risky assets, S and B, with the following characteristics: E(rs) 9%, Os 20% E(TB) 5%, OB 5% and PBS - 1 a) Is it possible to combine the two assets a portfolio such that the portfolio has zero risk (i.e. zero standard deviation)? If so, what is the composition of the zero risk portfolio? b) Suppose that in addition to trading in the risky assets S and B, investors can also freely buy, sell or short-sell a risk-free asset with risk-free rate rf. What must be the risk-free rate re? What would happen otherwise?arrow_forwardneed helparrow_forwardA diagram of the CML and SML for the market M, risk-free asset ry, an inefficient portfolio P, and a complete portfolio C is shown below. The diagram is not to scale. E(r) E(13) CML & CALP E(12) P C E(r) M 01 02 03 P βρ SML M Вм The values of the labeled variables are E[1] = 3.0%, E[12] = 10.3%, E[3] = 16.7%, σ₁ = 17.9%, σ = 30.0%, 03 = 44.3%. What is the standard deviation of nonsystematic risk for the complete portfolio σc under the CAPM? O a. 0.1374 O b. 0.1180 O c. 0.0988 d. 0.1105 O e. 0.0791 O f. 0.0913 Og. 0.0858 O h. 0.1443arrow_forward

- Calculate the optimal risky portfolio for the following cases when short-sales are allowed. Compute its expected return and the standard deviation of its returns. 1. Two risky assets: Rp = 3, R' = [6, 9], and 4 5 5 20 2. Three risky assets: Rp = 4, R' = [5,9, 8], and [10 0 0 E=0 40 0 0 20 3. Three risky assets: Rp = 5, R' = [12, 9, 8], and 40 10 -5] E= 10 20 0 5 0 30 4. Five risky assets: Rp = 2, R' = [5, 3, 18, 9, 2], and %3D 2 16 0. -12 5 -12 20 16 10 7 14 27 14 9. -13 8. 7 27 13arrow_forwardConsider the following risk-return characteristics for funds A and B: Expected return Risk Fund A (Equity) 12% 20% Fund B (Debt) 9% 16% The correlation coefficient between the returns of fund A and fund B is 0.4. 1. Which Fund is riskier? Write 1 if your answer is Fund A, write 2 if your answer is Fund B, or write 3 if your answer is undetermined. 2.1 What is the weight of fund A in the minimum variance portfolio? 2.4 What is the risk of the minimum variance portfolio? 2.2 What is the weight of Fund B in the minimum variance portfolio? 2.3 What is the expected return of the minimum variance portfolio?arrow_forwardhf.3arrow_forward

- QUESTION Assume that the expected rates of return and the beta coefficients of the alternatives supplied by an independent analyst are as follows: Security Estimated rate of returns Beta Nescom 5% 1.5 Market 4 1 Pk_Steel 3.5 0.75 T_Bills 3 0 Nawab 1 -0.6 What is a beta coefficient, and how are betas used in risk analysis? Do the expected returns appear to be related to each alternative’s market risk? Is it possible to choose among the alternatives on the basis of the information developed thus far?arrow_forwardIf the beta of Asset A is 2.2, the risk free rate is 2.5%, and the expected return on Asset A is 8%, what is the expected return on the market (Note: you want to use CAPM)? Group of answer choices 7.28% 5.00% 8.00% 16.80%arrow_forwardThe portfolio with the highest Sharpe Ratio is I. The minimum-variance point on the efficient frontier II. The tangency point of the capital market line and the efficient frontier III. The maximum-return point on the efficient frontier IV. The line with the steepest slope that connects the risk-free rate to the efficient frontier Select one: a. II and IV only b. I and IV only c. III and IV only d. Only IV e. I and II onlyarrow_forward

- Q6. ) A portfolio is formed by investing 32% in Asset-1; 28% in Asset-2; and 40% in Asset-3. The covariances of the three assets with the market portfolio are 24, 36, and 48. The variance of the market portfolio is 40. If the risk - less rate is 7.5%, and the expected return on the market portfolio is 12.5%, what is the expected return of this portfolio, assuming that the CAPM is valid?arrow_forwardNonearrow_forward<Urgent> please answer M9,M10,M11arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education