Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

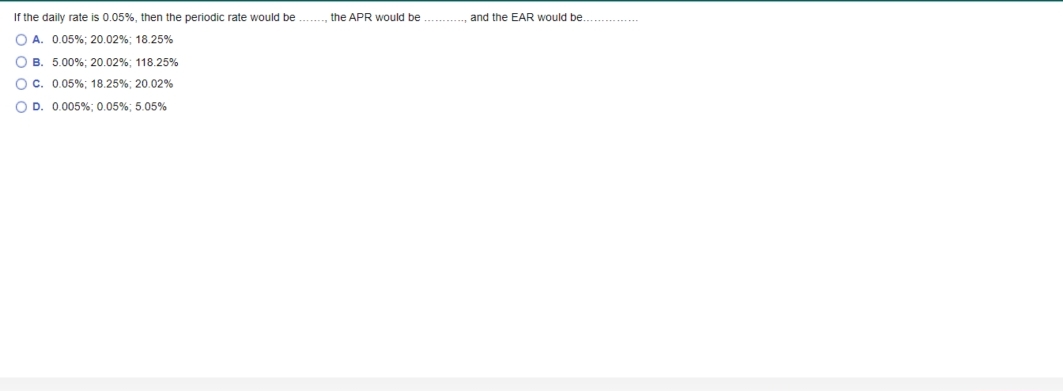

Transcribed Image Text:If the daily rate is 0.05%, then the periodic rate would be ., the APR would be ., and the EAR would be .

O A. 0.05%; 20.02%; 18.25%

O B. 5.00%; 20.02%; 118.25%

Oc. 0.05%; 18.25%; 20.02%

O D. 0.005%; 0.05%; 5.05%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Find the effective rate of interest corresponding to a nominal rate of 5.5% compounded seminannually. Answer choices: 5.645% 5.91% 5.558% 5.569%arrow_forwardSuppose that the current one-year rate (one- year spot rate) and expected one-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows: 1R1=6%, E(2r1) =7%, E(3r1) =7.5% E(4r1)=7.85% 1 Using the unbiased expectations theory, calculate the current (long-term) rates for one-, two-, three-, and four-year-maturity Treasury securities. Show your answers in percentage form to 3 decimal places.arrow_forwardAssume an initial starting Ft of 306 units, a trend (Tt) of eight units, an alpha of 0.20, and a delta of 0.40. If actual demand turned out to be 294, calculate the forecast for the next period. (Round your answer to 1 decimal place.) Forecast for the next period unitsarrow_forward

- Suppose that the current 1-year rate (1-year spot rate) and expected 1-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows:1R1 = 2.62%, E(2r1) = 3.90%, E(3r1) = 4.40%, E(4r1) = 5.90%Using the unbiased expectations theory, calculate the current (long-term) rates for one-, two-, three-, and four-year-maturity Treasury securities. (Do not round intermediate calculations. Round your answers to 2 decimal places.)arrow_forwardSuppose you work as a broker in an investment company, and there is an expectation that the market interest rate will be 0.031. based on this expectation you are required to calculate the market price for the following CD; Issue date: 1 January 2021 Maturity date:10 May 2021. The face value OMR 10000. Interest on CD: 5 percent.arrow_forwardUse the following Annuity Table for questions 1 through 6. Future Value of Ordinary Annuity of 1 Period 5% 6% 8% 10% 12% 11.000001.000001.000001.000001.00000 22.050002.060002.080002.100002.12000 33.152503.183603.246403.310003.37440 44.310134.374624.506114.641004.77933 55.525635.637095.866606.105106.35285 66.801916.975327.335927.715618.11519 78.142018.393848.922809.4871710.08901 89.549119.8974710.6366311.4358912.29969 911.0265611.4913212.4875613.5794814.77566 1012.5778913.1807914.4865615.9374317.54874 Present Value of an Ordinary Annuity of 1 Period 5% 6% 8% 10% 12% 1.95238.94340.92593.90909.89286 21.859411.833391.783261.735541.69005 32.723252.673012.577102.486852.40183 43.545953.465113.312133.169863.03735 54.329484.212363.992713.790793.60478 65.075694.917324.622884.355264.11141 75.786375.582385.206374.868424.56376 86.463216.209795.746645.334934.96764 97.107826.801696.246895.759025.32825 107.721737.360096.710086.144575.65022 Use the following…arrow_forward

- Solve for the unknown interest rate in each of the following (Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.):arrow_forwardCan you please help with the question in the picture attached? The answer should be only one and I’m quite confused. Thank you!arrow_forwardSuppose that the current 1-year rate (1-year spot rate) and expected 1-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively) are as follows:1R1 = 2.62%, E(2r1) = 3.90%, E(3r1) = 4.40%, E(4r1) = 5.90%Using the unbiased expectations theory, calculate the current (long-term) rates for one-, two-, three-, and four-year-maturity Treasury securities. (Do not round intermediate calculations. Round your answers to 2 decimal places.)arrow_forward

- Find the discount rate equivalent to the following: r= 11 5/8% t= 145 days t= 1 year and 7 monthsarrow_forwardApproximately, what is the value of (F) if P-15300, n=7 years, and i= 6% per year? Select one: O a. 23006 O b. 30829 O c. 27608 O d. 19095arrow_forwardSuppose that the current 1-year rate (1-year spot rate) and expected 1-year T-bill rates over the following three years (I.e., years 2, 3, and 4, respectively) are as follows: 1R1 = 1%, E(211) = 4.30%, E(31) = 4.80%, E471) = 6.30% Using the unblased expectations theory, calculate the current (longterm) rates for 1-, 2-, 3-, and 4-year-maturity Treasury securities. Plot the resulting yield curve. (Do not round Intermediate calculations. Round your answers to 2 decimal places.) Year 1234 Current (Long-term) Rates %arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education