ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

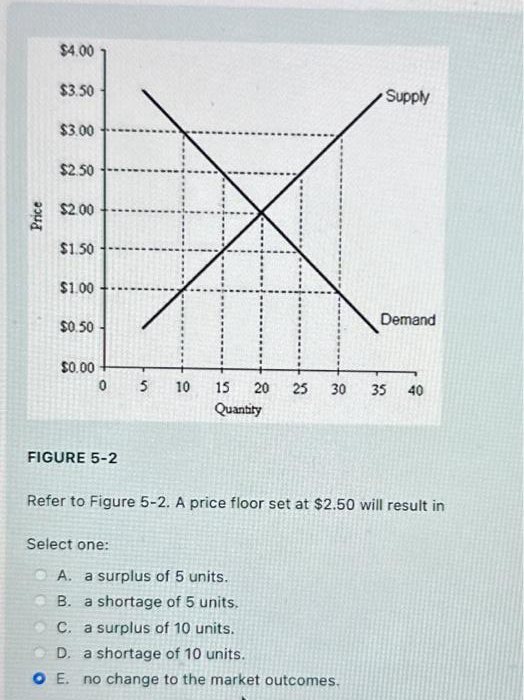

Transcribed Image Text:Price

$4.00

$3.50

$3.00

$2.50

$2.00

$1.50

$1.00

$0.50

$0.00

0

FIGURE 5-2

5

Select one:

10

15

Quantity

Supply

20 25 30 35

Demand

A. a surplus of 5 units.

B. a shortage of 5 units.

C. a surplus of 10 units.

D. a shortage of 10 units.

OE. no change to the market outcomes.

Refer to Figure 5-2. A price floor set at $2.50 will result in

40

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Price (dollars per gallon) 5.50 5.00 4,50 4.00 3.50 3.00 2.50 2.00 1.50 1.00 0.50 0 DNovember Djuly os 100 200 300 400 500 600 Quantity (gallons per day) 2. The graph above shows the demand and supply of ice cream in a small town in July and November. In July, the equilibrium price is $3.00 and the equilibrium quantity is 200 gallons of ice cream a day. In November, the equilibrium price is $2.50 and the equilibrium quantity is 100 gallons a day. a. What happens to consumer surplus and producer surplus in November compared to July? Calculate the amount of consumer/producer in November and July. b. Calculate the amount of total surplus in November and July.arrow_forwardWhat happens to the equilibrium price and quantity of gasoline during a severe hurricane in the Gulf of Mexico? A. Price decrease, Quantity decrease B. Price decrease, Quantity increase C. Price increase, Quantity decrease D. Price increase, Quantity increasearrow_forward3. Using the following schedule, define the equilibrium price and quantity. Describe the situation at a price of $10. What will occur? Describe the situation at a price of $2. What will occur? Quantity Demanded. Quantity Supplied Price 500 100 $ 1 $ 2 $ 3 $ 4 $ 5 400 120 350 150 320 200 300 300 Quantity Demanded Quantity Supplied Price $ 6 $ 7 $ 8 $ 9 275 410 260 500 230 650 200 800 $10 150 975 4. Suppose the government imposed a minimum price of $7 in the schedule of exercise 3. What would occur? Illustrate. 2 345arrow_forward

- 4. What will be the problem created in the following market if the price is $11.00? How will it be corrected? $12.00 11.00 10 00 Price 9.00 8.00 200 400 600 800 1000 1200 Quantityarrow_forwardA market price of $40 per dozen of roses will lead to a: a b C Price ($/dozen) 40 d 30 20 10 0 100 200 300 400 Select an answer and submit. For keyboard navigation, use the up/down arrow keys to select an answer. shortage of 200 dozens of red roses. surplus of 200 dozens of red roses. shortage of 100 dozens of red roses. Supply surplus of 100 dozes of red roses. Demand Quantity of Red Roses (dozens)arrow_forwardSupply and D Jayden Tu Problems Start Assignment Due Apr 13 by 11:59pm Points 10 Submitting a text entry box, a media recording, or a file upload Supply and Demand Problems Follow the directions to create graphs and explanations. 1. Looking at the market for Sacramento Kings Coffee Mugs: Draw supply and demand curves that follow the laws of supply and demand. Label the curves S and D, and label the equilibrium E. Also label the equilibrium quantity and equilibrium price. Suppose the abel the e Kings win the NBA championship, which is a big surprise, show what would happen on your graph (& labels) and explain it in words. demand will go up Supply will go up if they win everybody stuff. 'D' D Q Q' Quantity 2. Looking at the market for Wheaties cereal: Draw supply and demand curves that follow the laws of supply and demand. Label the curves S and D, and label the equilibrium E. Also label the equilibrium quantity and equilibrium price. cast ques up demand i Suppose the cost of wheat goes…arrow_forward

- Price (P) B $50 $30 Demand 800 1,200 Quantity (Q) In the figure above, when the price increases from point A to point B, the quantity effect on Total Revenue (the revenue loss from losing buyers who had been buying a lower price) is: Select one: а. — $16,000 b. - $4,000 c. - $12,000 d. - $10,000 Next pagearrow_forward2. Supply and Demand Schedules for A Gallon of Gasoline Price Quantity Supplied Quantity Demanded $4.00 $5.00 $6.00 $7.00 $8.00 6500 7000 7500 8000 8500 8000 7000 6000 5000 4000 Complete parts a, b, and c and either part d OR part e. a. Graph the supply and demand schedules in a supply curve and demand curve, respectively, on one graph. b. What are the equilibrium price and quantity? c. Show on your graph from part a and explain how the sanctions being placed upon Russia as a result of their actions in the Ukraine has affected the world market for the gallons of gasoline. Label what you did as R. d. If the government determined that the price for the gallon of gas in the marketplace should be set at $4.00, would this indicate that they were setting a price ceiling or a price floor? At this price of $4.00, how many gallons of gas will be soldarrow_forward4-5 Draw the price effect and the quantity effect for a price change from $60 to $70. Which effect is larger? Does total revenue increase or decrease? No calculation is necessary.arrow_forward

- The market for burritos in a college town is shown to the right. At a price of $7, how much excess demand is there? A. 0; there is excess supply at $7. B. 20 units C. 30 units D. 10 units C… Price 16- 14- 12- 10- 8- 6- 4- 2- 0 0 20 40 60 80 Quantity 100 S D 120 140 160arrow_forward(Figure: The Blu-ray Disc Rental Market) Use Figure: The Blu-ray Disc Rental Market. If the rental price of Blu-ray discs rises from $5 to $7: Question 2 options: v supply will increase from 50 to 70 rentals per weekend. the quantity demanded will decrease from 50 to 30 rentals per weekend. the quantity supplied will increase from 50 to 60 rentals per weekend. demand will decrease from 50 to 30 rentals per weekend.arrow_forwardPrice Supply $4 M 3 2 Demand 40 50 60 Quantity If the price starts out at $4, what will surely happen over time? a) The quantity supplied will fall, quantity demanded will rise and quantity sold will fall. b) The quantity supplied will fall, quantity demanded will rise and quantity sold will rise. c) The quantity supplied will fall, quantity demanded will fall and quantity sold will rise. d) The quantity supplied will rise, quantity demanded will fall and quantity sold will rise.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education