FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

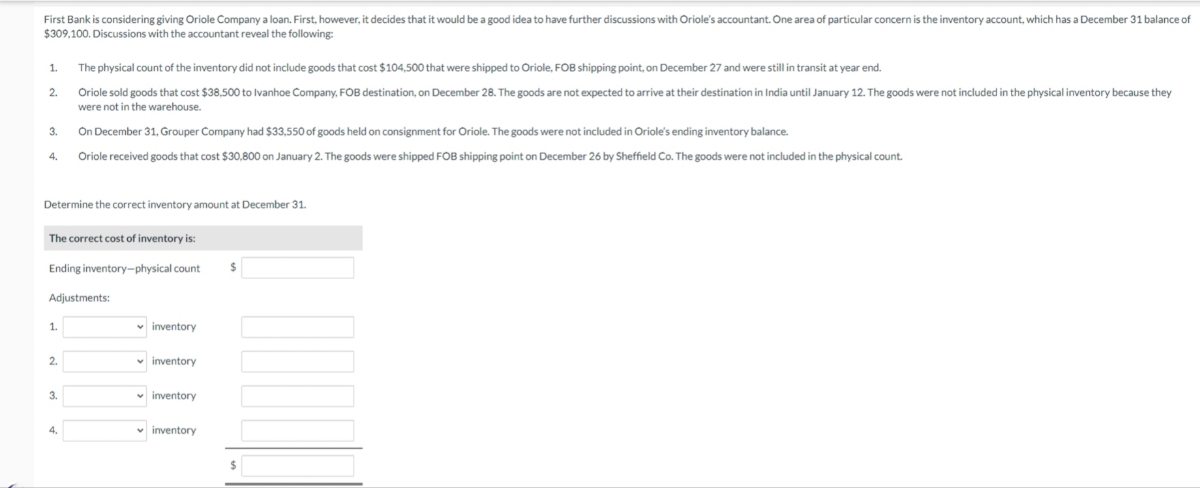

Transcribed Image Text:First Bank is considering giving Oriole Company a loan. First, however, it decides that it would be a good idea to have further discussions with Oriole's accountant. One area of particular concern is the inventory account, which has a December 31 balance of

$309,100. Discussions with the accountant reveal the following:

1.

The physical count of the inventory did not include goods that cost $104,500 that were shipped to Oriole, FOB shipping point, on December 27 and were still in transit at year end.

2.

Oriole sold goods that cost $38,500 to Ivanhoe Company, FOB destination, on December 28. The goods are not expected to arrive at their destination in India until January 12. The goods were not included in the physical inventory because they

were not in the warehouse.

3.

On December 31, Grouper Company had $33,550 of goods held on consignment for Oriole. The goods were not included in Oriole's ending inventory balance.

4.

Oriole received goods that cost $30,800 on January 2. The goods were shipped FOB shipping point on December 26 by Sheffield Co. The goods were not included in the physical count.

Determine the correct inventory amount at December 31.

The correct cost of inventory is:

Ending inventory-physical count

Adjustments:

1.

inventory

2.

inventory

3.

inventory

inventory

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Similar questions

- Bramble Company just took its physical inventory. The count of inventory items on hand at the company's business locations resulted in a total inventory cost of $350,000. In reviewing the details of the count and related inventory transactions, you have discovered the following items had not been considered. 1. Bramble has sent inventory costing $21,000 on consignment to Alissa Company. All of this inventory was at Alissa's showrooms on December 31. 2. The company did not include in the count inventory (cost, $20,000) that was sold on December 28, terms FOB shipping point. The goods were in transit on December 31. 3. The company did not include in the count inventory (cost, $14,000) that was purchased with terms of FOB shipping point. The goods were in transit on December 31. Compute the correct December 31 inventory. Correct December 31 inventory $arrow_forwardFonda Motorcycle Shop sells motorcycles, ATVs, and other related supplies and accessories. During the taking of its physical inventory on December 31, 20Y8, Fonda Motorcycle Shop incorrectly counted its inventory as $337,500 instead of the correct amount of $328,850.a. State the effect of the error on the December 31, 20Y8, balance sheet of Fonda Motorcycle Shop.b. State the effect of the error on the income statement of Fonda Motorcycle Shop for the year ended December 31, 20Y8.c. If uncorrected, what would be the effect of the error on the 20Y9 income statement?d. If uncorrected, what would be the effect of the error on the December 31, 20Y9, balance sheet?arrow_forwardHenderson Company uses the gross profit method to estimate ending inventory and cost of goods sold when preparing monthly financial statements required by its bank. Inventory on hand at the end of July was $124,000. The following information for the month of August was available from company records: Purchases Freight-in Sales. Sales returns Purchases returns $ 222,000 5,500 353,000 9,300 4,600 In addition, the controller is aware of $10,000 of inventory that was stolen during August from one of the company's warehouses. Required: 1. Calculate the estimated inventory at the end of August, assuming a gross profit ratio of 30%. 2. Calculate the estimated inventory at the end of August, assuming a markup on cost of 25%. 1. Estimated ending inventory 2. Estimated ending inventoryarrow_forward

- You own a retailer of boats, motors, and marine accessories. The store manager has just informed you that the amount of the physical inventory was incorrectly reported as $630,000 instead of the correct amount of $360,000. Unfortunately, yesterday you sent the quarterly financial statements to the stockholders. Now you must send revised statements and a letter of explanation. (a) What effect did the error have on the items of the balance sheet for the retailer? Express your answer as overstatedor understated for the items affected by the error. Merchandise inventory was by $ . Therefore, Current assets, Total assets, and Total stockholders' equity were by $ . (b) What effect will the error have on the items of the income statement for the retailer? The cost of goods sold was by $ . Therefore, gross profit and net income were by $ . (c) Did this error make the retailer's quarterly results look better or worse than they actually were? The inventory error made…arrow_forwardYou are called by Tim Duncan of Shamrock Co. on July 16 and asked to prepare a claim for insurance as a result of a theft that took place the night before. You suggest that an inventory be taken immediately. The following data are available. Inventory, July 1 Purchases-goods placed in stock July 1-15 Sales revenue-goods delivered to customers (gross) Sales returns-goods returned to stock $36,600 81,300 119,400 Your client reports that the goods on hand on July 16 cost $31,300, but you determine that this figure includes goods of $6,300 received on a consignment basis. Your past records show that sales are made at approximately 60% over cost. Duncan's insurance covers only goods owned. Claim against the insurance company $ 3,600 Compute the claim against the insurance company. (Round ratios for computational purposes to 3 decimal places, e.g. 78.736% and final answer to O decimal places, e.g. 28,987.) LA 26700arrow_forwardZaheer Abbas, an auditor with Saeed CPAs, is performing a review of K Company’s inventory account. K Company did not have a good year and top management is under pressure to boost reported income. According to its records, the inventory balance at year-end was $37,000. However, the following information was not considered when determining that amount.1. Included in the company’s count were goods with a cost of $125,000 that the company is holding on consignment. The goods belong to S Corporation. 2. The physical count did not include goods purchased by K Company with a cost of $20,000 that were shipped FOB destination on December 28 and did not arrive at K Company’s warehouse until January 3. 3. Included in the inventory account was $8,500 of office supplies that were stored in the warehouse and were to be used by the company’s supervisors and managers during the coming year. 4. The company received an order on December 29 that was boxed and was sitting on the loading dock awaiting…arrow_forward

- Concord Inc. is a retailer using a perpetual inventory system. All sales returns from customers result in the goods being returned to inventory. (Assume that the inventory is not damaged.) Assume that there are no credit transactions; all amounts are settled in cash. You are provided with the following information for Concord Inc. for the month of January. Date Description Quantity Unit Cost orSelling Price Dec. 31 Beginning inventory 160 $21 Jan. 2 Purchase 100 22 Jan. 6 Sale 180 40 Jan. 9 Sale return 10 40 Jan. 9 Purchase 75 24 Jan. 10 Purchase return 15 24 Jan. 10 Sale 50 45 Jan. 23 Purchase 100 26 Jan. 30 Sale 120 51arrow_forwardCastillo Styling is a wholesaler of hair supplies. Castillo Styling uses a perpetual inventory system. The following transactions (summarized) have been selected for analysis: a. Sold merchandise for cash (cost of merchandise $32, 757). b. Received merchandise returned by customers as unsatisfactory (but in perfect condition). for cash refund (original cost of merchandise $330). c. Sold merchandise (costing $7,885) to a customer on account with terms n/60.. d. Collected half of the balance owed by the customer in (c). e. Granted a partial allowance relating to credit sales the customer in (c) had not yet paid. f. Anticipate further returns of merchandise (costing $250) after year-end from sales made during the year. A6-3 (Algo) Part 2 Compute the gross profit percentage. (Round your answer to 1 decimal place.) $ 58,240 360 16, 600 8,300 182 370arrow_forwardDuring the taking of its physical inventory on December 31, 20Y4, Barry's Bike Shop incorrectly counted its inventory as $225,870 instead of the correct amount of $179,251. The effect on the balance sheet and income statement would be a. assets overstated by $46,619; retained earnings understated by $46,619; and net income statement understated by $46,619 b. assets overstated by $46,619; retained earnings understated by $46,619; and no effect on the income statement c. assets, retained earnings, and net income all overstated by $46,619 d. assets and retained earnings overstated by $46,619; and net income understated by $46,619arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education