FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

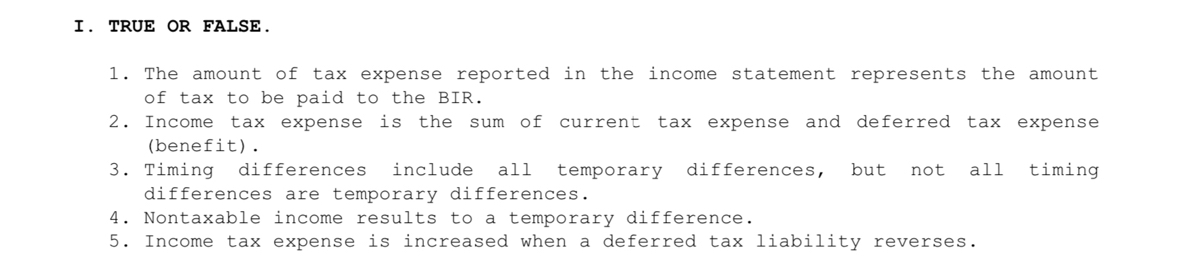

Transcribed Image Text:I. TRUE OR FALSE.

1. The amount of tax expense reported in the income statement represents the amount

of tax to be paid to the BIR.

2. Income tax expense is the sum of

current

tax expense and deferred tax expense

(benefit).

3. Timing

differences

include

all

temporary

differences,

but

all

timing

not

differences are temporary differences.

4. Nontaxable income results to a temporary difference.

5. Income tax expense is increased when a deferred tax liability reverses.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 1continue.. Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.For each item below, indicate whether it involves: 1. A temporary difference that will result in future deductible amounts and, therefore, will usually give rise to a deferred income tax asset. 2. A temporary difference that will result in future taxable amounts and, therefore, will usually give rise to a deferred income tax liability. 3. A permanent difference. (e) Installment sales of investments are accounted for by the accrual method for financial reporting purposes and the installment method for tax purposes. (f) For some assets, straight-line depreciation is used for both financial reporting purposes and tax purposes, but the assets’ lives are shorter for tax purposes. (g)…arrow_forwardTax rates other than the current tax rate may be used to calculate the deferred income tax amount for financial statement reporting if O it is probable that a future tax rate change will occur. O it appears likely that a future tax rate will be greater than the current tax rate. O it appears likely that a future tax rate will be less than the current tax rate. O the enacted tax rate is expected to apply in future years.arrow_forwardA deferred tax account is classified on the balance sheet as: A net noncurrent amount A net current amount It should never appear on the balance sheet Either a current or a noncurrent liabilityarrow_forward

- If the valuation allowance for a deferred tax asset is decreased, there is a(n) ________ to income tax expense, which is a(n) ________ to income tax benefit. Group of answer choices increase; decrease increase; increase decrease; decrease decrease; increasearrow_forwardOf the following temporary differences, which one ordinarily creates a deferred tax asset? O Installment sales for tax reporting. O Fines paid for violation of law. O Prepaid expenses. O Estimated warranty expense.arrow_forwardA temporary difference which would result in a deferred tax liability is a) installment sale included in accounting income at the time of sale but not in tax incomeb) subscription received in advancec) research cost is recognized as expense in accounting income but not in tax incomed) Dividend revenue on equity investmentarrow_forward

- 2arrow_forwardExpenditures currently deducted in the tax return but not included with expenses in the income statement until subsequent years create deferred tax liabilities. O True O Falsearrow_forwardAn unused tax loss will arise when: a. Expenses deductible for tax purposes are less than the taxable income b. Expenses deductible for tax purposes exceeds the taxable income. c. Expenses deductible for tax purposes are equal to the taxable income d. Expenses deductible for tax purposes do not exist.arrow_forward

- 1 contiune Listed below are items that are commonly accounted for differently for financial reporting purposes than they are for tax purposes.For each item below, indicate whether it involves: 1. A temporary difference that will result in future deductible amounts and, therefore, will usually give rise to a deferred income tax asset. 2. A temporary difference that will result in future taxable amounts and, therefore, will usually give rise to a deferred income tax liability. 3. A permanent difference. (e) Installment sales of investments are accounted for by the accrual method for financial reporting purposes and the installment method for tax purposes.(f) For some assets, straight-line depreciation is used for both financial reporting purposes and tax purposes, but the assets’ lives are shorter for tax purposes.(g)…arrow_forwardSome items are treated as a deduction for tax purposes when they are paid but are recognised as expenses when they are accrued for accounting purposes. Which of the following items are of that type? a. Warranty costs b. Goodwill impairment c. Fines d. Entertainment expenses e. Prepaid insurancearrow_forwardValuation allowances reduce deferred tax liabilities to the amount that is more likely than not to be payable in the future. O True Falsearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education