FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

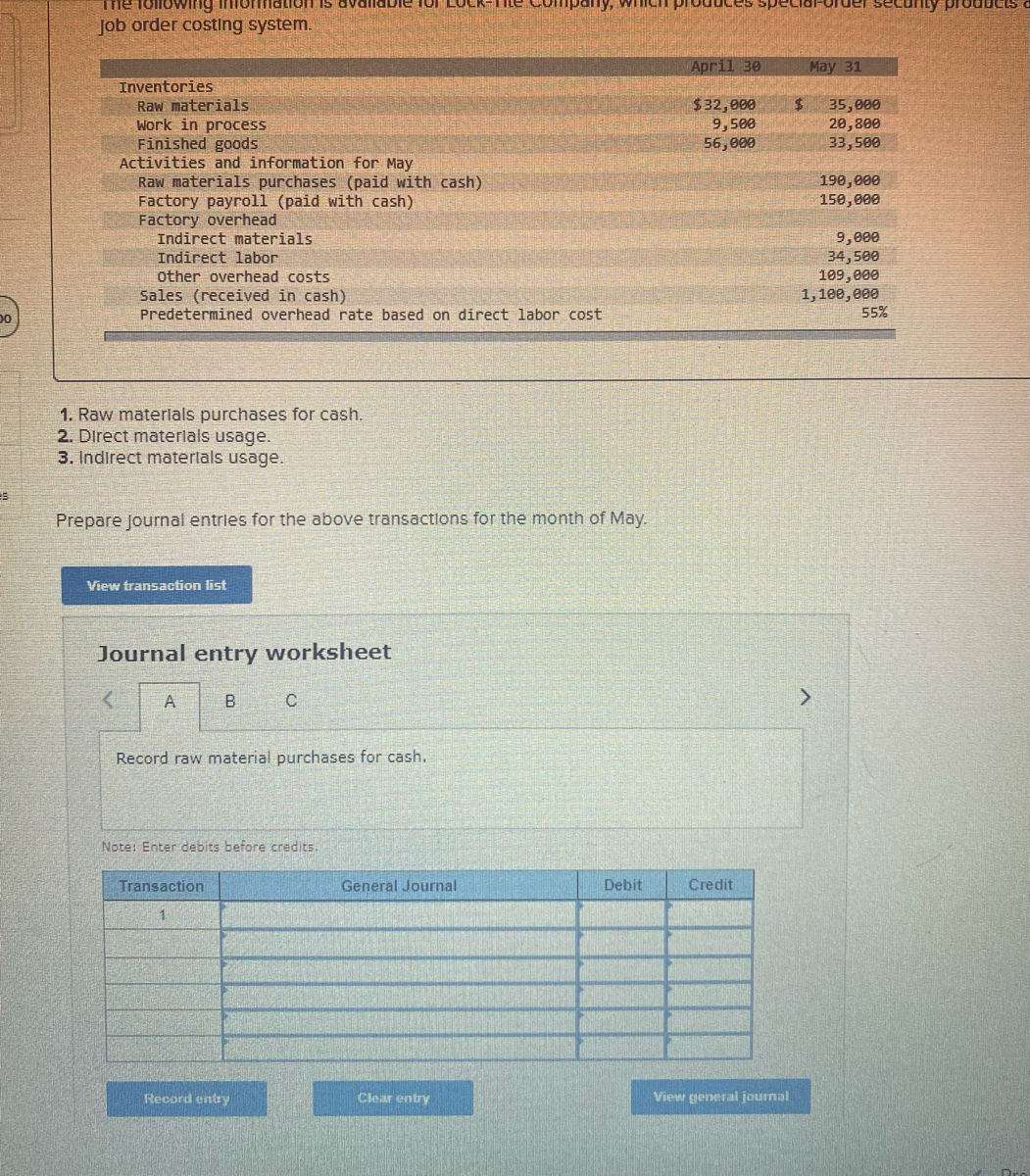

Transcribed Image Text:### Lock-It-Te Company Financial Overview

The following data pertains to Lock-It-Te Company, a producer of special-order security products utilizing a job order costing system. This overview summarizes inventory balances and activities for the month of May.

#### Inventories

- **Raw Materials**

- April 30: $32,000

- May 31: $35,000

- **Work in Process**

- April 30: $9,500

- May 31: $20,000

- **Finished Goods**

- April 30: $56,000

- May 31: $33,500

#### Activities and Information for May

- **Raw Materials Purchases**

- Paid with Cash: $190,000

- **Factory Payroll**

- Paid with Cash: $150,000

- **Factory Overhead Expenses**

- Indirect Materials: $9,000

- Indirect Labor: $34,500

- Other Overhead Costs: $109,000

- **Sales (Received in Cash)**

- $1,100,000

- **Predetermined Overhead Rate**

- Based on Direct Labor Cost: 55%

#### Instructions

To accurately prepare financial records for May, adhere to the following steps:

1. Record raw materials purchased for cash.

2. Document direct materials usage.

3. Note indirect materials usage.

Begin by preparing journal entries.

### Journal Entry Worksheet

This worksheet facilitates the recording of financial transactions related to the purchase of raw materials for cash. Ensure to enter debits before credits.

#### Transactions Table

| Transaction | General Journal | Debit | Credit |

|-------------|-----------------|-------|--------|

| 1 | | | |

*Options are available to record, clear, and view general entries.*

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Factory Overhead Rate, Entry for Applying Factory Overhead, and Factory Overhead Account Balance The cost accountant for River Rock Beverage Co. estimated that total factory overhead cost for the Blending Department for the coming fiscal year beginning February 1 would be $588,500, and total direct labor costs would be $535,000. During February, the actual direct labor cost totaled $46,000, and factory overhead cost incurred totaled $52,600. What is the predetermined factory overhead rate based on direct labor cost? Enter your answer as a whole percent not in decimals.fill in the blank% Journalize the entry to apply factory overhead to production for February. fill in the blank $fill in the blank $fill in the blank fill in the blank $fill in the blank $fill in the blank What is the February 28 balance of the account Factory Overhead—Blending Department? Amount: $fill in the blank Debit or Credit? ____________ Does the balance for Feb. 28…arrow_forwardProvide Solutionsarrow_forwardJob cost sheets show the following information: Job January February March Completed Sold AA2 $2,600 $1,400 February Not sold AA4 4,840 January February AA5 3,230 February March ААЗ 3,408 $2,321 April Not sold Total $7,440 $8,038 $2,321 What are the balances in the work in process inventory, finished goods inventory, and cost of goods sold for January, February, and March? Work in Finished Process Goods COGS January $ February $ Marcharrow_forward

- Owearrow_forwardHelparrow_forwardPredetermined Factory Overhead Rate Street Runner Engine Shop uses a job order cost system to determine the cost of performing engine repair work. Estimated costs and expenses for the coming period are as follows: Engine parts $949,400 Shop direct labor 693,000 Shop and repair equipment depreciation 59,300 Shop supervisor salaries 164,900 Shop property taxes 29,900 Shop supplies 23,100 Advertising expense 19,000 Administrative office salaries 81,600 Administrative office depreciation expense 10,400 Total costs and expenses $2,030,600 The average shop direct labor rate is $21 per hour. Determine the predetermined shop overhead rate per direct labor hour. Round the answer to nearest whole cent. per direct labor hourarrow_forward

- Ivanhoe Company begins operations on April 1. Information from job cost sheets shows the following: Manufacturing Costs Assigned Job Number April May June Month Completed 10 $6,700 $4,600 May 11 4,400 4,200 $3,200 June 12 1,400 April 13 4,900 3,500 June 14 5,600 3,600 Not complete Each job was sold for 25% above its cost in the month following completion. (a) Calculate the balance in Work in Process Inventory at the end of each month. Work in Process Inventory April 30 $enter a dollar amount May 31 $enter a dollar amount June 30 $enter a dollar amountarrow_forwardEntry for Factory Labor Costs The weekly time tickets indicate the following distribution of labor hours for three direct labor employees: Job 301 Work in Process Job 302 17 13 13 Factory Overhead Wages Payable Landon Vincent Fahad Hamad Ivory Argo The direct labor rate earned per hour by the three employees is as follows: $24 19 22 10 18 Hours 17 Job 303 7 16 Process Improvement 9 5 2 Landon Vincent Fahad Hamad Ivory Argo The process improvement category includes training, quality improvement, and other indirect tasks. 5 a. Journalize the entry to record the factory labor costs for the week. If an amount box does not require an entry, leave it blank.arrow_forwardOnline A company uses a job-order costing system with the following partially completed summary T-accounts for the just completed period: Debit Balance Direct materials Direct labor Overhead applied Balance Debits Debit Work In Process 22,000 Credits 85,000 161,000 269,000 ? Manufacturing Overhead 200,000 Credits Manufacturing overhead for the period was: Credit Credit 434,000 ?arrow_forward

- How much is total cost of goods manufactured?arrow_forwardPredetermined Factory Overhead Rate Road Runner Engine Shop uses a job order cost system to determine the cost of performing engine repair work. Estimated costs and expenses for the coming period are as follows: Engine parts Shop direct labor Shop and repair equipment depreciation Shop supervisor salaries Shop property taxes Shop supplies Advertising expense Administrative office salaries Administrative office depreciation expense Total costs and expenses The average shop direct labor rate is $22 per hour. $1,054,900 770,000 39,700 110,400 20,000 15,400 21,100 90,700 11,600 $2,133,800 Determine the predetermined shop overhead rate per direct labor hour. Round the answer to nearest whole cent. per direct labor hourarrow_forwardLouisiana Metals uses a job costing system. The company applies manufacturing overhead using a predetermined rate based on direct labor cost. The following debits (credits) appeared in the Work-in-Process Inventory for June. June 1 For the month For the month For the month For the month Balance Direct labor Direct materials Manufacturing overhead To finished goods Beginning inventory ??? $ 33,000 43, 200 19,800 (78,700) Job LM-12, the only job still in production at the end of June, has been charged $13,200 in direct materials cost and $12,400 in direct labor cost. Required: What was the beginning balance in Work-in-Process Inventory?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education