ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

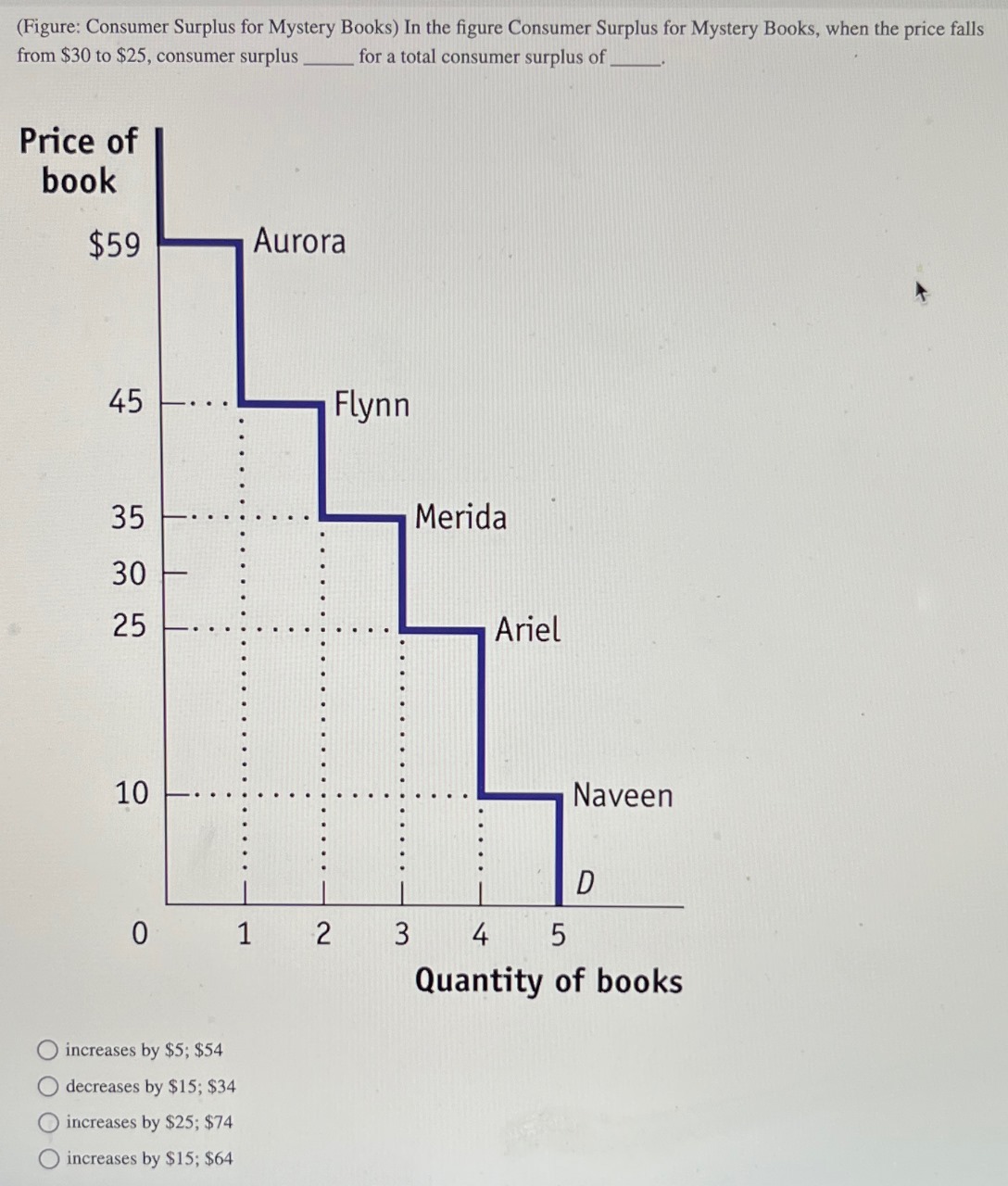

Transcribed Image Text:(Figure: Consumer Surplus for Mystery Books) In the figure Consumer Surplus for Mystery Books, when the price falls

from $30 to $25, consumer surplus

for a total consumer surplus of

Price of

book

$59

45

35

30

25

10

Aurora

0 1

increases by $5; $54

decreases by $15; $34

increases by $25; $74

increases by $15; $64

2

Flynn

3

Merida

Ariel

Naveen

D

4 5

Quantity of books

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 10 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Explain differences between a “change in demand” and a “change in quantity demanded.” (2)Find an example where there has been a change in demand of a good/service andexplain using a graph.arrow_forward7. Shifts in supply or demand II The following graph plots the market for scones in Denver, where you can assume there are always over 1,000 bakeries. Suppose scone sellers expect that tomorrow the price of scone will be significantly higher than today's price. Show the effect of this change on the market for scones by shifting one or both of the curves on the following graph, holding all else constant. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. PRICE (Dollars per scone) QUANTITY (Scones) Supply Demand Demand 1 Supply ?arrow_forwardQuestion 4 (Figure: Demand for Tuna Sandwiches) The graph shows Beatriz's weekly demand for tuna sandwiches. Tuna Sandwiches Price per sandwich $165 $12 $8 $4 0 Beatriz's individual demand curve Quantity of sandwiches (per week) If she orders three tuna sandwiches per week, what can we infer? The price of a tuna sandwich is no higher than $4. Beatriz's demand for tuna has shifted. O For Beatriz, tuna sandwiches are a normal good. O For Beatriz, tuna sandwiches are an inferior good.arrow_forward

- In the preceding diagram what areas represent consumers surplus at the equilibrium price of PE? At PC?arrow_forward8. U.S. government price supports for milk led to an unceasing surplus of milk. In an effort to reduce the surplus about a decade ago, Congress offered to pay dairy farmers to slaughter cows. Use two graphs, one for the milk market and one for the meat market, to illustrate how this policy should have affected the price of meat. (Assume that meat is sold in an unregulated market.) Be sure to draw the inverse demand and supply curves and label your axes. Explain clearly.arrow_forwardFigure: Leonard's Demand for Pecan Pie) Look at Leonard's weekly demand curve for slices of pie. How many slices of pie is Leonard willing to buy at $3 per slicearrow_forward

- 8. Total economic surplus The following graph plots the supply and demand curves in the market for VR headsets. Use the black point (plus symbol) to indicate the equilibrium price and quantity of VR headsets. Then use the green point (triangle symbol) to fill the area representing consumer surplus, and use the purple point (diamond symbol) to fill the area representing producer surplus. (?) PRICE (Dollars per headset) 350 315 280 245 210 175 140 105 70 35 0 0 Demand Supply 55 110 165 220 275 330 385 440 495 QUANTITY (Millions of headsets) Total surplus in this market is $ 550 million. + Equilibrium Consumer Surplus Producer Surplusarrow_forward6. Determinants of demand The following graph input tool shows the demand for sedans in New York City. For simplicity, assume that all sedans are identical and sell for the same price. Initially, the calculator shows market demand under the following circumstances: average household income is $50,000 per year, the price of a gallon of regular unleaded gas is $3 per gallon, and the price of a subway ride is $1.50. Use the graph input tool to help you answer the questions that follow. (Note: You will not be graded on any adjustment made to the graph used in the tool.) PRICE (Thousands of dollars per sedan) Demand 100 200 300 400 500 600 700 800 900 QUANTITY (Sedans per month) Graph Input Tool Price of a sedan (Thousands of dollars) Quantity of sedans (Sedans per month) Average Income (Thousands of dollars) Price of gasoline (Dollars per gallon) Price of a subway ride Suppose that the price of a sedan decreased from $25,000 to $20,000. This would cause a 25 450 50 $3.00 $1.50 Suppose that…arrow_forwardThe table below represents the market for DVDS. The value of consumer surplus is $__________milon (Enter your reaponse as an integer)arrow_forward

- 9. Shirts in supply or demana 11 The following graph shows the market for croissants in San Diego, where there are over 1,000 bakeries at any given moment. Suppose an innovation in the baking process makes it possible to produce more croissants at a lower cost than ever before. Show the effect of this change on the market for croissants by shifting one or both of the curves on the following graph, holding all else constant. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. PRICE (Dollars per croissant) QUANTITY (Croissants) Supply Demand Demand T Supply ?arrow_forward5. Complete the sentences: A demand curve shows the quantity demanded at each possible holding the other factors that influence purchases. The quantity demanded is the amount of a good that consumers are willing to given price, holding the other factors that influence purchases. Changes in the quantity demanded in response to changes in price are A change in any relevant factor other than the price of the good causes at aarrow_forwardMarcus buys a tablet for $5,000. What determines the size of consumer surplus Marcus receives? Explain.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education