ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

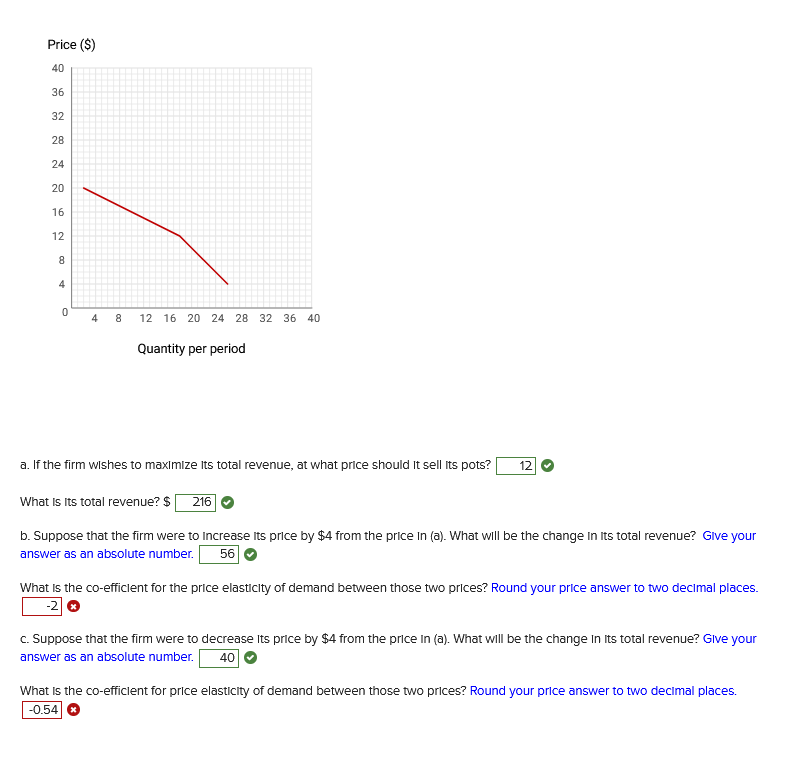

Transcribed Image Text:Price ($)

40

36

32

28

24

226

20

16

12

8

4

0

4

8

12 16 20 24 28 32 36 40

Quantity per period

a. If the firm wishes to maximize its total revenue, at what price should It sell its pots? 12

What is its total revenue? $ 216

b. Suppose that the firm were to increase its price by $4 from the price in (a). What will be the change in its total revenue? Give your

answer as an absolute number. 56

What is the co-efficient for the price elasticity of demand between those two prices? Round your price answer to two decimal places.

-2 Ⓡ

c. Suppose that the firm were to decrease its price by $4 from the price in (a). What will be the change in its total revenue? Give your

answer as an absolute number. 40

What is the co-efficient for price elasticity of demand between those two prices? Round your price answer to two decimal places.

-0.54

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 5 steps with 13 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Only typed answerarrow_forwardFarmer Lee grows strawberries. The average total cost and marginal cost of growing strawberries in the long run for an individual farmer are illustrated in the graph to the right. Suppose the market price is $7.05 per box. If so, then farmers will strawberries until the market price is $ number rounded to two decimal places.) per box. (Enter a numeric the market for a real enter exit Price and cost (dollars per box) 10- 9- 8- 5- 3- 2- 1. 0 MC ATC 10 20 30 40 50 60 70 80 90 100 Quantity of strawberries (boxes per week) oarrow_forwardA price-taking firm's variable cost function is VC = 20³, where Q is its output per week. It has a sunk fixed cost of $108 per week. Its marginal cost is MC = 6Q². a. What is the firm's supply function when the $108 fixed cost is sunk? Instructions: Enter your answer as a whole number. Q = (P/6) 0.5 for Pz $| b. What is the firm's supply function when the fixed cost is avoidable? Instructions: Enter your answer as a whole number. Q = (P/6) 0.5 for Pz $ 216 ✪ 0arrow_forward

- Consider a small landscaping company run by Mr. Viemeister. He is considering increasing his firm’s capacity. If he adds one more worker, the firm’s total monthly revenue will increase from $50,000 to $62,000. If he adds one more tractor, monthly revenue will increase from $50,000 to $58,000. Each additional worker costs $4,000 per month, while an additional tractor would also cost $4,000 per month. Instructions: Enter your answers as a whole number. a. What is the marginal revenue product of labor? $ The marginal revenue product of capital? $ b. What is the ratio of the marginal revenue product of labor to the price of labor (MRPL/PL)? : What is the ratio of the marginal revenue product of capital to the price of capital (MRPC/PC)? :arrow_forward①The total cost for producing x items is given by 12x + 3735. Each item is sold for $21. Find the formula for the total items must be sold to break even? revenue. How Many ②Solve the equation x² - 10x = -2x-15 3 A department store will buy 8 items if the price is $40 per item, and 14 items if the price is $28 per item. The Supplier is willing to sell 5 items if the price is $70 per item and 12 items if the price is $140 per item. If the supply and demand functions are linear, find the equilibrium point. invest $10,000 in an account that pays 10% compounded you continuously, how much money will you have in 15 years? (4) If ⑤ het f(x) = 300 √x + 2. Find the average rate of change when x increases from 25 to 100. Calculate derivatives of the following functions. a) 2 2x-3 4x+5 b) (2x5 +1) 9 ⑦Calculate derivatives of the following functions 8 の 2 6x в) че 6) 1) In (3x² + 5x) Calculate the following integral S (8x7 - 12x 5 + 3x² + 4) dxarrow_forward4 total cost is c(4, r, q) 5 total 75. If Firm A has constant marginal cost, and input prices double to 2r and 2w, how much will it cost to produce q 6 units of output (what is c(6, 2r, 2w))? (HINT: First calculate the marginal cost for c(q, r, w), then calculate c(6, r, w), and then calculate c(6, 2r, 2w)) = Firm A has cost function c(q, r, w). At output q = cost is c(5,r, q) ○ c(6, 2r, 2w) ○ c(6, 2r, 2w) = 90 ○ c(6, 2r, 2w) = 150 c(6, 2r, 2w) O c(6, 2r, 2w) = 180 - = - 75 160 = 60, and at output q -arrow_forward

- 8. A commodity has price demand function p(x)= 11800 - .01x and each unit costs 1000 and the overhead is 5000. a) what is the revenue function, cost function and profit function ? b) what price should be charged to maximize profits? c) what is the marginal profit for x=400 ? Explain what this marginal profit number means.arrow_forwardProve it! 2. If the demand function for products A and B is in the order Pa = 36 - 3Qa and Pb = 40 - 5Qb and the common cost function is TC = Qa' + 2QaQb + 3Qb². With the above information, then calculate: a. Production values A and B at the maximum or minimum profit levels. b. The maximum or minimum profit value Did the profit reach its maximum or minimum value? Prove it c.arrow_forwardThe following graph plots the marginal cost (MC) curve, average total cost (ATC) curve, and average variable cost (AVC) curve for a firm operating in the competitive market for jumpsuits. COSTS (Dollars) 80 72 64 56 24 16 8 0 0 8 0 MC ATC AVC Price (Dollars per jumpsuit) 4 8 12 36 48 60 ■ 16 24 32 40 48 56 QUANTITY (Thousands of jumpsuits) ☐ Quantity (Jumpsuits) 64 For every price level given in the following table, use the graph to determine the profit-maximizing quantity of jumpsuits for the firm. Further, select whether the firm will choose to produce, shut down, or be indifferent between the two in the short run. (Assume that when price exactly equals average variable cost, the firm is indifferent between producing zero jumpsuits and the profit-maximizing quantity of jumpsuits.) Lastly, determine whether the firm will earn a profit, incur a loss, or break even at each price. 72 80 Produce or Shut Down? Profit or Loss?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education