ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:NAME

PRINT LAST NAME, FIRST NAME

SECTION#

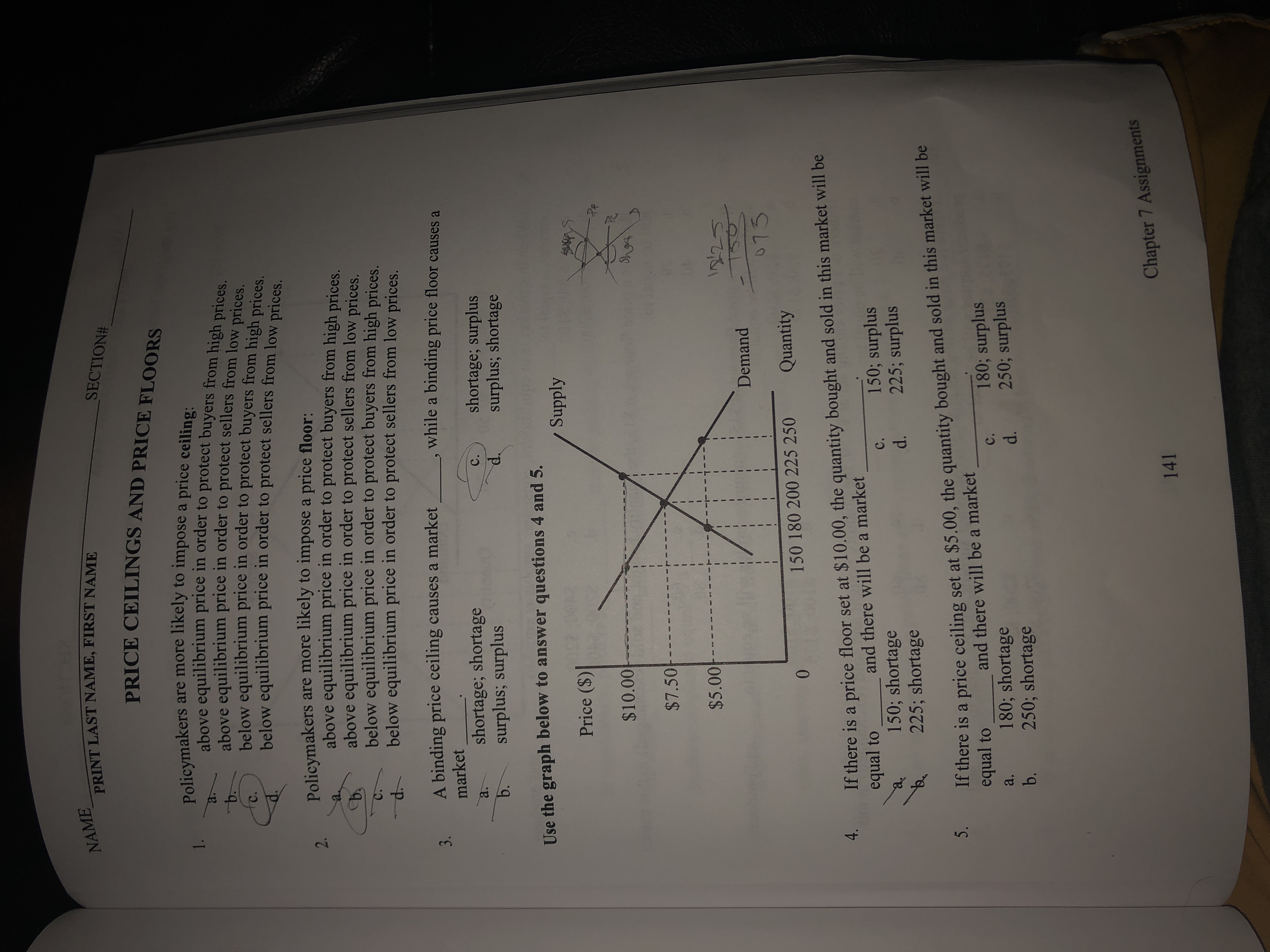

PRICE CEILINGS AND PRICE FLOORS

Policymakers are more likely to impose a price ceiling-

above equilibrium price in order to protect buyers from high prices.

above equilibrium price in order to protect sellers from low prices.

below equilibrium price in order to protect buyers from high prices

1.

b.

C.

below equilibrium

price in order to protect sellers from low

prices.

Policymakers are more likely to impose a price floor:

above equilibrium price in order to protect buyers from high prices.

above equilibrium price in order to protect sellers from low prices.

below equilibrium price in order to protect buyers from high prices.

below equilibrium price in order to protect sellers from low prices.

2.

a.

C.

3. A binding price ceiling causes a market

while a binding price floor causes a

market

shortage; shortage

surplus; surplus

b.

shortage; surplus

surplus; shortage

C.

Use the graph below to answer questions 4 and 5.

Supply

Price ($)

$10.00

$7.50

0000

150

073

Demand

150 180 200 225 250

Quantity

0.

If there is a price floor set at $10.00, the quantity bought and sold in this market will be

equal to

and there will be a market

c.

150; shortage

225; shortage

150; surplus

225; surplus

d.

3. If there is a price ceiling set at $5.00, the quantity bought and sold in this market will be

equal to

and there will be a market

180; surplus

250; surplus

d.

c.

180; shortage

250; shortage

a.

b.

Chapter 7 Assignments

141

Transcribed Image Text:SECTION#

NAME

PRINT LAST NAME, FIRST NAME

NAME

PE

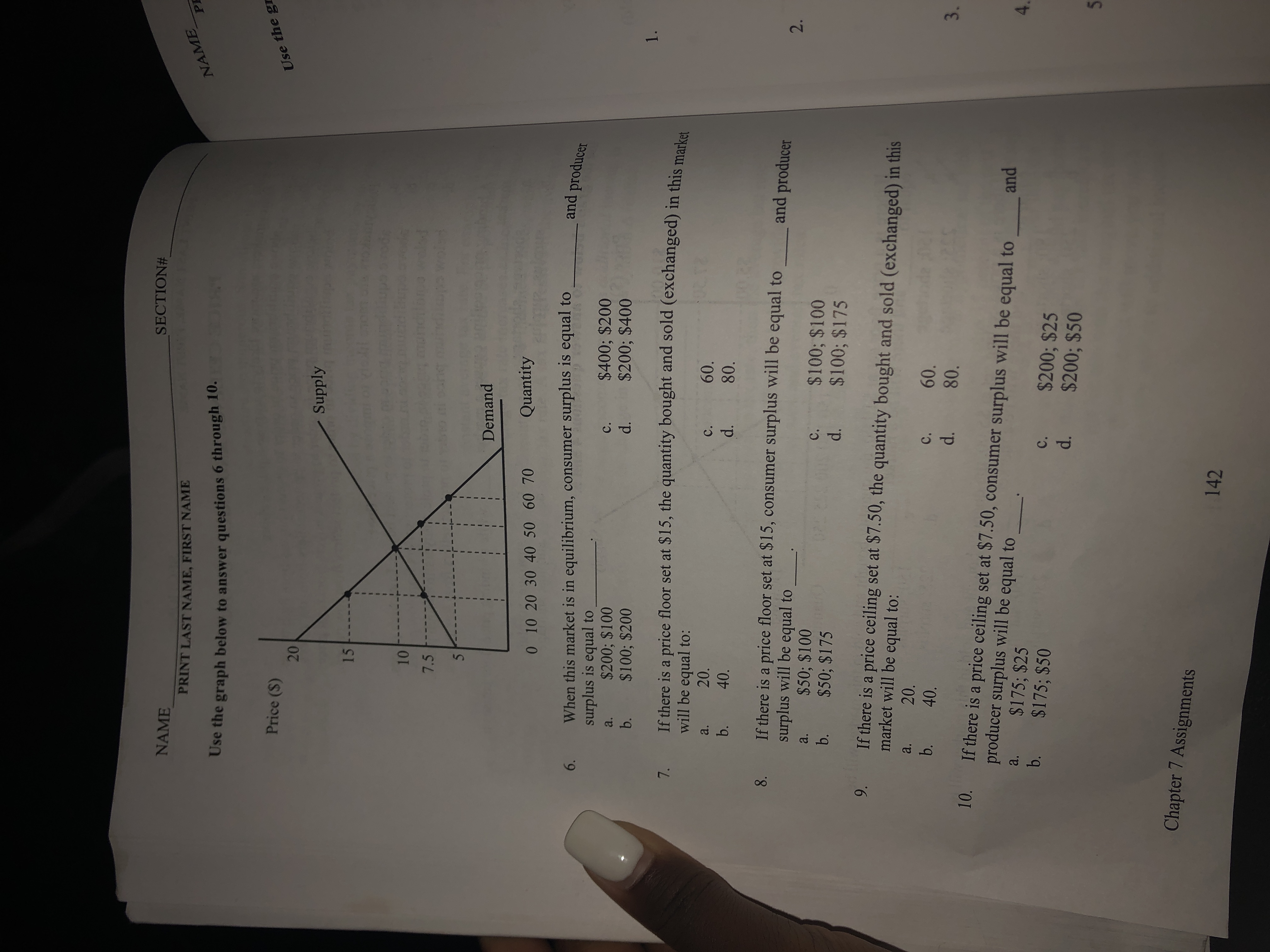

Use the graph below to answer questions 6 through 10.

Price (S)

Use the gr

- Supply

15

10

7.5

Demand

Quantity

0 10 20 30 40 50 60 70

When this market is in equilibrium, consumer surplus is equal to

surplus is equal to

$200; $100

$100; $200

and producer

6.

$400; $200

$200; $400

C.

a.

d.

b.

1.

If there is a price floor set at $15, the quantity bought and sold (exchanged) in this meala

will be equal to:

7.

20.

a.

60.

C.

b.

40.

d.

80.

If there is a price floor set at $15, consumer surplus will be equal to

surplus will be equal to

$50; $100

$50; $175

and producer

a.

$100; $100

$100; $175

C.

b.

d.

If there is a price ceiling set at $7.50, the quantity bought and sold (exchanged) in this

market will be equal to:

9.

20.

a.

b.

60.

C.

40.

d.

80.

3.

10. If there is a price ceiling set at $7.50, consumer surplus will be equal to

producer surplus will be equal to

$175; $25

b. $175; $50

and

a.

$200; $25

$200; $50

c.

d.

Chapter 7 Assignments

142

2.

20

8.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- 9arrow_forwardHow would each event affect the market for COVID-19 vaccines? Does the event cause a change in demand or a change in the quantity demanded? Is the change positive or negative? Or does the event cause a change in supply or a change in the quantity supplied? Is the change positive or negative? Explain the mechanism for the change and what happens to equilibrium price and quantity. a) The vaccine is approved for children under the age of 12. b) The U.S. government provides a subsidy that allows the price of the vaccine to be $0 for everyone. c) Several vaccines pass Phase 3 (large-scale efficacy tests) and are approved by the FDA for full use. d) A truck carrying the Pfizer vaccine has a malfunction and the refrigeration requirements aren’t met, so all the doses go bad. e) School districts and health care facilities add a requirement for getting the vaccine for all employees.arrow_forwarddo fast.arrow_forward

- Imagine that the government wages a major war on illicit drugs. Assuming that both at the point of initial and new market equilibria demand for illicit drugs is INELASTIC, what should happen to the amount of money that the drug dealers are getting from selling the drugs if the government measures are successful and the supply of illicit drugs at the market drops? The amount of money received by the drug dealers goes up The amount of money received by the drug dealers goes down The amount of money received by the drug dealers does not changearrow_forwardQ10.arrow_forwardWhat are the side effects of price ceilings? How might price ceilings affect the supply of goods and services that are subject to the price ceilings? Do you agree or disagree with price ceilings? Why or why not? Do you agree or disagree with laws against price gouging? Why or why not?arrow_forward

- Consider the market for corn. Suppose that right now, the equilibrium price is considered “too low” by farmers (i.e. suppliers) in order to make a living. These farmers go to their state representatives and convince them to enact a price floor that is above the equilibrium price. Depict this situation graphically. Is there a shortage or a surplus (or does nothing happen)? Now, conceptually, describe how we know with certainty, that consumers are harmed by this policy. Then, describe conceptually how farmers may be harmed or may benefit from this policy. Graphically depict how we know that consumers are harmed while farmers may be better or worse off (ambiguous). If we were to consider the “total surplus” of consumers and farmers, can we say with certainty whether this economy is better or worse off from the price floor?arrow_forward12. Market equilibrium and disequilibrium The following graph shows the monthly demand and supply curves in the market for calendars. Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. Graph Input Tool 100 Market for Calendars 90 Price (Dollars per calendar 30 Supply Quantity Demanded (Calendars) Quantity Supplied Calendars) 500 80 50 40 Demand 100 150 200 250 300 350 400 450 800 OIANTITY Calendars 803 PM arch. PRICE (Dollars per calendar)arrow_forwardUse the accompanying graph to answer these questions. 20 S sº Price of X ($) 18 16 14 12 10 8 6 4 2 0 1 2 3 4 Quantity of Good X units 5 6 D a. Suppose demand is D and supply is SO. If a price ceiling of $6 is imposed, what are the resulting shortage and full economic price? Shortage: Full economic price: $ b. Suppose demand is D and supply is SO. If a price floor of $12 is imposed, what is the resulting surplus? What is the cost to the government of purchasing any and all unsold units? Surplus: Cost to government: $ c. Suppose demand is D and supply is so so that equilibrium price is $10. If an excise tax of $6 is imposed on this product, what happens to the equilibrium price paid by consumers? The price received by producers? The number of units sold? Fauilibrium price paid by consumers $1arrow_forward

- 10. Price controls in the Florida orange market The following graph shows the annual market for Florida oranges, which are sold in units of 90-pound boxes. Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. Graph Input Tool Market for Florida Oranges 50 I Price (Dollars per box) 45 Supply 20 40 Quantity Demanded (Millions of boxes) Quantity Supplied (Millions of boxes) 486 360 35 30 25 20 bemand 15 10 5 90 180 270 360 450 540 630 720 810 900 QUANTITY (Millions of boxes) PRICE (Dollars per box)arrow_forwardi will urgent 10 upvotes. In the market shown in the figure, if a price ceiling of 10 is imposed, the shortage is _______arrow_forwardG.237.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education