MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

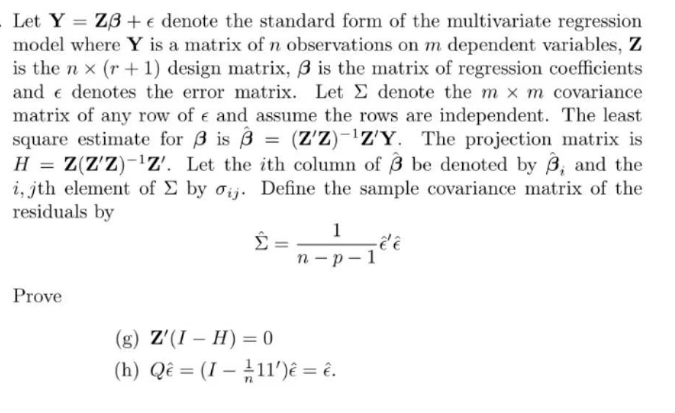

Transcribed Image Text:Let Y Z3+ e denote the standard form of the multivariate regression

model where Y is a matrix of n observations on m dependent variables, Z

is the nx (r + 1) design matrix, 3 is the matrix of regression coefficients

and denotes the error matrix. Let Σ denote the m x m covariance

matrix of any row of e and assume the rows are independent. The least

square estimate for 3 is 3 = (Z'Z)-¹Z'Y. The projection matrix is

H = Z(Z'Z)-¹Z'. Let the ith column of 3 be denoted by 3, and the

i, jth element of Σ by oij. Define the sample covariance matrix of the

residuals by

Prove

Σ

=

1

n-p-1

(g) Z'(I-H) = 0

(h) Qê= (I-11')ê = ê.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- Suppose we have a multiple regression model with 2 predictors and an intercept. (Without any interaction or higher order terms, we have only the 2 predictors in the model and the intercept.) We have only n= 6 observations (so it would be rather silly to fit this model to this data, but let's pretend it is reasonable). We find the values of the first 5 residuals are: 2.6, 2.3, 2.5, -1.5, -1.4 What is the value of MSRes for this multiple regression model?arrow_forwardfind the least squares regression line equation from the given data.arrow_forwardStudents who complete their exams early certainly can intimidate the other students, but do the early finishers perform significantly differently than the other students? A random sample of 37 students was chosen before the most recent exam in Prof. J class, and for each student, both the score on the exam and the time it took the student to complete the exam were recorded. a. Find the least-squares regression equation relating time to complete (explanatory variable, denoted by x, in minutes) and exam score (response variable, denoted by y) by considering Sx = 15, sy = 17,r = 39.706, x = 90, ỹ = 78 b. The standard error of the slope of this least-squares regression line was approximately (Sp) is 20.13. Test for a significant positive linear relationship between the two variables exam score and exam completion time for students in Prof. J's class by doing a hypothesis test regarding the population slope B1. Write the null and Alternate hypothesis and conclude the results. (Assume that…arrow_forward

- Consider the following population model for household consumption: cons = a + b1 * inc+ b2 * educ+ b3 * hhsize + u where cons is consumption, inc is income, educ is the education level of household head, hhsize is the size of a household. Suppose a researcher estimates the model and gets the predicted value, cons_hat, and then runs a regression of cons_hat on educ, inc, and hhsize. Which of the following choice is correct and please explain why. A) be certain that R^2 = 1 B) be certain that R^2 = 0 C) be certain that R^2 is less than 1 but greater than 0. D) not be certainarrow_forwardFind the least-squares regression line y^=b0+b1x through the points (−2,2),(3,6),(4,15),(8,20),(12,26) and then use it to find point estimates y^ corresponding to x=4 and x=8. For x=4, y^ = For x=8, y^ =arrow_forward)A county real estate appraiser wants to develop a statistical model to predict the appraised value of 3) houses in a section of the county called East Meadow. One of the many variables thought to be an important predictor of appraised value is the number of rooms in the house. Consequently, the appraiser decided to fit the simple linear regression model: E(u) = Bo + Bix, where y = appraised value of the house (in thousands of dollars) and x = number of rooms. Using data collected for a sample of n = 73 houses in Fast Meadow, the following results were obtained: y = 73.80 + 19.72x What are the properties of the least squares line, y = 73.80 + 19.72x? A) Average error of prediction is 0, and SSE is minimum. B) It will always be a statistically useful predictor of y. C) It is normal, mean 0, constant variance, and independent. D) All 73 of the sample y-values fall on the line.arrow_forward

- Suppose Derrick is an insect enthusiast who measured the body length and weight of three insects in his backyard. His data are shown in the table. Length (mm) Weight (mg) Variable ?x ?y Insect 1 7 28 Insect 2 21 42 Insect 3 35 70 Derrick used the data to compute the least squares regression line. ?̂ =1.5?+15.167y^=1.5x+15.167 Calculate the residual value for each of Derrick's data points and the sum of the residual values. Report your answers precise to three decimal places. Residual 1: Residual 2: Residual 3: Sum of the residuals:arrow_forwardFind the coefficients for the least-squares regression line y^=b0+b1x through the points (−2,0),(2,6),(4,14),(9,20),(9,25) b0 =. b1 =arrow_forwardA year-long fitness center study sought to determine if there is a relationship between the amount of muscle mass gained y(kilograms) and the weekly time spent working out under the guidance of a trainer x(minutes). The resulting least-squares regression line for the study is y=2.04 + 0.12x A) predictions using this equation will be fairly good since about 95% of the variation in muscle mass can be explained by the linear relationship with time spent working out. B)Predictions using this equation will be faily good since about 90.25% of the variation in muscle mass can be explained by the linear relationship with time spent working out C)Predictions using this equation will be fairly poor since only about 95% of the variation in muscle mass can be explained by the linear relationship with time spent working out D) Predictions using this equation will be fairly poor since only about 90.25% of the variation in muscle mass can be explained by the linear relationship with time spent…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman