ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

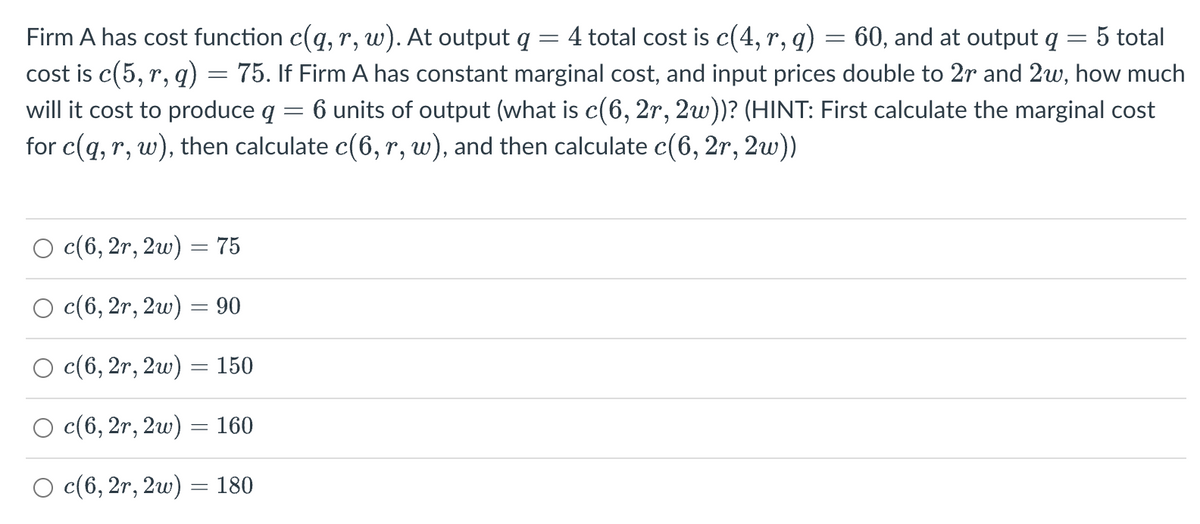

Transcribed Image Text:4 total cost is c(4, r, q)

5 total

75. If Firm A has constant marginal cost, and input prices double to 2r and 2w, how much

will it cost to produce q 6 units of output (what is c(6, 2r, 2w))? (HINT: First calculate the marginal cost

for c(q, r, w), then calculate c(6, r, w), and then calculate c(6, 2r, 2w))

=

Firm A has cost function c(q, r, w). At output q

=

cost is c(5,r, q)

○ c(6, 2r, 2w)

○ c(6, 2r, 2w) = 90

○ c(6, 2r, 2w) = 150

c(6, 2r, 2w)

O c(6, 2r, 2w) = 180

-

=

-

75

160

=

60, and at output q

-

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 11 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a firm with the following cost function: C (q) = 4q^2 + 100 Find the long-run supply and the short-run supply of the firm, under the assumptions that the total cost function is the same in the long and in the short run, but the xed cost is sunk in the short run.arrow_forwardSuppose you own an acre of land. You could grow crops on that land. The cost of seeds is $100. The crops you grow from those seeds will sell for $350. You could also rent the land to another farmer. The rent you could eam is $300. Calculate your economic profit. (Do not include a $ sign in your answer.) Answer: Suppose the total cost function for a firm is given by: TC= 100 + 2q +0.5q2. Find the marginal cost function and then use that to determine the marginal cost of the 10th unit. (Do not include a $ sign in your response.) # Answer:arrow_forwardThe cost function of a firm is c(y) = 3y^2 + 6y + 5.1. Find the Average variable and Marginal Cost curves of the firm.2. What is the quantity level where the average variable cost is minimized?arrow_forward

- Suppose the short-run production function for a restaurant producing a pack of food is given by: Q = 3L – 0.312 Where Q is the number of packs of food produced and L is the amount of labour used. If the cost of a unit of labour is ¢6 and the unit price of a pack of food produced is ¢10, a) what is the amount of labour the restaurant should employ in order to maximize profit. b) How much profit is made?arrow_forwardThe total cost of a firm is TC(Q)=3Q2+4Q+37. Suppose its current output level is 7. Find its ATC.arrow_forwardThe market for drones is perfectly competitive. Assume for simplicity that fractions of everything, including firms, is possible. We have identical firms, each with a Total Cost curve of TC=215+58q+q^2 and Marginal Cost curve MC=58+2q. Market demand is Q=744-2P. What is the Average Variable Cost if the firm produces 17 units?arrow_forward

- The ATC of a Firm is 25 when its output level is 21. The marginal cost producing the next unit is 33. Please find the ATC of the firm after it produces the next unit.arrow_forwardAssume a firm's short-run cost function is given by the following expression: C(q) = 2+q+q² - If the firm can sell each unit of their output at a price of p maximizing level of output in the short-run? Profit maximizing q = dollars, what is the firm's profitarrow_forwardHey need correct answerarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education