FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

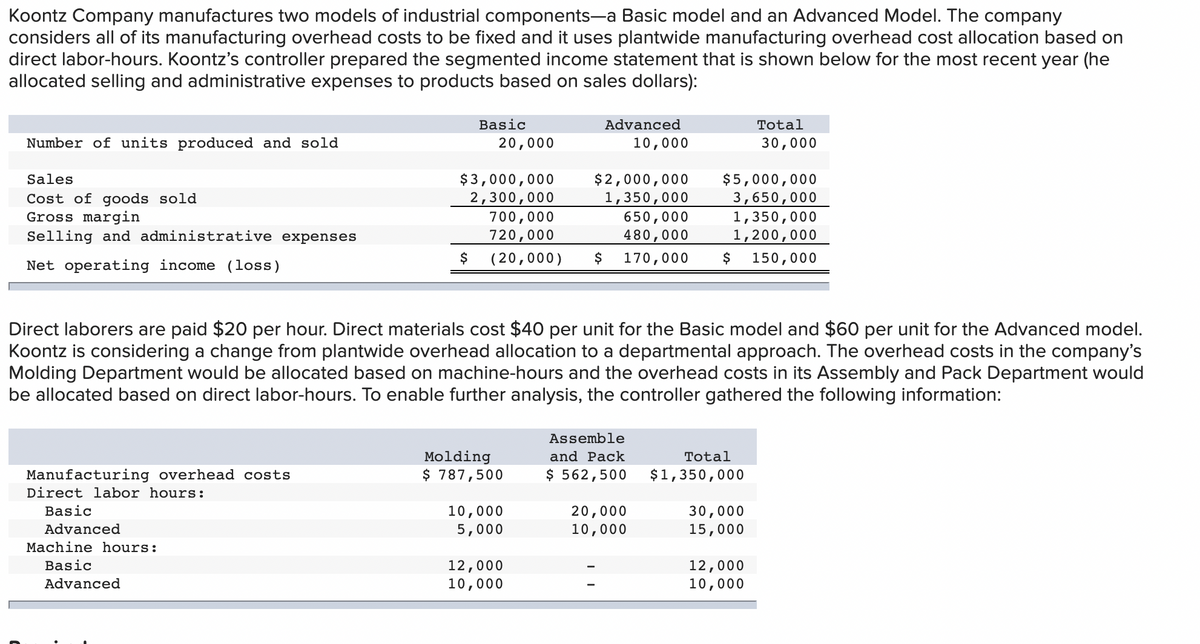

Transcribed Image Text:Koontz Company manufactures two models of industrial components-a Basic model and an Advanced Model. The company

considers all of its manufacturing overhead costs to be fixed and it uses plantwide manufacturing overhead cost allocation based on

direct labor-hours. Koontz's controller prepared the segmented income statement that is shown below for the most recent year (he

allocated selling and administrative expenses to products based on sales dollars):

Basic

Advanced

Total

Number of units produced and sold

20,000

10,000

30,000

$3,000,000

2,300,000

700,000

720,000

$2,000,000

1,350,000

650,000

480,000

$5,000,000

3,650,000

1,350,000

1,200,000

Sales

Cost of goods sold

Gross margin

Selling and administrative expenses

$

( 20,000)

$

170,000

$

150,000

Net operating income (loss)

Direct laborers are paid $20 per hour. Direct materials cost $40 per unit for the Basic model and $60 per unit for the Advanced model.

Koontz is considering a change from plantwide overhead allocation to a departmental approach. The overhead costs in the company's

Molding Department would be allocated based on machine-hours and the overhead costs in its Assembly and Pack Department would

be allocated based on direct labor-hours. To enable further analysis, the controller gathered the following information:

Assemble

Molding

$ 787,500

and Pack

Total

Manufacturing overhead costs

Direct labor hours:

$ 562,500

$1,350,000

30,000

15,000

Basic

10,000

5,000

20,000

10,000

Advanced

Machine hours:

12,000

10,000

Basic

12,000

10,000

Advanced

Transcribed Image Text:4. Using your activity-based cost assignments from requirement 3, prepare a contribution format segmented income statement that is

adapted from:Exhibit 4-8; (Hint: Organize all of the company's costs into three categories: variable expenses, traceable fixed expenses,

and common fixed expenses.)

5. Using your contribution format segmented income statement from requirement 4, calculate the break-even point in dollar sales for

the Advanced model.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Wilmington Company has two manufacturing departments--Assembly and Fabrication. It considers all of its manufacturing overhead costs to be fixed costs. The first set of data that is shown below is based on estimates from the beginning of the year. The second set of data relates to one particular job completed during the year--Job Bravo. Estimated Data Assembly Fabrication Total Manufacturing overhead costs $ 7,250,000 $ 7,830,000 $ 15,080,000 Direct labor-hours 145,000 87,000 232,000 Machine-hours 58,000 290,000 348,000 Job Bravo Assembly Fabrication Total Direct labor-hours 30 22 52 Machine-hours 22 25 47 Required: 1. If Wilmington used a plantwide predetermined overhead rate based on direct labor-hours, how much manufacturing overhead would be applied to Job Bravo? 2. If Wilmington uses departmental predetermined overhead rates with direct labor-hours as the allocation base in Assembly and machine-hours as the allocation base in…arrow_forwardKoontz Company manufactures two models of industrial components-a Basic model and an Advanced Model. The company considers all of its manufacturing overhead costs to be fixed and it uses plantwide manufacturing overhead cost allocation based on direct labor-hours. Koontz's controller prepared the segmented income statement that is shown below for the most recent year (he allocated selling and administrative expenses to products based on sales dollars): Basic Advanced Total Number of units produced and sold 20,000 10,000 30,000 $ 5,000,000 3,650,000 1,350,000 1,200,000 $3,000,000 $2,000,000 1,350,000 650,000 480,000 Sales Cost of goods sold Gross margin Selling and administrative expenses 2,300,000 700,000 720,000 (20,000) Net operating income (loss) $4 $4 170,000 150,000 Direct laborers are paid $20 per hour. Direct materials cost $40 per unit for the Basic model and $60 per unit for the Advanced model. Koontz is considering a change from plantwide overhead allocation to a departmental…arrow_forwardGodiva company has two products, A and B. The company uses activity-based costing to allocate overhead costs of $100,000. Data relating to the company's activity pools for the current year are given below: Cost Pool Total cost in Total Number of Activity Measures Used Cost Pool Product A Product B Total Activity 1 $42,000 100 200 300 Activity 2 $10,000 20 5 25 Activity 3 $48,000 3,000 3,000 6,000 Compute the activity rate (allocation rate) for Activity 2: $500 $2,000 $400 $140arrow_forward

- Klumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Supporting direct labor Machine processing Machine setups Production orders. Shipments Product sustaining Activity data have been supplied for the following two products: Total Expected Activity Activity Rates $ 7 per direct labor-hour $ 4 per machine-hour $50 per setup $ 170 per order $ 130 per shipment $ 800 per product Number of units produced per year Direct labor-hours Machine-hours Machine setups Production orders Shipments Product sustaining K425 200 1,075 2,200 11 11 22 2 M67 2,000 40 30 2 2 2 2 Required: How much total overhead cost would be assigned to K425 and M67 using the activity-based costing system?arrow_forwardHensel Manufacturing separates its manufacturing overhead costs into 2 broad categories: (1) maintenance costs and (2) utility costs. Maintenance costs average $100,000 per month, whereas utility costs average $8,000 per month. Maintenance costs are allocated to 2 activity cost pools: (1) the repair cost pool and (2) the set-up cost pool. Utility costs also are allocated to 2 activity cost pools: (1) the heating and air conditioning cost pool (HVAC) and (2) the machinery cost pool. Maintenance costs are allocated to their unique activity cost pools on the basis of the number of employees associated with each pool. Utility costs are allocated to their unique activity cost pools on the basis of kilowatt-hour (kWh) consumption. Of the company's maintenance employees, 70% engage primarily in repair activities, whereas 30% engage primarily in set-up activities. Approximately 75% of the company's kWh consumption can be traced to HVAC use, whereas 25% of its kWh consumption can be traced to…arrow_forwardLarner Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Rates $8.00 per direct labor-hour Activity Cost Pool Labor-related Machine-related Machine setups Production orders Shipments $9.00 per machine-hour $ 50.00 per setup $100.00 per order $ 180.00 per shipment General factory $9.00 per direct labor-hour Cost and activity data have been supplied for the following products: Direct materials cost per unit Direct labor cost per unit Number of units produced per year Direct labor-hours Machine-hours Machine setups Production orders Shipments Unit product cost Total Expected Activity J76 379 900 2,900 4 8 12 852 50 20 B52 4 Required: Compute the unit product cost of each product listed above. (Do not round intermediate calculations. Round your answers to 2 decimal places.) 378 $ 4.50 $ 4.75 4,000 852 $ 45.00 $10.00. 500arrow_forward

- Hansabenarrow_forwardGadubhaiarrow_forwardKlumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Supporting direct labor Machine processing Machine setups Production orders Activity Rates 2$ 6 per direct labor-hour $4 4 per machine-hour 24 50 per setup 90 per order 2$ Shipments Product sustaining 14 per shipment $ 840 per product Activity data have been supplied for the following two products: Total Expected Activity К425 М67 Number of units produced per year 200 2,000 Direct labor-hours 80 500 Machine-hours 100 1,500 Machine setups Production orders Shipments Product sustaining 1 4 1 4. 1. 10 1 1arrow_forward

- Aarrow_forwardHickory Company manufactures two products—13,000 units of Product Y and 5,000 units of Product Z. The company uses a plantwide overhead rate based on direct labor-hours. It is considering implementing an activity-based costing (ABC) system that allocates all $829,500 of its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products Y and Z: Activity Cost Pool Activity Measure Estimated Overhead Cost Expected Activity Machining Machine-hours $ 246,000 12,000 MHs Machine setups Number of setups $ 137,500 250 setups Product design Number of products $ 89,000 2 products General factory Direct labor-hours $ 357,000 14,400 DLHs Activity Measure Product Y Product Z Machine-hours 7,500 4,500 Number of setups 40 210 Number of products 1 1 Direct labor-hours 8,500 5,900 Foundational 7-12 (Algo) 12. Using the ABC system, what percentage of the Machining costs is assigned to Product…arrow_forwardQriole Inc. manufactures two products: car wheels and truck wheels. To determine the amount of overhead to assign to each product line, the controller, William Brown, has developed the following information: Estimated wheels produced Direct labour hours per wheel Car Car wheels $ Truck 45,000 11,000 4 Total estimated overhead costs for the two product lines are $1,340,000. Calculate the overhead cost assigned to the car wheels and truck wheels, assuming that direct labour hours are used to allocate overhead costs. 8 180,000arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education