FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

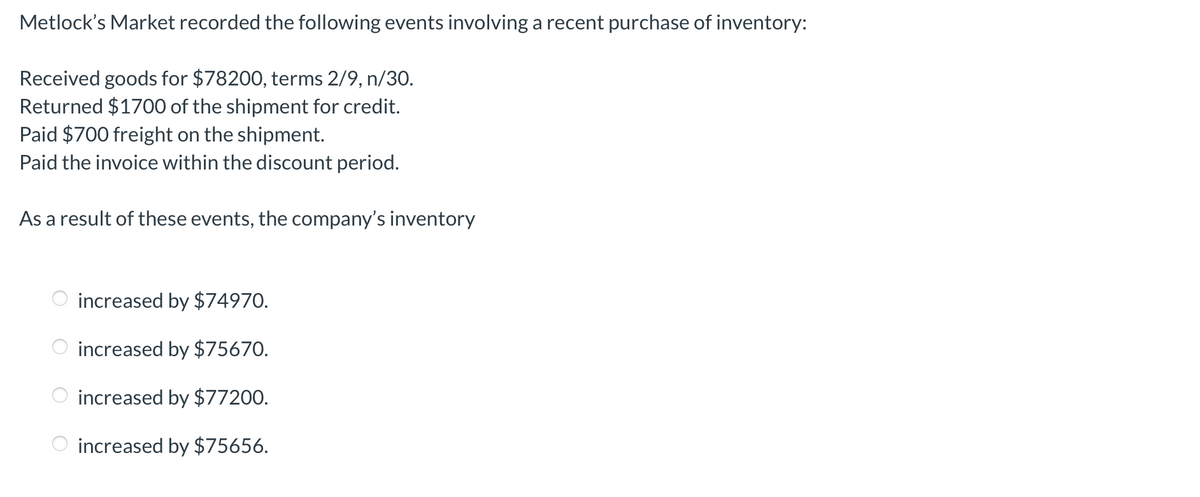

Transcribed Image Text:Metlock's Market recorded the following events involving a recent purchase of inventory:

Received goods for $78200, terms 2/9, n/30.

Returned $1700 of the shipment for credit.

Paid $700 freight on the shipment.

Paid the invoice within the discount period.

As a result of these events, the company's inventory

increased by $74970.

increased by $75670.

increased by $77200.

O increased by $75656.

O O

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Raleigh Department Store uses the conventional retail method for the year ended December 31, 2022. Available information follows: a. The inventory at January 1, 2022, had a retail value of $49,000 and a cost of $34,380 based on the conventional retail method. b. Transactions during 2022 were as follows: Gross purchases Purchase returns Purchase discounts Sales Sales returns Employee discounts Freight-in Net markups Net markdowns Cost $ 323,040 6,300 5,400 Beginning inventory 28,500 Sales Sales returns Employee discounts Estimated ending inventory at retail Estimated ending inventory at cost Retail $530,000 14,000 Sales to employees are recorded net of discounts. c. The retail value of the December 31, 2023, inventory was $85,330, the cost-to-retail percentage for 2023 under the LIFO retail method was 69%, and the appropriate price index was 106% of the January 1, 2023, price level. d. The retail value of the December 31, 2024, inventory was $52,320, the cost-to-retail percentage for…arrow_forwardCARDO Company suspects that there is missing inventory in its warehouse at December 31, 2021. All sales and purchases were made on account. Also, the gross profit rate based on net sales is consistent every year. To aid in your investigation, you obtained the following: How much is the cost of sales based on the historical gross profit rate?arrow_forwardAt the beginning of the current period, Penny Worth Corporation had balances in Accounts Receivable of $176,000 and in Allowance for Expected Credit Losses of $8,000 (credit). During the period, Penny Worth had credit sales of $704,000 and collections on account of $671,600. Penny Worth expects a return rate of 5%. Penny Worth uses a perpetual inventory system and determined that the cost of goods sold during the period was $589,600. Penny Worth wrote off as uncollectible, accounts receivable of $6,400. However, a $2,800 account previously written off as uncollectible was recovered before the end of the current period. Uncollectible accounts are estimated to total $22,000 at the end of the period. (a) Prepare the entries to record sales, cost of goods sold, and collections during the period. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the…arrow_forward

- [The following information applies to the questions displayed below.] Autumn Company began the month of October with inventory of $25,000. The following inventory transactions occurred during the month: The company purchased inventory on account for $37,000 on October 12. Terms of the purchase were 2/10, n/30. Autumn uses the net method to record purchases. The inventory was shipped f.o.b. shipping point and freight charges of $600 were paid in cash. On October 31, Autumn paid for the inventory purchased on October 12 During October inventory costing $19,500 was sold on account for $30,000. It was determined that inventory on hand at the end of October cost $42,360. Assuming Autumn Company uses a periodic inventory system, prepare journal entries for the above transactions including the adjusting entry at the end of October to record cost of goods sold. Autumn considers purchase discounts lost as part of interest expense.arrow_forwardNeed all answer'sarrow_forward[The following information applies to the questions displayed below.] Autumn Company began the month of October with inventory of $33,000. The following inventory transactions occurred during the month: The company purchased inventory on account for $49,000 on October 12. Terms of the purchase were 210/210 , n30/�30 . Autumn uses the net method to record purchases. The inventory was shipped f.o.b. shipping point and freight charges of $680 were paid in cash. On October 31, Autumn paid for the inventory purchased on October 12. During October inventory costing $20,700 was sold on account for $31,600. It was determined that inventory on hand at the end of October cost $61,000. 1. Assuming Autumn Company uses a perpetual inventory system, prepare journal entries for the above transactions. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education