ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

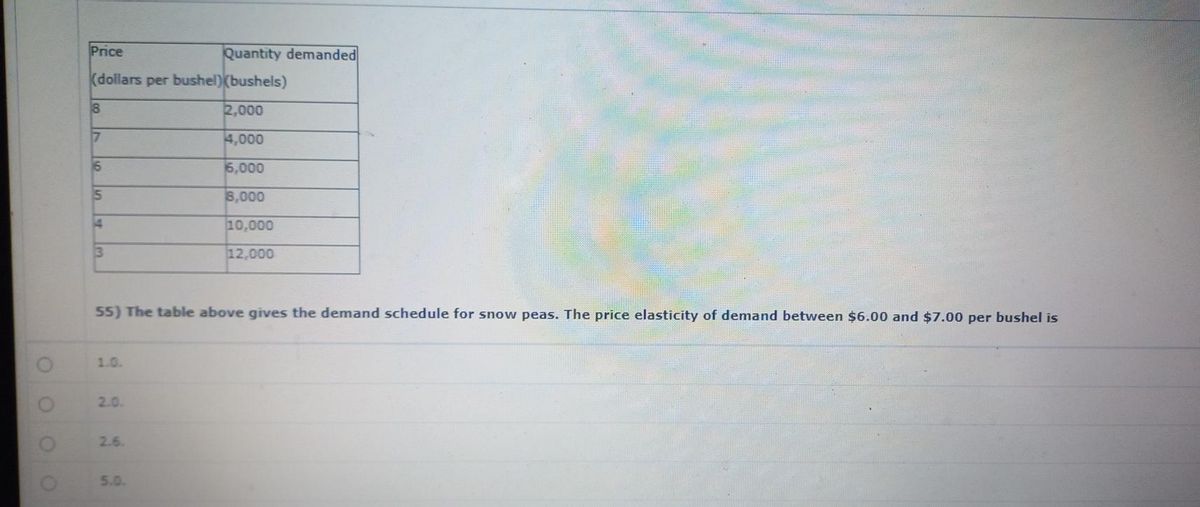

Transcribed Image Text:Price

Quantity demanded

(dollars per bushel)(bushels)

2,000

17

4,000

16

6,000

IS

8,000

14

10,000

3

12,000

55) The table above gives the demand schedule for snow peas. The price elasticity of demand between $6.00 and $7.00 per bushel is

1.0.

2.0.

2.6.

5.0.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- No chatgpt answerarrow_forwardTable 5.6 Quantity Supplied Price 10 $10 20 $20 30 $30 40 $40 50 $50 Refer to Table 5.6. If price decreases from $50 to $30, the price elasticity of supply is: Group of answer choices 10 5 0.5 2 1arrow_forward2) Calculate the price elasticity of demand for each price: VALUE KIND OF PRICE AMOUNT INCOME ELASTICITY ELASTICITY 7 4 6. 3 8 10 1. 12 14arrow_forward

- img' (a If po increases, what happens to the demand and supply of public transportation (shifts left/shifts right/doesn’t change) What happens to the equilibrium quantity and price for public transportation? (increase/decrease) (b)At a given price p, as oil becomes more expensive (po increases), does the (own) price elasticity of demand for public transportation increase / decrease / stay the same? (c) Calculate the cross-price elasticity of public transportation demand with respect to the oil price po, at the point p = 1 and po = 2. Are the two goods (public transportation and oil) substitutes or complements, or unrelated?arrow_forward11.) In the market for cars, the price elasticity of supply is +1.5, and the price elasticity ofdemand is -0.8. The equilibrium price is $ 30 thousand, and quantity is 120 million.(a) Assuming supply and demand are linear, reconstruct and draw the supply and demandcurves. Label the intercepts.(b) To reduce traffic, the government imposes a $400 tax on cars. What are PB and PS after thetax? What is the new equilibrium quantity? Illustrate them on the same graph.(c) How big is the change in consumer surplus, producer surplus, government revenue, anddeadweight loss?arrow_forwardPRICE (Dollars per unit) 140 50 20 0 Region Between W and X Between X and Y Between Y and Z W O True O False QUANTITY (Units) For each of the regions listed in the following table, use the midpoint method to identify if the demand for this good is elastic, (approximately) unit elastic, or inelastic. N O Elastic Inelastic Unit Elastic Demand (S. ? True or False: The value of the price elasticity of demand is equal to the slope of the demand curve.arrow_forward

- 5. Suppose that the price elasticity of the demand is 0.76. If we increase the price ofthe the demanded product, how would this affect the revenue? Explainarrow_forwardsuppose a pharmaceutical company considers increasing the price of insulin tm $125 per vial to $300 per vial. whenthe price was $125, the company sold 100, 000 vials per day. the company knows its price elasticity is .25. calculate thepercentage change in quantity demanded that would result in a price elasticity of .25. show your workarrow_forwardIn the figure below, what is the point price elasticity of demand when price is $60? 120 P Price ($) 100- 80 60 40 14 20- es Correct! Demand 0 200 400 600 800 1,000 1,200 Quantity O -0.50 -1.60 -2.00 -0.75 -1.00arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education