Related questions

Investigating the principle that all

Bonds: Bonds are a debt instrument on which interest is paid. They can be issued at a discount/par or premium.

Present Value of Bonds Payable = Present Value of all interest payments + Present Value of principle returned

Present Value of Bonds Payable = PVIFA (r%, n) * Interest payment + PVIF (r%, n) * principal value

where,

PVIFA = Present Value of Annuity

r = Rate of interest (market)

n = Number of years

PVIF = Present Value

Note:

To get PVIFA (4.5%,10) we look for 4.5% and in that column, we search for 10 in the row and we take the intersection value.

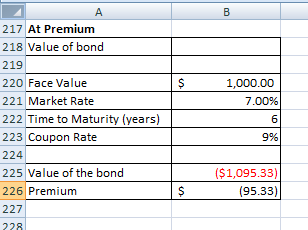

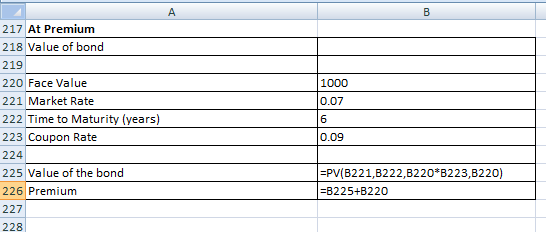

Let our bond be of par value of 1000

Coupon rate: 9% paid annually

Maturity: 6 years

Current Market Rate: 7%

Price of the bond:

Hence, Value of Bond = $1,095.33

Step by stepSolved in 3 steps with 2 images

- A bond's real rate of return is reflected by the bond's 1). YTM 2). Coupon Rate 3). Par Value 4). Selling Price 5). Redemption Valuearrow_forwardNeed help finding the current yield for both bond P and D, & the capital yield gains for both bonds P and D. Thank you in advancearrow_forwardWrite down an equation for the three main components of the nominal long term interest rate on a bond, clearly explaining what each symbol stands for.arrow_forward

- solve this practice problemarrow_forwardCheck all that are true with respect to the yield to maturity (YTM) and the expected return for a bond. Group of answer choices The expected return is based on the contractly obligated payments whereas the YTM is based on what the investors expect to receive The YTM is based on the promised payments whereas the expected return is based on the expected cash flows Higher YTMs always mean higher expected returns In the presence of non-zero default risk, the YTM will be higher than the expected return YTM is just another name for the expected returnarrow_forwardcan you may this calculations for each of my bonds?. For each of your bonds, calculate expected defavvult percent loss as = default probability* (1 - recovery rate ). You will need to use the default rates and recovery rates that match each bond's rating. 4. Calculate the overall expected loss to your portfolio as the weighted average of the expected default percent lossarrow_forward

- Calculate YTC using a financial calculator by entering the number of payment periods until call for N, the price of the bond for PV, the interest payments for PMT, and the call price for FV. Then you can solve for 1/YR YTC. Again, remember you need to make the appropriate adjustments for a semiannual bond and realize that the calculated 1/YR is on a periodic basis so you will need to multiply the rate by 2 to obtain the annual rate. In addition, you need to make sure that the signs for PMT and FV are identical and the opposite sign is used for PV; otherwise, your answer will be incorrect. A company is more likely to call its bonds if they are able to replace their current high-coupon debt with less expensive financing. A bond is more likely to be called if its price is above par-because this means that the going market interest rate is less than its coupon rate. Quantitative Problem: Ace Products has a bond issue outstanding with 15 years remaining to maturity, a coupon rate of 8.4%…arrow_forwardUse the following information to answer this question. In your answers, ignore the negative sign, if any. Yield on Bond A Yield on Bond B Yield on Bond C 5.50% 6.50% 3.50% a) What is the yield spread between bonds A and B (in basis points)? b) What is the relative yield spread between bonds B and C? Bond C is your basis. c) What is the yield ratio between A and C? Bond C is your basis.arrow_forwardPlease help with section d!!arrow_forward

- The time value of money is used in calculating bond prices because: Group of answer choices A - The company might choose to repay the bonds prior to their maturity date B - Bond investors receive future payments and purchase bonds with current dollars C - The amount to be repaid at maturity will change as market rates change D - Cash interest payments to bondholders will change as market rates changearrow_forwardGive typing answer with explanation and conclusion Question 16: Which of the following statements about convexity are true? I. Convexity accounts for the curvilinear function of bond rates II. A bond with a very low coupon and a long maturity will have low convexity III. A bond investor would seek to avoid bonds with high convexity. IV. Convexity is defined as the rate of change of the slope of the price/yield curve V. There is an inverse relationship between maturity and convexity a. I. b. II. III. IV. c. I. IV. d. II. IV. V. e. I. II. IV. V.arrow_forwardGive Correct Answer with explanation and also provide explanation of Correct and incorrect optionarrow_forward

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education