FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

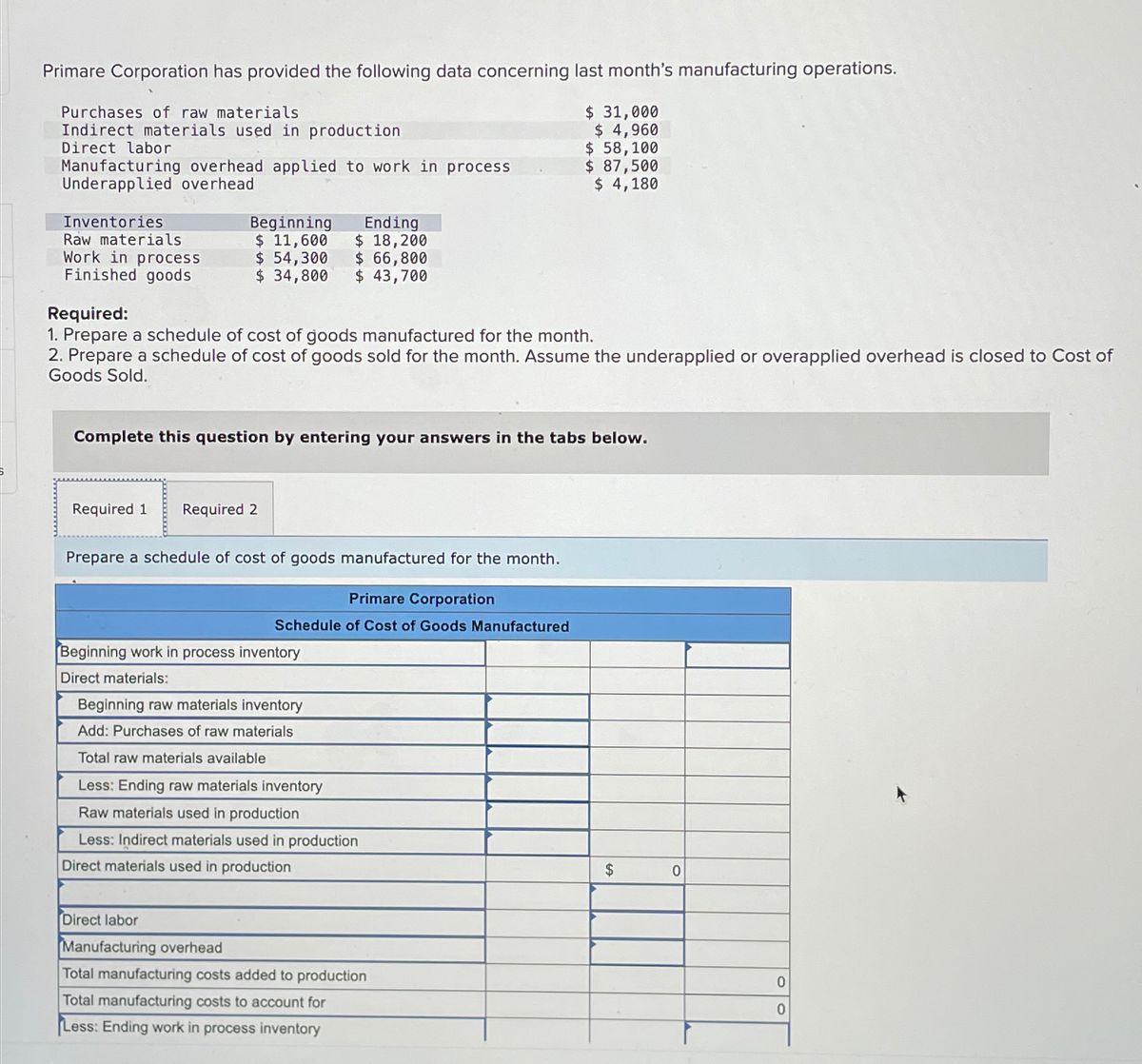

Transcribed Image Text:Primare Corporation has provided the following data concerning last month's manufacturing operations.

Purchases of raw materials

Indirect materials used in production

Direct labor

$ 31,000

$ 4,960

$ 58,100

Manufacturing overhead applied to work in process

Underapplied overhead

$ 87,500

$ 4,180

Inventories

Raw materials

Work in process

Finished goods

Required:

Beginning

Ending

$ 11,600 $ 18,200

$ 54,300 $ 66,800

$ 34,800

$ 43,700

1. Prepare a schedule of cost of goods manufactured for the month.

2. Prepare a schedule of cost of goods sold for the month. Assume the underapplied or overapplied overhead is closed to Cost of

Goods Sold.

Complete this question by entering your answers in the tabs below.

Required 1

Required 2

Prepare a schedule of cost of goods manufactured for the month.

Primare Corporation

Schedule of Cost of Goods Manufactured

Beginning work in process inventory

Direct materials:

Beginning raw materials inventory

Add: Purchases of raw materials

Total raw materials available

Less: Ending raw materials inventory

Raw materials used in production

Less: Indirect materials used in production

Direct materials used in production

$

0

Direct labor

Manufacturing overhead

Total manufacturing costs added to production

Total manufacturing costs to account for

Less: Ending work in process inventory

0

0

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- i need the answer quicklyarrow_forwardPrimare Corporation provided the following data for last month's manufacturing operations. Purchases of raw materials Indirect materials used in production Direct labor Manufacturing overhead applied to work in process Underapplied overhead Inventories Raw materials Work in process Finished goods Ending $ 19, 100 Beginning $ 11, 100 $ 55,500 $ 66,300 $ 34,000 $ 42, 600 $ 32,000 $ 4,910 $ 58,800 $ 88,400 $ 4,110 Required: 1. Prepare a schedule of cost of goods manufactured. 2. Prepare a schedule of cost of goods sold. Assume the underapplied or overapplied overhead is closed to Cost of Goods Sold.arrow_forwardK Inc. has provided the following data for the month of May: Inventories: Beginning Ending $ 31,000 $26,000 $ 60,000 $64,000 Work in process Finished goods Additional information: Direct materials $ 71,000 $101,000 $ 77,000 $ 75,000 Direct labor cost Manufacturing overhead cost incurred Manufacturing overhead cost applied to Work in Process Any underapplied or overapplied manufacturing overhead is closed out to cost of goods sold. The cost of goods manufactured for May is: Multiple Choice $254,000 $252,000 $247,000 $249,000arrow_forward

- Bledsoe Corporation has provided the following data for the month of November: Beginning $ 25,700 Ending $ 21,700 $ 17,700 $ 48,700 Inventories Raw materials Work in process Finished Goods Additional information: Raw materials purchases Direct labor cost $ 10,700 $56,700 Manufacturing overhead cost incurred Indirect materials included in manufacturing overhead cost incurred Manufacturing overhead cost applied to Work in Process Any underapplied or overapplied manufacturing overhead is closed out to cost of goods sold. Required: Prepare a Schedule of Cost of Goods Manufactured and a Schedule of Cost of Goods Sold. Complete this question by entering your answers in the table below. Schedule of Schedule of COGS COGM $ 72,700 $ 92,700 $ 42,770 $ 4,070 $41,700arrow_forwardPrimare Corporation has provided the following data concerning last month's manufacturing operations. Purchases of raw materials Indirect materials used in production Direct labor Manufacturing overhead applied to work in process Underapplied overhead Inventories Raw materials Work in process Finished goods Beginning $ 10,700 $ 55,700 $ 33,100 Ending $ 18,000 $ 65,400 $ 43,200 $ 32,000 $ 4,950 $ 59,600 $ 88,700 $ 4,170 Required: 1. Prepare a schedule of cost of goods manufactured for the month. 2. Prepare a schedule of cost of goods sold for the month. Assume the underapplied or overapplied overhead is closed to Cost of Goods Sold.arrow_forwardplease step by step solution.arrow_forward

- Help fill outarrow_forwardGive me answerarrow_forwardHow can i resolve this problem? Primare Corporation has provided the following data concerning last month’s manufacturing operations. Purchases of raw materials $ 30,000 Indirect materials used in production $ 4,990 Direct labor $ 59,000 Manufacturing overhead applied to work in process $ 88,200 Underapplied overhead $ 4,130 Inventories Beginning Ending Raw materials $ 11,700 $ 18,600 Work in process $ 55,800 $ 67,300 Finished goods $ 33,400 $ 42,900 Required: 1. Prepare a schedule of cost of goods manufactured for the month. 2. Prepare a schedule of cost of goods sold for the month. Assume the underapplied or overapplied overhead is closed to Cost of Goods Sold.arrow_forward

- Using the attached Prepare a schedule of cost of goods manufactured.arrow_forwardPrimare Corporation has provided the following data concerning last month's manufacturing operations. Purchases of raw materials Indirect materials used in production Direct labor Manufacturing overhead applied to work in process Underapplied overhead Inventories Raw materials Work in process Finished goods Beginning $ 11, 200 $ 55,700 $ 33,700 Ending $ 19,900 $ 65,800 $ 42,800 $ 31,000 $ 4,940 $ 59,300 $ 87,600 $ 4,080 Required: 1. Prepare a schedule of cost of goods manufactured for the month. 2. Prepare a schedule of cost of goods sold for the month. Assume the underapplied or overapplied overhead is closed to Cost of Goods Sold.arrow_forwardPrimare Corporation has provided the following data concerning last month’s manufacturing operations. Purchases of raw materials $ 31,000 Indirect materials used in production $ 4,860 Direct labor $ 59,700 Manufacturing overhead applied to work in process $ 88,100 Underapplied overhead $ 4,120 Inventories Beginning Ending Raw materials $ 11,500 $ 18,600 Work in process $ 54,000 $ 65,900 Finished goods $ 33,600 $ 42,400 Required: Prepare a schedule of cost of goods manufactured for the month. Prepare a schedule of cost of goods sold for the month. Assume the underapplied or overapplied overhead is closed to Cost of Goods Sold.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education