Related questions

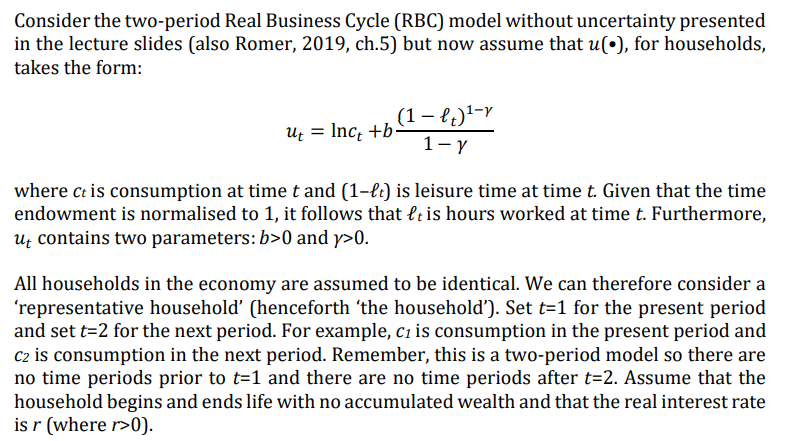

a) Present the Lagrangian (constrained maximisation) problem for the household under this modified specification and derive the first order conditions in this case. Hint: the household chooses c1, c2, ℓ1 and ℓ2.

b) Use the first order conditions for ℓ1 and ℓ2 to derive an expression for the relative amount of leisure time chosen by the household over the two periods, i.e. derive an expression for (1–ℓ1)/(1–ℓ2). Explain how an increase in the relative wage (w2/w1) affects the household’s decision about how much leisure to enjoy in each period.

c) Calculate the intertemporal elasticity of substitution between period 1 and period 2 leisure time in this case. Explain how the magnitude of this elasticity influences the household’s decision-making in the model.

d) Use the first order conditions for c1 and c2 to derive an expression for the relative amount of consumption chosen by the household over the two time periods, i.e. derive an expression for c2/c1. Provide an economic interpretation to accompany your answer.

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 14 images

Hi, is there an answer for part D at all

Hi, is there an answer for part D at all

Hi, is there an answer for part D at all

Hi, is there an answer for part D at all

Hi, is there an answer for part D at all

Hi, is there an answer for part D at all

- Question 5 Solving Consumer's Choice Problem under CES Utility, Numerical (sympy solution not required) The consumer with income Y has a preference represented by CES utility function U(91,92) = (90.4 + 92.4) 04. Given prices for the two goods, denoted by P₁, P2, solve the consumer's optimal choice problem following the steps below. (a) Write down the consumer's maximization problem, i.e be clear about (1) the choice variables, (2) the objective function and (3) the constraint. (b) Write down the Lagrangian for this optimization problem. (c) Derive the three first-order conditions. (d) Solve for the optimal consumption bundles q₁,92 . (e) Now we analyze the properties of demand. How does q respond to changes in P₁, P2 and Y? Specifically, does q increase or decrease if 1. p₁ increases? 2. P2 increases? 3. Y increases? For simplicity, we only analyze q, results for q are similar. (Hint: comparative statics, calculate, etc.)arrow_forwardA consum sumer of two goods has indirect utility v(p, w) = √w -1/2 P₁ + P₂ (a) Find the indirect money-metric utility e(p, v(p, w)). (b) Calculate the compensating variation associated with the change from (p, w) = ((4,4), 2) to (p', w')= ((1,9), 5). can you explain the notation please break it down each part of it, please teach How do you know where to place the values? The indirect money-metric utility e(p, v(p, w)) can be calculated as follows: e(p, v(p, w)) = v(p, w) - ((p1* w1) + (p2 * w2)) plugging in the values from the problem, we get: e(p, v(p, w)) = (sqrt(w))/p1^-0.5+p2^-0.5- ((44) + (9 * 5)) e(p, v(p, w)) = 2 - 41 CV = 2 e(p, v(p, w)) = -39 The compensating variation associated with the change from (p, w) = ((4,4), 2) to (p', w')= ((1,9), 5) can be calculated as follows: CV = e(p', w')- e(p, w) plugging in the values from the problem, we get: CV-39 (-41) This means that the consu would be willing to pay up to $2 in order to maintain their original level of utility.arrow_forwardAssume a consumer has current-period income y = 200, future-period income y′ = 150, current and future taxes t = 40 and t′ = 50, respectively, and faces a market real interest rate of r = 0.05, or 5% per period. The consumer would like to consume according to the following utility function: U (c, c′ ) = ln(c) + ln(c′ ). Show mathematically the lifetime budget constraint for this consumer. Find the optimal consumption in the current and future periods and optimal saving. Suppose that instead of r = 0.05 the interest rate is r = 0.1. Repeat parts (a) and (b). Does the substitution effect or the income effect dominate?arrow_forward

- Using a diagram, draw the outcome of optimal choice using an indi↵erence curve and the individual’s lifetime budget constraint.arrow_forwardQ2: Let a consumer’s daily hours of work is denoted by H, and hours of leisure by L. Consumer has no other source of income except wages for hours worked. She consumes what she earns each day. Her utility function is U(C, N) = ln(C) + 3 ln(N) Where C stands for the dollar amount of her consumption. Now answer following questions (a) Suppose the wage rate is 50Rs. per hour. Write down the consumer’s utility function and budget constraint with C and H as the choice variables. (b) How many hours will she choose to work, and what will be the resulting utility?arrow_forwardLet u(x) be a utility function that represents % and let f(.) be a continuousmonotonic function. f(x) is monotonic when x > y ⇐⇒ f(x) > f(y) a) Show that any monotonic transformation of the utility function (f ◦u) can also represent the same preferences.arrow_forward

- 4. Steve's utility funetion over leisure and consumption is given by u(L,Y) = min (3L, Y). Wage rate is w and the price of the composite consumption good is p = 1. (a) Suppose w = 5. Find the optimal leisure - consumption combination. What is the amount of hours worked? (b) Suppose the overtime law is passed so that every worker needs to be paid 1.5 times their current wage for hours worked beyond the first 8 hours. Will this law induce Steve to work more hours? If so, how many? If not, explain.arrow_forwardEmma has a utility functionU(x1, x2, x3) = logx1+ 0.8 logx2+ 0.72 logx3over her incomes x1, x2, x3 in the next three years. This is an example of(A) expected value;(B) quasi-hyperbolic utility function;(C) standard discounted utility;(D) none of the above. Emma’s preferences can exhibit which of the following behavioral patterns?(A) preference for flexibility;(B) context effects;(C) time inconsistency;(D) intransitivity.arrow_forwardConsider a consumer who can borrow or lend freely at an interest rate of 100% per period of time (think of the period as being, say, 30 years, a bit like with a mortgage). So r = 1.0, or 100%. The consumer's two-period utility function is: U = In(ct) + (1/2)In(Ct+1) The consumer earn Y=100 each period, so Y₁=100 and Yt+1 also equals 100. If this consumer is behaving optimally, trying to maximize her lifetime utility subject to the IBC, what's her consumption in period t?arrow_forward

- Suppose you have the following indirect utility function: V(Pa, Py, I) = In PxPy What are marshallian demands for x and y? I (a) (9x9y) = (22) (b) (9,9y) = (In, In 2) (c) (9, 9y) = (exp(2p/py), exp(2ppy)) I (d) (9x, gy) = (2pr+py' px+2py) What is the expenditure function for the associated expenditure minimization problem? (a) E(pa, Py, U) = (P + Py) ln(U) (b) E(pa, Py, U) = √exp(U)Papy (c) E(pa, Py, U)= (p²+p²) In(U) (d) E(pa, Py, U) = exp(U)²papy What are the individual's Hicksian demands for goods x and y? (a) (h₂, hy) = ((BU)¹/², (PU) ¹/²) (b) (ha, hy) = (RU, DU) (c) (ha, hy) = ((2 exp(U))¹/², (exp(U))¹/²) -1/2 (d) (hx, hy) = ((P₂PzU)−¹/², (P₂PzU)-¹/2) Are x and y complements or substitutes?arrow_forwardQ7: An individual lives for only two periods and has preferences given by the follow- ing intertemporal utility function: U = lng + aln(1-h₁) + B[lno₂+ a ln(1 — h₂)] (1) where, c₁, c₂ denotes consumption in period 1 and period 2 respectively h₁, h₂ denote the labour supply in period 1 and 2 respectively. Therefore 1-h is the amount of leisure time in period 1. The term 3 is the discount factor. The problem of the individual at period 1 is to choose consumption in both periods and labour supply in both periods subject to the following budget constraints: +8= why and 0₂= w₂h₂ + (1+r)s where s denote the saving, w denotes the wates and r denotes the real interest rate. (a) Provide an economic interpretation of the two budget constraints written above. (b) Combine the two budget constraints written above and prove the economic interpretation of of life time budget constraint. (c) Set the Lagrangean function and find the first order conditions with respect to C₁ C₂, hi and h₂. (d) Find the…arrow_forward6. If intertemporal preferences are consistent and the lifetime utility function is additive, then the discount function 8(t) must be (a) bounded (b) exponential (c) hyperbolic (d) linear (e) logarithmicarrow_forward

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education