ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

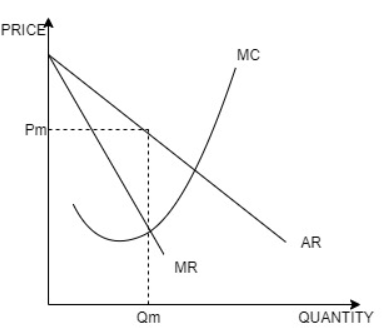

Transcribed Image Text:On a diagram with quantity on the horizontal axis and price on the vertical axis, the short run per unit profit for a monopolist is

a. a vertical distance.

b. the area of a rectangle.

c. a horizontal distance.

d. area of a triangle.

Expert Solution

arrow_forward

Step 1

In a monopoly profit is maximized at the point where the marginal revenue curve intersects the marginal cost curve. And that quantity is the quantity produced by the monopoly.

For monopoly, the profit is:

Profit=(Pm×Qm)-TC

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The graph below depicts the demand curve facing a monopolist. The monopoly has constant marginal costs of $5. On the graph: A). Use the straight line tool to draw the marginal revenue curve. B) use the straight line tool to draw the marginal cost curve up to 60 units of output C) use the point tool to plot the profit maximization point on the demand curve.arrow_forwardO Macmillan Learning (Figure: Determining Monopolist Profit) Based on the graph, the profit-maximizing price is at point Price and Cost h Of. O g. d. C MR Output MC ATCarrow_forwardNonearrow_forward

- Figure 15-7 Price $20 15 10 ● 100 150 Figure 15-8 200 Marginal Cost Demand Quantity Refer to Figure 15-7. To maximize its profit, which outcome would a monopolist choose? Marginal Revenue a. 100 units of output and a price of $10 per unit * b. 100 units of output and a price of $20 per unit C. 150 units of output and a price of $15 per unit d. 200 units of output and a price of $10 per unit polist ?arrow_forwardHow do you graph this Consumer surplus and Deadweight Lossarrow_forwardQUESTION 12 The table below shows a monopolist's demand curve and the cost information for the production of its good. What will their profits equal? Quantity Price per UnitTotal Cost 10 $100 20 $80 $60 $40 $20 O 30 40 50 a. $600 O b. $1,200 O c. $1,600 O d. $1,000 $100 $400 $800 $1,400 $2,400arrow_forward

- If a monopolist with significant barriers to entry is making positive economic profit in the short run, what do we expect to happen as the market transitions to the long run? O The profit will increase since the monopolist has no competition, they can just raise the price to earn higher profits. O It will decrease as positive economic profit signals new firms to enter the market, increasing the market supply, and lowering the prevailing price. O It will increase, in the long run firms will drop out the market increasing the monopolists dominance in the marketplace. O The profit will stay the same, strong barriers to entry prevent new competition.arrow_forwardQUESTION 23 If the monopolist shown in the following figure could practice first-degree price discrimination, the producer surplus would be: Price (dollars) 50 40 30 20 10 $0. $225. $450. $900. O $1,200. 30 50 60 MR 100 MC Quantityarrow_forwardQuestion 30 Demand: P=120-Q Marginal Revenue: MR=120-2Q Total Cost: TC=Q² Marginal Cost: MC=2Q For this monopolist, the profit-maximizing price is and the profit-maximizing quantity is 90, 30 30, 90 40, 80 None of these answers O O Oarrow_forward

- 3. Suppose that a monopoly has the following demand curve and total costs: 오 P TR TC ATC MC MR Total Profit 50 40 1 45 50 2 40 72 - 3 35 95 - 4 30 125 - 25 165 6 20 225 a. Fill in the blanks in the preceding table. b. What output will maximize the monopolist's profit? c. What price will the monopolist choose?arrow_forwardIf a monopolist faces an inverse demand curve, p(y) = 100-2y and has constant marginal costs of $32 and zero fixed costs and if this monopolist is able to practice perfect price discrimination, its total profits will be O a. $1,156. O b. $17. O c. $578. O d. $1,734. O e. $289.arrow_forwardanswer quicklyarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education