Related questions

Concept explainers

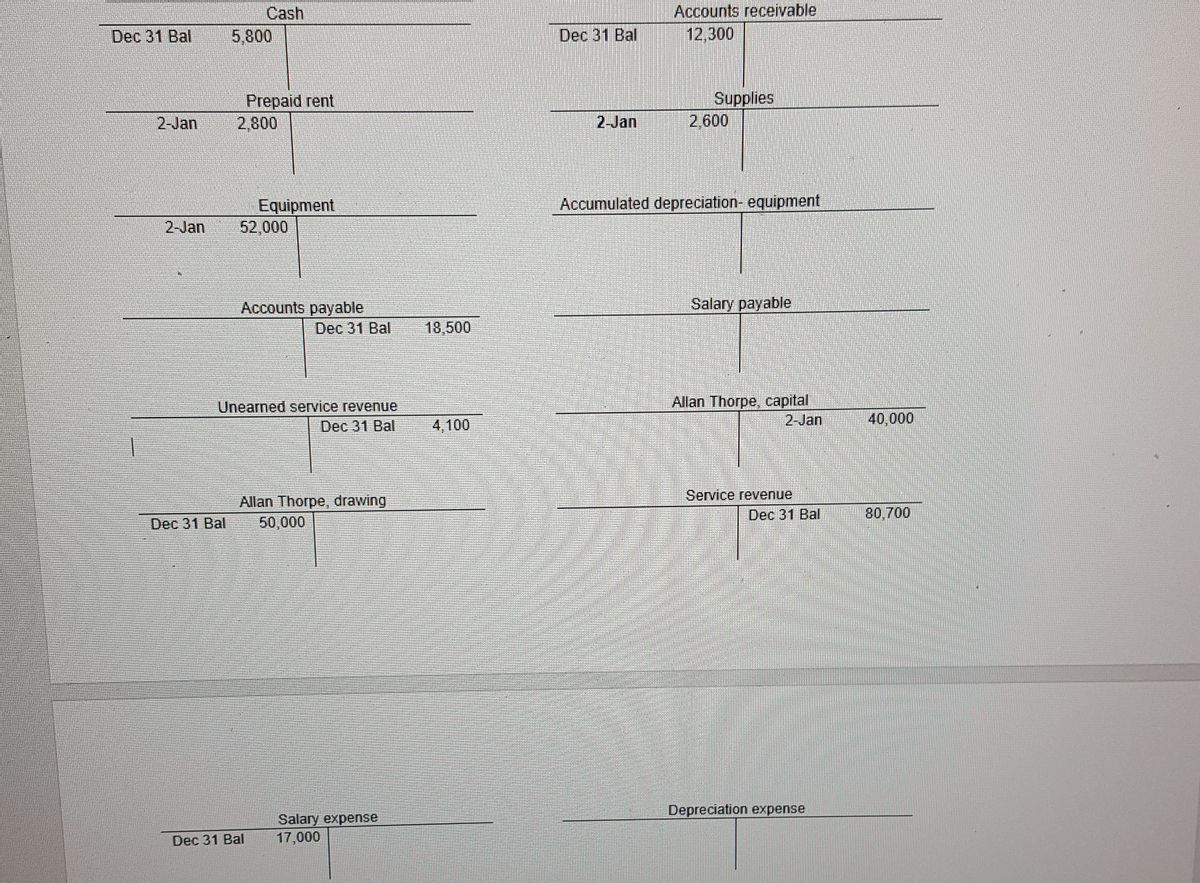

One year ago, Allan Thorpe founded Alcazar Sales Company, and the business has prospered. Allan comes to you for advice. He wishes to know how much net income the business earned during the past year. The accounting records consist of the T-accounts in the ledger, which were prepared by an accountant who has resigned from the company. The accounts at December 31, are as follows:

Allan indicates that, at year-end, customers owe him $1,000 accrued service revenue, which he expects to collect early next year. These revenues have not been recorded. During the year, he collected $4,100 service revenue in advance from customers, but the business has earned only $800 of that amount. During the year he has incurred $2,400 of advertising expense, but he has not yet paid for it. In addition, he has used up $2,100 of the supplies. Allan determines that

Allan expresses concern that drawing during the year might have exceeded the business’s net income. To get a loan to expand the business, Allan must show the bank that the business’s owner’s equity has grown from its original $40,000 balance. You and Allan agree that you will meet again in one week.

Requirement:

1.Prepare the

2. Prepare the adjusted

3. Prepare the 2019 company’s financial statements for presentation to the bank and to help address the first issue concerning Allan.

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 6 images

- The following are the transactions of Spotlighter, Incorporated, for the month of January. a. Borrowed $4,390 from a local bank on a note due in six months. b. Received $5,080 cash from investors and issued common stock to them. c. Purchased $1,900 in equipment, paying $650 cash and promising the rest on a note due in one year. d. Paid $750 cash for supplies. e. Bought and received $1,150 of supplies on account. Required: Post the effects to the appropriate T-accounts and determine ending account balances. Show a beginni Debit Beginning Balance Ending Balance Debit F Cash Equipment Credit Credit Debit Beginning Balance Ending Balance Debit Supplies Accounts Payablearrow_forwardIan bought some goods in May for $600 and sold them in the following August for $950.For the financial year ending on 30 June,which of the following statements is correct? A.Ian has expenses amounting to $600 B.Ian has assets of $600 C.Ian has revenues amounting to $950 D.Ian has a profit of $350arrow_forwardYou are the bookkeeper for Harley Inc., a newly formed corporation. Harley had the following transactions for their business: * Four shareholders contributed $40,000 ($10,000 each) in exchange for Harley common stock. * Harley purchased inventory for $5,000. Harley received an invoice for the inventory that is due in 30 days. What are the effects on Harley's accounting equation? A B D Based on the two transactions, Assets increased by $40,000, Liabilities decreased by $5,000 and Shareholder Equity increased by $45,000. Based on the two transactions, Assets increased by $45,000, Liabilities increased by $5,000 and Shareholder Equity increased by $40,000. C Based on the two transactions, Assets increased by $15,000, Liabilities increased by $5,000 and Shareholder Equity increased by $10,000. Based on the two transactions, Assets increased by $35,000, Liabilities decreased by $5,000 and Shareholder Equity increased by $40,000.arrow_forward

- Brian Sipe began operations of his business, Sipe Sons Incorporated, on January 1, Year One. During the year, the company performed services on credit of $192,000. Of that amount, $115,750 was collected in cash during the year. Brian estimates, of the remaining amount due, $5,100 may not be collected. Prepare the entries for the events during year one What is the balance in the accounts receivable account? What is the amount of receivables reported on the balance sheet? Why would Brian have a separate allowance account and not reduce the receivable balance for the amount estimated to e uncollectible? What type of account is Allowance for Doubtful Accountsarrow_forwardBob Jacobs wishes to expand his business and has borrowed $100,000. As a condition for making this loan, the bank requires that the business maintain a current ratio of at least 1.50. Business has been good but not great. The expansion costs have brought the current ratio down to 1.20 in the middle of December. Bob, as the owner of the business, is considering what might happen if he reports a current ratio of 1.4 to the bank. One possible action for Bob is to record in December $10,000 of revenue that the business will earn in January of next year. He thinks this is doable because the contract for this job has been signed. Journalize the revenue transaction and indicate how recording this revenue in December would affect the current ratio. Discuss whether it is ethical to record the revenue transaction in December. Identify the accounting principle relevant to this situation. and give the reasons underlying your conclusion. Propose an ethical action for Bob Jacobs.arrow_forwardA bookstore is incorporated at the beginning of the year, so all entries of balance sheet are zero at the beginning of the year (Jan. 1). David invests $5,000 at the beginning of the year and withdraws $5,000 at the end of the year. The bookstore buys books worth $5,000. The bookstore sells all of the books for $15,000 (cash) during the year. The bookstore incurs operating expense of $3,000 to pay utilities. At the beginning of the year, the bookstore borrows $5,000 whose interest rate is 40% at the beginning of the year. The bookstore pays interest and principal at the end of the year. The tax rate is 20% . What is the firm value at the end of the year? Question 5 options: $ 1,000 $2,000 $3, 000 $4,000 Can not be determinedarrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education