MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

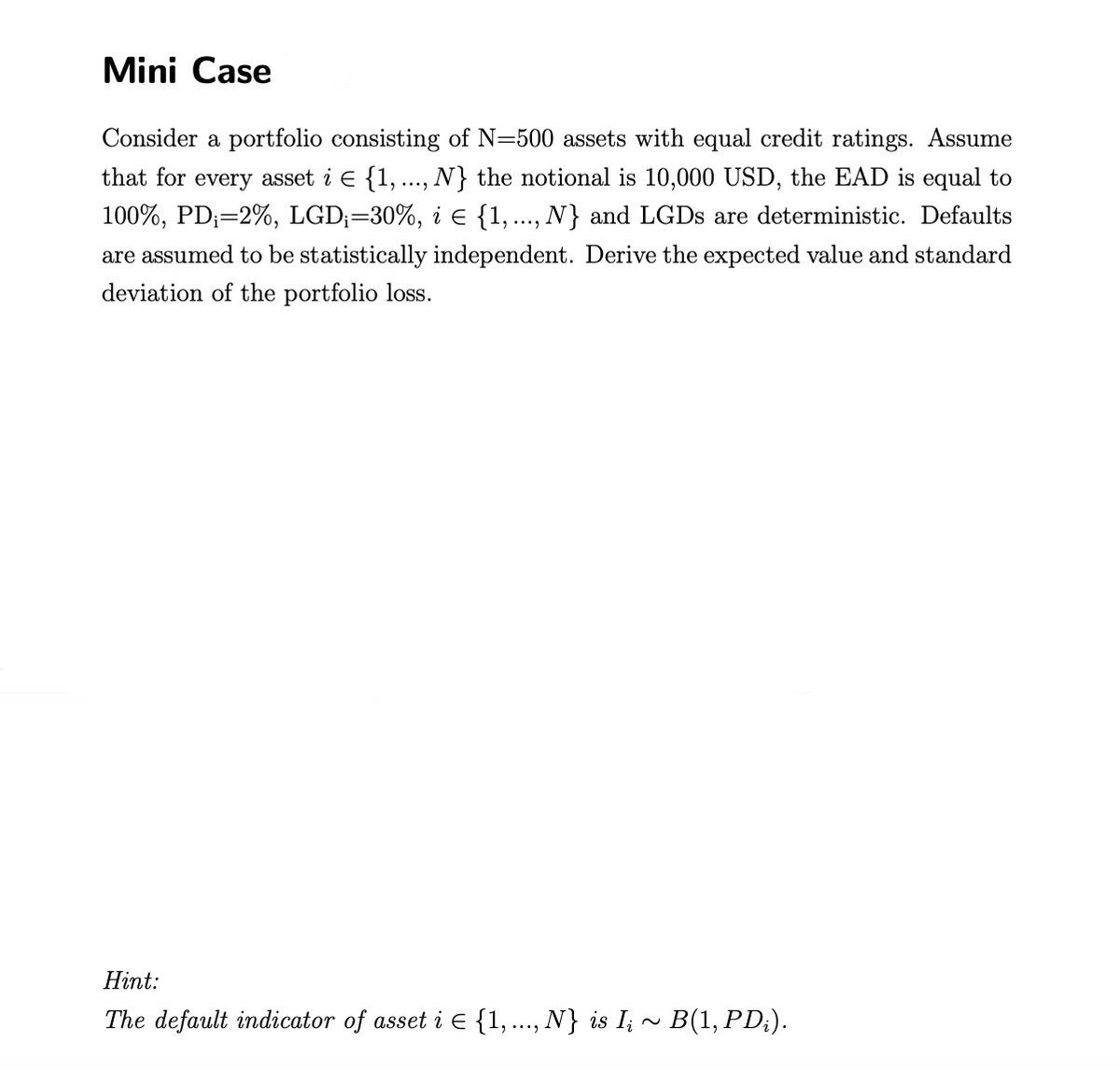

Transcribed Image Text:Mini Case

Consider a portfolio consisting of N-500 assets with equal credit ratings. Assume

that for every asset i E {1, ..., N} the notional is 10,000 USD, the EAD is equal to

100%, PD;=2%, LGD;=30%, i € {1,..., N} and LGDs are deterministic. Defaults

are assumed to be statistically independent. Derive the expected value and standard

deviation of the portfolio loss.

Hint:

The default indicator of asset i E {1,..., N} is Iį ~ B(1, PD;).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 8 images

Knowledge Booster

Similar questions

- Consider the following data: Stock M N Average return 26% 16% Risk (Std. Dev.) 20% 10% If the return on stocks M and N are perfectly negatively correlated, what is the range of risk (std dev) associated with all possible portfolio combinations? A. Range of the risk: between 0= risk s10 % OB. Range of the risk: between 0 < risk 10% OC. Range of the risk: between 5% and 10%. OD. Range of the risk (std. dev): between 15% to 20% OE. None of the abovearrow_forwardThe lowest portfolio risk will result when the asset returns are perfectly positively correlated. Select one: True Falsearrow_forwardConsider an auto insurance portfolio where the number of accidents follows a Poisson distribution with parameter λ= 1000. Suppose the damage sizes for separate accidents are i.i.d. (independent identically distributed) r.v.'s having an exponential distribution with a mean of $2500. Each policy involves a deductible of $500. Let N₁ be the number of accidents that result in claims, and N₂ be the number of accidents that do not result in claims. Answer the following questions 1-5. Q1 Are N₁, N₂ dependent? Q2 Depends on a situation, No Yes What is the name of the distributions of N₁, №₂? O Marked Poisson Gamma Exponential Compound Poissonarrow_forward

- Q4. Assume that daily evaporation rates (E) have a uniform distribution with a = 0 and b = 0.35 in/day. Determine the following probabilities: (a) P(E > 0.1); (b) P(E < 0.22); and (c) P(E = 0.2).arrow_forwardA survey is conducted on 700 Californians older than 30 years of age. The study wants to obtain inference on the relationship between years of education and yearly income in dollars. The response variable is income in dollars and the explanatory variable is years of education. A simple linear regression model is fit, and the output from R is below: Im(formula = Income ~ Education, data = CA) Coefficients: Estimate Std. Error t value Pr(>|t|) (Intercept) 25200.25 1488.94 16.93 3.08e-10 *** Education 2905.35 112.61 25.80 1.49e-12 *** Residual standard error: 32400 on 698 degrees of freedom Multiple R-squared: 0.7602arrow_forwardA company manager plans to purchase a machine. The company requires a high quality machine. The manager is currently considering two companies that supply this machine. The machine from company A can produce approximately1050 units in average per day, but the standard deviation of this machine is about 250 units per day; while the machine from company B can produce approximately 900 units in average per day, but the standard deviation of this machine is about 100 units per day. Both of these two companies guarantee at least 10 years life. In addition, both prices are similar although machine A is a little bit higher. Price is not the main concern for the manager because both prices are under their budget. However, the manager cannot decide which machine should be purchased, because he is not sure what test he needs to conduct. Can you recommend the manager what test the manager should conduct? Should the manager conduct the test about the difference between two population means or the…arrow_forward

- Chains "A" and "B" are made of the same steel. "A" consists of three links and "B" consists of six links, each link having a normal distribution function of the resisting strength with a mean of 60,000 psi and standard deviation of 5,000 psi. Determine which chain is generally weaker (from a probabilistic point of view) by plotting the probability distribution functions of their resisting strengths on the same diagram.arrow_forwardIn finance, one example of a derivative is a financial asset whose value is determined (derived) from a bundle of various assets, such as mortgages. Suppose a randomly selected mortgage in a certain bundle has a probability of 0.06 of default. (a) What is the probability that a randomly selected mortgage will not default? (b) What is the probability that four randomly selected mortgages will not default assuming the likelihood any one mortgage being paid off is independent of the others? Note: A derivative might be an investment that only pays when all four mortgages do not default. (c) What is the probability that the derivative from part (b) becomes worthless? That is, at least one of the mortgages defaults. (a) The probability is (Type an integer or a decimal. Do not round.)arrow_forwardCholesterol is a fatty substance that is an important part of the outer lining (membrane) of cells in the body of animals. Suppose that the mean and standard deviation for a population of individuals are 180 mg/dl and 20 mg/dl, respectively. Samples are obtained from 25 individuals, and these are independent. (a) What is the probability that the average of the 25 measurements exceeds 185 mg/dl? (b) Determine symmetric limits around 180 such that the probability that the sample average is within the limits equals 0.95.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman