Principles of Economics 2e

2nd Edition

ISBN: 9781947172364

Author: Steven A. Greenlaw; David Shapiro

Publisher: OpenStax

expand_more

expand_more

format_list_bulleted

Question

The young and beautiful expert Hand written solution is not allowed please

Transcribed Image Text:Mc

Saved

Help

Save & Exit

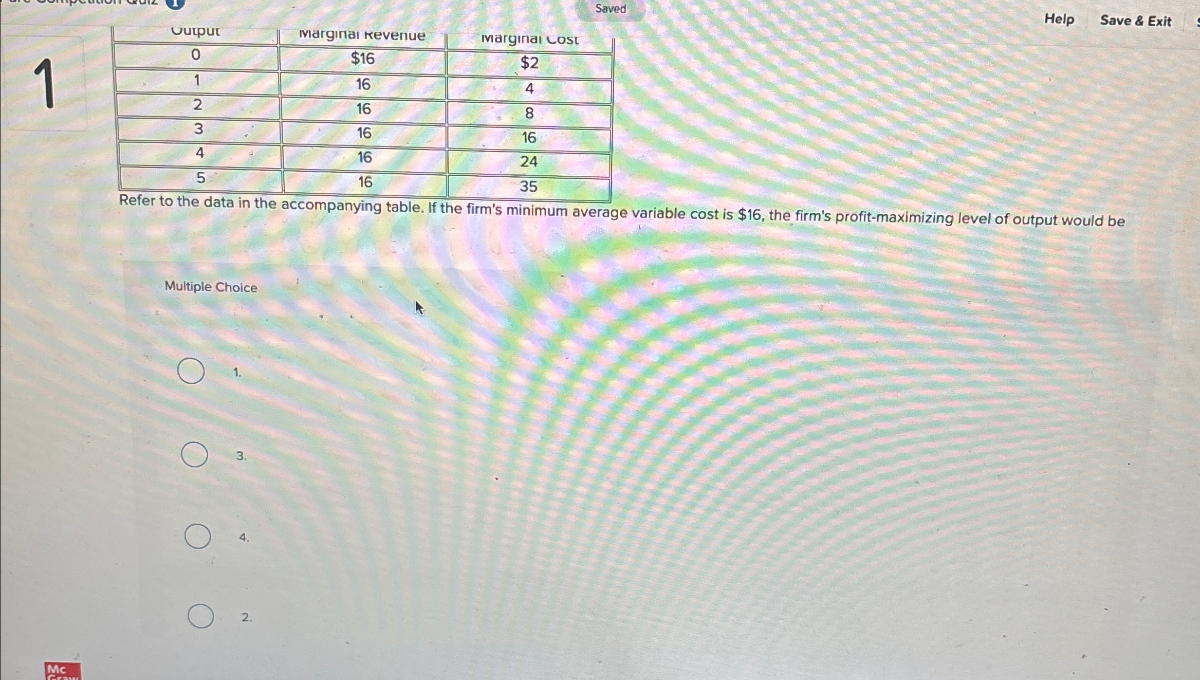

Output

Marginal Revenue

Marginal Cost

$16

$2

1

1

16

4

2

16

8

3

16

16

24

5

35

16

16

Refer to the data in the accompanying table. If the firm's minimum average variable cost is $16, the firm's profit-maximizing level of output would be

Multiple Choice

O

O

3.

4.

2.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- A computer company produces affordable, easy-to-use home computer systems and has fixed costs of 250. The marginal cost of producing computers is 700 for the first computer, 250 for the second, 300 for the third, 350 for the fourth, 430 for the fifth, 450 for the sixth, and 500 for the seventh. Create a table that shows the companys output, total cost, marginal cost, average cost, variable cost, and average variable cost. At what price is the zero-profit point? At what price is the shutdown point? If the company sells the computers for 500, is it making a profit or a loss? How big is the profit or loss? Sketch a graph with AC, MC, and AVG curves to illustrate your answer and show the profit or loss. If the firm sells the computers for 300, is it making a profit or a loss? How big is the profit or loss? Sketch a graph with AC, MC, and AVG curves to illustrate your answer and show the profit or loss.arrow_forwardHow would an improvement in technology, like the high-efficiency gas turbines or Pirelli tire plant, affect me lung-nm average cost curve of a firm? Can you draw the old curve and the new one on the same axes? How might such an improvement affect other firms in the industry?arrow_forwardCompute the average total cost, average variable cost, and marginal cost of producing 50 and 72 haircuts. Draw the graph of line three curves between 60 and 72 haircuts.arrow_forward

- Return to Figure 7.7. What is the marginal gain in output from increasing the number of batters from 4 to 5 and from 5 to 6? Does it continue the pattern of diminishing marginal returns? Figure 7.7 How output Affects Total costsarrow_forwardBased on your answers to the WipeOut Ski Company in Exercise 7.3, now imagine a situation where the firm produces a quantity of 5 units that it sells for a price of 25 each. What will be the companys profits or losses? How can you tell at a glance whether the company is making or losing money at this price by looking at average cost? At the given quantity and price, is the marginal unit produced adding to profits?arrow_forwardWhat two lines on a cost curve diagram intersect at the shutdown point?arrow_forward

- Automobile manufacturing is an industry subject to significant economies of scale. Suppose there are four domestic auto manufacturers, but the demand for domestic autos is no more than 2.5 times the quantity produced at the bottom of the long-run average cost curve. What do you expect will happen to the domestic auto industry in the long run?arrow_forwardIn choosing a production technology, how will firms react if one input becomes relatively more expensive?arrow_forwardAverage cost curves (except for avenge fixed cost) tend to be U-shaped, decreasing and then increasing. Marginal cost curves have the same shape, though this may be harder to see since most of the marginal cost curve is increasing. Why do you think that average and marginal cost curves have the same general shape?arrow_forward

- What is the relationship between marginal product and marginal cost? (Hint: Look at the curves.) Why do you suppose that is? Is this relationship the same in the long run as in the short run?arrow_forwardThe WipeOut Ski Company manufactures skis for beginners. Fixed costs are 30. Fill in Table 7.16 for total cost, average variable test, average total cost, and marginal cost.arrow_forwardWhy does exit occur?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics 2e

Economics

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:OpenStax

Managerial Economics: Applications, Strategies an...

Economics

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:9781337091992

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning