ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

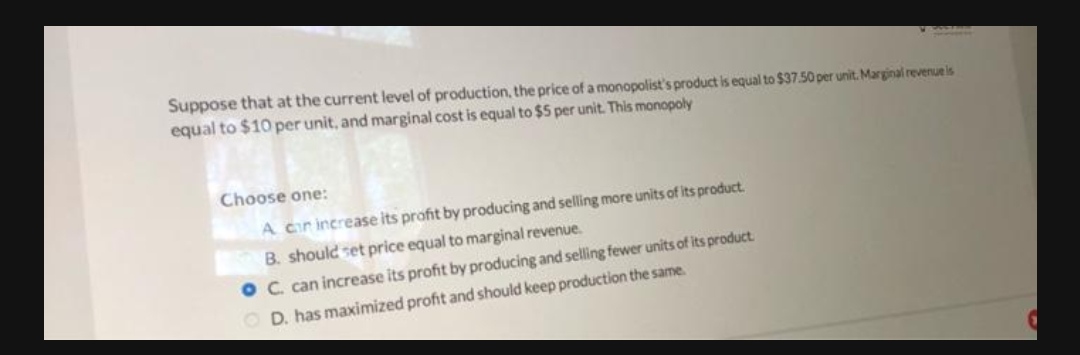

Transcribed Image Text:Suppose that at the current level of production, the price of a monopolist's product is equal to $37.50 per unit. Marginal revenueis

equal to $10 per unit, and marginal cost is equal to $5 per unit. This monopoly

Choose one:

A cir increase its profit by producing and selling more units of its product.

B. should set price equal to marginal revenue.

C. can increase its profit by producing and selling fewer units of its product.

O D. has maximized profit and should keep production the same.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Over a recent family dinner, your Aunt Trudy expresses her disdain for price discriminating monopoly businesses, to which you, having taken some economics reply, "A perfect price discriminating monopoly may convert all of the consumer surplus to monopoly profit, but at least it produces O A. more output than a competitive industry would produce. OB. the same output that a competitive industry would produce. C. at the minimum of its average total cost (ATC) curve. D. where its marginal cost (MC) curve is still declining.arrow_forwardHow much is the maximum profit a monopolist can earn? TC 10 15 25 40 60 Q 0 1 2 34 Select one: O a. 11 O b. 9 O c. 19 O d. 15 Price 40 30 20 10 0arrow_forwardMC Price AC AR 2345 MR Quantity The diagram above represents a monopoly firm. At which output level will the monopolist maximize profits? O A. Output level 3 B. Output level 4 O C. Output level 1 O D. Output level 5arrow_forward

- describe(s) a type of barrier to entry for a monopoly in which one firm can operate more efficiently than two or more firms. O A. Copyrights B. Patents C. Economies of scale D. Price discriminationarrow_forwardSuppose the table below describes the relationship between price and quantity demanded for a monopolist. Quantity 1 2 3 4 5 6 7 8 O If the marginal cost of producing each unit of output is $5, then this monopolist maximizes its profit by charging __________ per unit. O $8 $5 $3 Price $10 $9 $8 $7 $6 $5 $4 $3 $6arrow_forwardIn which of the following situations would the quantity supplied to the market increase? A price ceiling O below the competitive equilibrium price in a competitive market. above the unregulated monopolist price, but above the fırm's average total cost for a natural monopoly. none of the other answers are correct. A price ceiling never increases the quantity supplied to a market. O below the unregulated monopolist price, but above the firm's average total cost for a natural monopoly. above the competitive equilibrium price in a competitive market.arrow_forward

- 19 Which of the following describes how a natural monopoly is graphically illustrated? A When producing small quantities, the demand is higher than long-run average cost. BO The long-run average cost curve is U-shaped. CO When producing large quantities, the long-run average cost is greater than demand. The demand curve intersects the long-run average cost curve at a point where the long-run average cost curve is downward sloping. Darrow_forwardplease show me complete and neat solution thank youarrow_forwardAnswer fast pls...arrow_forward

- 8. Can a monopolist that is not subject to any regulation lead the market to Pareto efficiency by his own initiative? Pareto efficiency is a situation that cannot be modified so as to make any one individual better off without making at least one individual worse off. In the model of monopoly, we assume that the ultimate goal of a monopolist is to maximize his profit, which means MC-MR. We have seen (for example, in the lecture or earlier problems, e.g., problem 5) that this equality leads the monopolist to produce less and charge a higher price than in perfect competition. This makes the monopolist better off but at the same time makes consumers worse off, as compared to perfect competition. This also leads to a deadweight loss. As we have the deadweight loss, the monopoly is definitely not Pareto efficient. See the lecture slide # 37. The transactions between Qm and Qk (quantities supplied in the monopoly and perfect competition, respectively) could take place to everyone's benefit,…arrow_forward7arrow_forward47 and 48arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education