ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

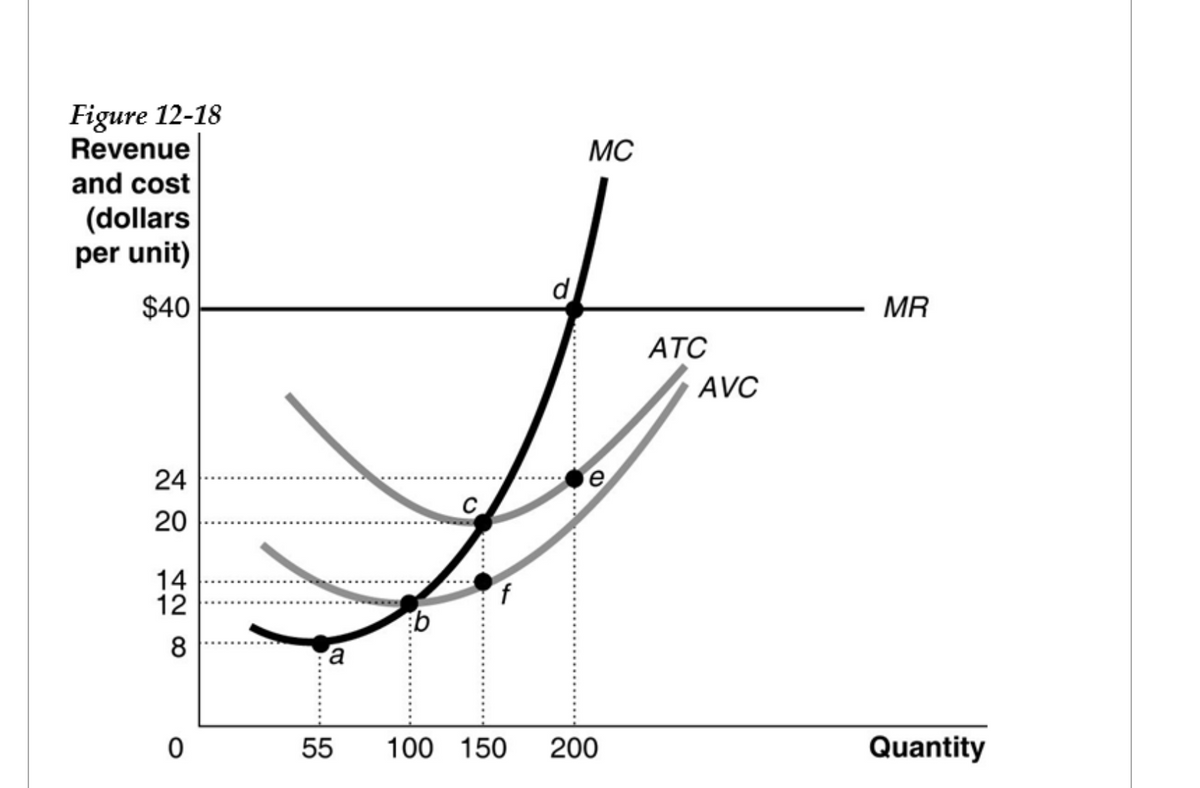

10 If it is not in long-run equilibrium, what will happen in this industry to restore long-run equilibrium?

11 In long-run equilibrium, what is the firm's profit-maximizing quantity?

Transcribed Image Text:Figure 12-18

Revenue

MC

and cost

(dollars

per unit)

d

$40

MR

ATC

AVC

24

C

20

14

12

8

a

55

100 150

200

Quantity

.......

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 11. Consider a competitive market where firms have U-shaped cost curves. Which of the following is true? a. The long run market supply curve for a constant cost industry is upward sloping, and, the short run supply curve of each firm is upward sloping. b. The long run market supply curve for an increasing cost industry is upward sloping, and, the short run supply curve of each firm is upward sloping. c. The long run market supply curve for a decreasing cost industry is upward sloping, and, the short run supply curve of each firm is upward sloping. d. The long run market supply curve for an increasing cost industry is downward sloping, and, the short run supply curve of each firm is horizontal. e. None of the above.arrow_forward4. The demand for an individual firm's output depends on the demand for the industry's output, the number of firms in the industry, and the structure of the industry. O a. True Ob. Falsearrow_forward3. Suppose a perfectly competitive firm is operating at a level of output such that P> MC. Would you advise this firm to keep producing at this level or should it increase or decrease its output? Why? (Hint: it will help you to draw a graph for a perfectly competitive firm in short run equilibrium. The level of profit in equilibrium does not matter).arrow_forward

- 11. The graph below shows the marginal revenue, marginal cost, and average total cost at different quantities for a firm in a perfectly competitive market. If this firm chooses to produce no output in the short run, what must the market price be? A-Below $20 $21-$30 $31-$40 $41-$50 Above $50 7. firm's implicit costs are $10,000, explicit costs are $5,000, and its total revenue is $10,000. This firm is earning A-normal accounting profit B-positive accounting profit of $5,000 C-positive economic profit of $5,000 D-normal economic profit E-negative accounting profit of $5,000arrow_forwardLooking to see how to resolvearrow_forward7 A local tavern in a perfectly competitive market was in a long-run equilibrium. Then, a scientific breakthrough determines that beer prevents heart attacks, resulting in an increase in demand for beer. Describe the market processes that affect the tavern in both the short run and the new long-run equilibrium.arrow_forward

- 7. Short-run supply and long-run equilibrium Consider the competitive market for ruthenium. Assume that no matter how many firms operate in the industry, every firm is identical and faces the same marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves plotted in the following graph. COSTS (Dollars per pound) 100 90 80 70 40 30 20 10 0 0 MC D 5 10 ATC 15, 15 AVC ☐ 15 20 25 30 35 QUANTITY (Thousands of pounds) 40 + 45 50 The following graph plots the market demand curve for ruthenium. (?)arrow_forward22. Which of these is a valid difference between firms in competitive price-searcher and price-taker markets? Price-taker firms advertise their products, while price-searcher firms do not. Price-searcher firms advertise their products, while price-taker firms do not. Price takers earn economic profit in the short run, while price searchers do not. Price searchers earn economic profit in the long run, while price takers do not.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education