ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Figure:

Note:-

Do not provide handwritten solution. Maintain accuracy and quality in your answer.

Take care of plagiarism.

Answer completely.

You will get up vote for sure.

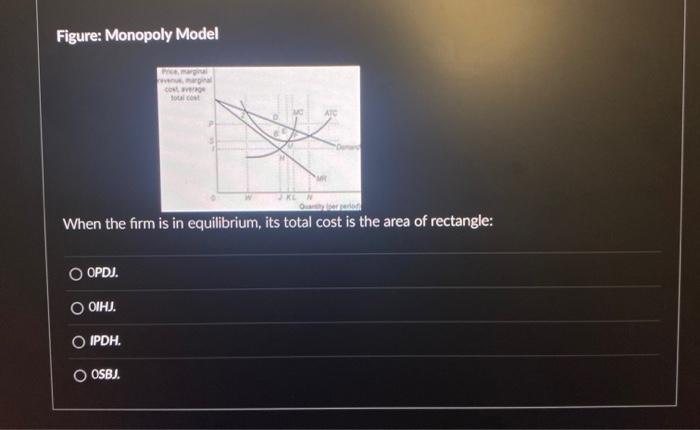

Transcribed Image Text:Figure: Monopoly Model

Price

cost average

total cost

O OPDJ.

O OIHJ.

O IPDH.

O OSBJ.

ATC

When the firm is in equilibrium, its total cost is the area of rectangle:

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- please help with Carrow_forwardDon't answer by pen paper and don't use chatgpt otherwise we will give dounvotearrow_forwardWhat will a long-run equilibrium for a monopoly most likely result in? . a economic losses or profits and production either more or less than the amount at which costs are a minimum. b either zero or positive economic profits and production less than the amount at which costs are a minimum. c zero economic profits and production less than the amount at which costs are a minimum d economic profits and production less than the amount at which costs are a minimum.arrow_forward

- For a monopoly, at the level of output where marginal revenue equals zero, then the Select one: a. firm has maximized total revenue. b. firm is a price taker. c. price elasticity of demand at this amount of output is zero. d. firm earns no revenue.arrow_forward1. For a price searching firm it's marginal revenue curve (a). Is below it's marginal cost curve (b). Must be vertical (c). Must be horizontal (d). Is below it's a demand curve 2. The most common source of illegal Monopoly today is (a). Predatory pricing (b). Intellectual property rights (c). Royal edict (d). Natural monopoly 3. The market demand is given by p= 420-0.05Q, vrp is the price of the good and Q is the quantity demanded at that price. The monopolist marginal revenue function in this market is (a). MR= 210-0.05Q (b). MR= 420-0.05Q (c). MR= 420- 0.025Q (d). MR= 420-0.1Q 4. In the monopolized ( profit maximizing) market equilibrium p> MC( the price exceeds the marginal cost) this implies that (a). The consumer surplus is equal to the producer surplus (b). The total value of the good is maximized (c). The equilibrium is Marshall inefficient (d). The market price is equal to the market quantity 5. The market demand is given Q= 440-40P, where P is the price of the good…arrow_forward1. How much total revenue does the monopoly firmmake? 2. How much total cost does the monopoly firm incur? 3. How much total profit does the firm make?arrow_forward

- What is true about the monopoly's marginal revenue? Assume no price discrimination please (just one price can be used ) a.Marginal revenue is lower than the price (except for the first unit), because selling more requires the monopoly to discount the former units as well b. Marginal revenue is equal to price c.Marginal revenue is higher than price d.None of the other answers is correct Which one?arrow_forwardI need answer typing clear no chatgpt i will give 5 upvotesarrow_forwardDue to , a natural monopoly's average cost is as its output rises. a Economies of scale; increasing b Economies of scale; decreasing c Diseconomies of scale; increasing d Diseconomies of scale; decreasingarrow_forward

- Compared to a competitive firm, a monopoly will ... (select all correct answers) A. produce an output where marginal revenue is lower than marginal cost B. charge a higher price □ C. produce greater quantities OD. be less efficientarrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardhelp please answer in text form with proper workings and explanation for each and every part and steps with concept and introduction no AI no copy paste remember answer must be in proper format with all workingarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education