FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

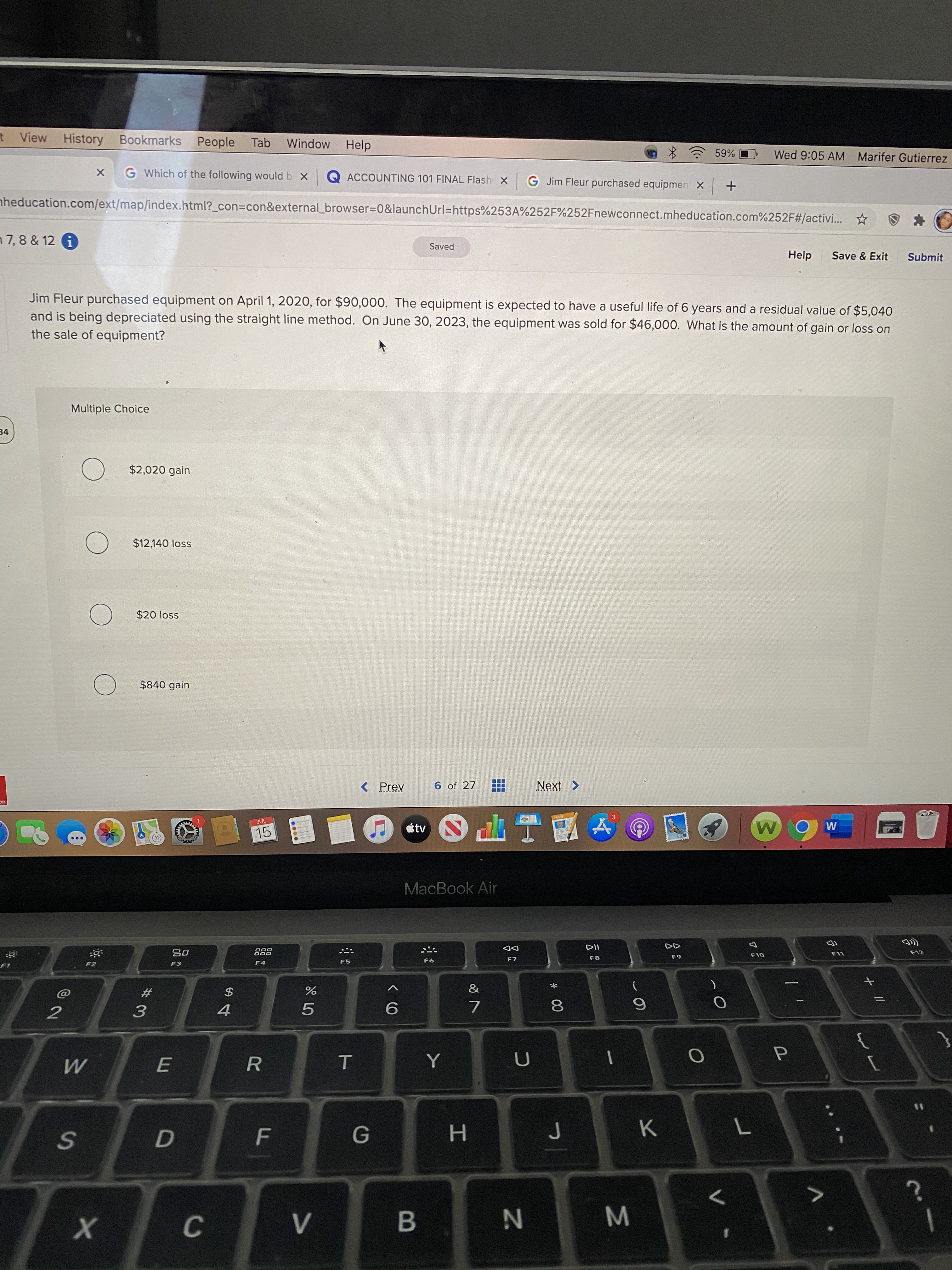

Transcribed Image Text:Jim Fleur purchased equipment on April 1, 2020, for $90,000. The equipment is expected to have a useful life of 6 years and a residual value of $5,040

and is being depreciated using the straight line method. On June 30, 2023, the equipment was sold for $46,000. What is the amount of gain or loss on

the sale of equipment?

Multiple Choice

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- On July 1, 2020, Hale Kennels sells equipment for $80,000. The equipment originally cost $300,000, had an estimated 5-year life and an expected residual value of $50,000. The accumulated depreciation account had a balance of $225,000 on January 1, 2020, using the straight-line method. The gain or loss on disposal is Select one: a. $30,000 gain. b. $45,000 gain. c. $45,000 loss. d. $30,000 loss.arrow_forwardSIMCO Company purchases a machine on 1/1/2020, at a cost of $24,000. The machine is depreciated using the straight-line method. The machine's useful life is estimated to be 5 years with a $4,000 salvage value. On 1/1/2022, management decides to change the useful life to 7 years, instead of 5 years, and keep salvage value the same.arrow_forwardSandhill Company owns equipment that cost $61,200 when purchased on January 1. 2019. It has been depreciated using the straight-line method based on estimated salvage value of $4,200 and an estimated useful life of 5 years. Prepare Sandhill Company's journal entries to record the sale of the equipment in these four independent situations. Sold for $29,200 on January 1.2022. Sold for $29,200 on May 1, 2022. Sold for $10,200 on January 1, 2022. Sold for $ 10,200 on October 1, 2022arrow_forward

- Perfect Auto Rentals sold one of its cars on January 1, 2019. Perfect had acquired the car on January 1, 2017, for $22,300. At acquisition Perfect assumed that the car would have an estimated life of 3 years and a residual value of $4,000. Assume that Perfect has recorded straight-line depreciation expense for 2017 and 2018. Required: Prepare the journal entry to record the sale of the car assuming the car sold for (a) $10,100 cash, (b) S7,700 cash, and (c) $11,200 cash. The company recorded the car as equipment.arrow_forwardOn January 1, 2014, Tanaka, Inc. purchased equipment for $27,000. Tanaka uses straight-line depreciation and estimates a 10-year useful life and a $3,000 salvage value. On December 31, 2021, Tanaka sells the equipment for $14,200. In recording this sale, Tanaka should reflect: Select one: a. A $1,400 gain b. A $1,600 gain c. A $3,000 gain d. A $6,400 gain e. None of the abovearrow_forwardWinia Corporation purchased farm equipment on January 1, 2019, for $280,000. In 2019 and 2020, Winia depreciated the asset on a straight-line basis with an estimated useful life of five years and a $90,000 residual value. In 2021, due to changes in technology, Winia revised the residual value to $30,000 but still plans to use the equipment for the full five years. What depreciation would Winia record for the year 2021 on this equipment? $8,000arrow_forward

- On August 1, 2015, Toy Inc. purchased a new piece of equipment that cost $25000. The estimated useful life is five years and the estimated residual value is $2,500. During the five years of useful life the equipment is expected to produce 10,000 units. If Toy Inc. uses the straight line method of depreciation and sells the equipment for $11,500 on August 1st, 2018. What will be the realized gain (loss)? Multiple Choice $0 $4,500 $13,500 None of the other alternatives are correct ($9,000) Xarrow_forwardOn January 1, 2018, Wheeler, Inc. purchased some equipment for $3,900. The equipment had an estimated life of five years and an expected residual value of $200. On July, 1, 2020, the equipment was sold for $1,000. Wheeler uses straight-line depreciation. Refer to Exhibit 11-03, what is the amount of depreciation expense that needs to be brought up to date prior to the sale? $370 $480 $200 $740arrow_forwardSchager Company purchased a computer system on January 1, 2019, at a cash cost of $25,000. The estimated useful life is 10 years, and the estimated residual value is $3,000. The company will use the double declining-balance depreciation method. How much is the 2020 depreciation expense? Group of answer choices A)$5,000 B)$4,120 C)$4,000 D)$3,520 E)None of the abovearrow_forward

- Cutter Enterprises purchased equipment for $66,000 on January 1, 2021. The equipment is expected to have a five-year life and a residual value of $8,100. Using the double-declining-balance method, depreciation for 2022 would be: Multiple Choice $26,400. $13,896. $15,840 None of these answer choices are correct.arrow_forwardHaystack company purchased a machine on January 1, 2015 for $48,000. The company estimates that the machine will have a $4,000 salvage value at the end of its 10 year useful life. On September 30, 2019 the machine was sold for a gain of $3,500. What must have been the selling price of the machine?arrow_forwardArchie Company purchased a framing machine for $52,000 on January 1, 2024. The machine is expected to have a four-year life, with a residual value of $7,000 the end of four years. Using the straight-line method, depreciation for 2025 and book value on December 31, 2025, would be: Multiple Choice O O $11,250 and $29,500, respectively $13,000 and $26,000, respectively $13,000 and $19,000, respectively $11,250 and $22,500, respectivelyarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education