ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

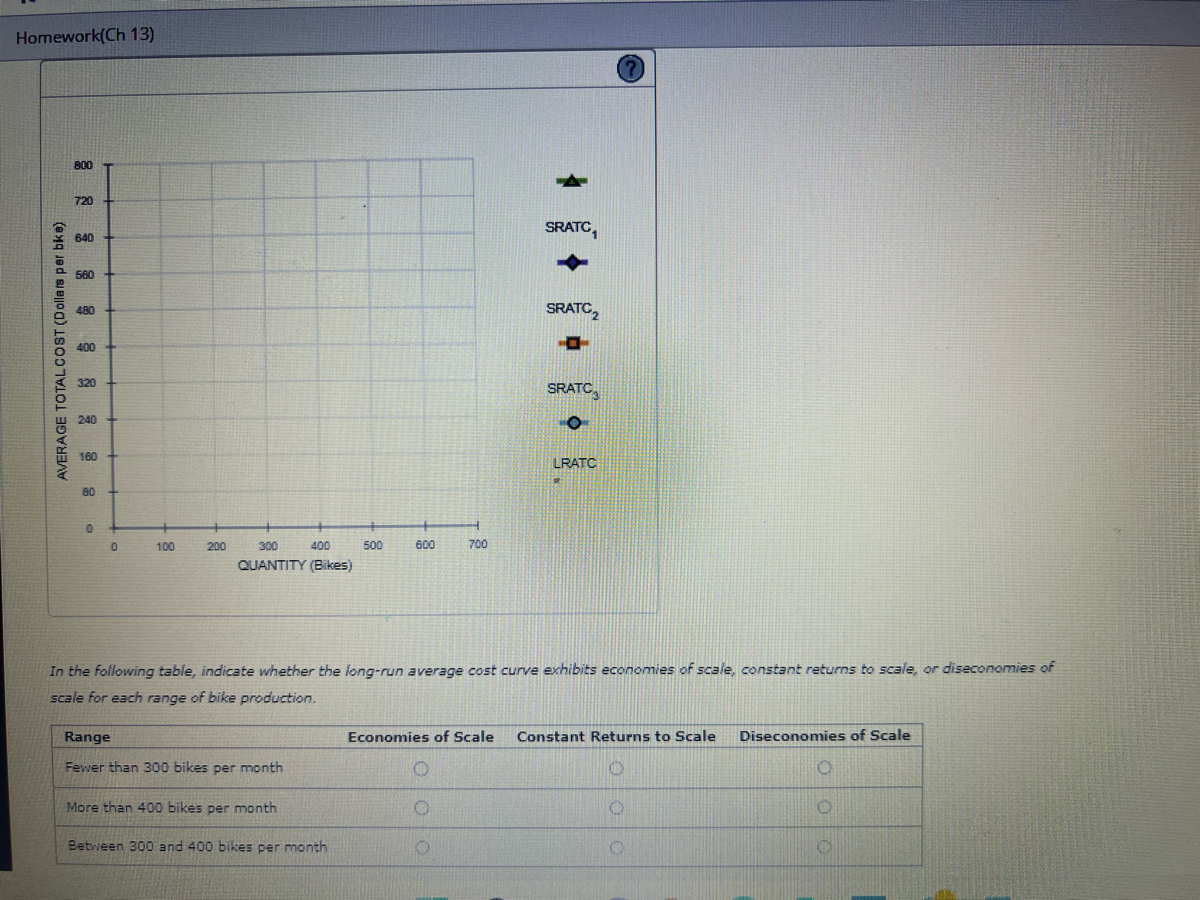

Transcribed Image Text:Homework(Ch 13)

AVERAGE TOTALCOST (Dollars per bike)

800

720

640

560

480

400

320

240

160

80

0

0

100

200

300

400

QUANTITY (Bikes)

Range

Fewer than 300 bikes per month

More than 400 bikes per month

500

Between 300 and 400 bikes per month

600

700

SRATC

In the following table, indicate whether the long-run average cost curve exhibits economies of scale, constant returns to scale, or diseconomies of

scale for each range of bike production.

0

O

SRATC₂

SRATC

O

LRATC

Economies of Scale Constant Returns to Scale

Diseconomies of Scale

O

O

Transcribed Image Text:3.cengage.com/static/nb/ui/evo/index.html?deploymentid=5981412232614779684085777463&eISBN=9780357133576&id=1498546365&sna... A

<

CENGAGE MINDTAP

Homework(Ch 13)

5. Costs in the short run versus in the long run

Ike's Bikes is a major manufacturer of bicycles. Currently, the company produces bikes using only one factory. However, it is considering expanding

production to two or even three factories. The following table shows the company's short-run average total cost (SRATC) each month for various levels

of production if it uses one, two, or three factories. (Note: Q equals the total quantity of bikes produced by all factories.)

Number of Factories Q = 100

1

360

2

540

3

720

Q = 200

200

300

400

.

Average Total Cost

(Dollars per bike)

Q = 300

Q = 400

240

160

160

160

160

240

Q = 500 Q = 600

400

720

300

540

200

360

Suppose Ike's Bikes is currently producing 500 bikes per month in its only factory. Its short-run average total cost is $

per bike.

Suppose Ike's Bikes is expecting to produce 500 bikes per month for several years. In this case, in the long run, it would choose to produce bikes

using

Q Search this course

Ⓒ

On the following graph, plot the three SRATC curves for Ike's Bikes from the previous table. Specifically, use the green points (triangle symbol) to plot

its SRATC curve if it operates one factory (SRATC₁); use the purple points (diamond symbol) to plot its SRATC curve if it operates two factories (

OLD

O

X

7:59 PM

7/11/2022

Expert Solution

arrow_forward

Introduction:

The average total cost is determined by dividing the total production cost by the total output. In other words, the average cost is the total fixed and variable costs of the firm divided by the total number of units produced. Using the average total cost, production managers determine which level of production can increase profitability. To calculate the total cost of production per unit produced, the average total cost accounts for both fixed and variable costs.

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Nonearrow_forwardWhich of the curves in the following graph is the average total cost curve?arrow_forwardFill in the space (d) in the table below associated with the firm William Perry, Inc., that delivers refrigerators in the Chicago area, using the two inputs of labor and trucks. Number of Amount of Trucks Labor 2 2 2 2 2 2 2 0 1 2 3456 Total Output 0 75 (c) 380 (f) Average Product of Labor (a) (b) 100 (d) (e) 75 Marginal Product of Labor 100 50 (g) 0arrow_forward

- Section 11.5 The Short-Run and Long-Run Average Total Cost Curves exhibit 1 SRATC for small plant SRATC for medium plant SRATC tor large plant LRATC B $500 $400 Economies of Scale Constant Returns to Saie 1,000 1,200 Quantity of Computers (per day) Notice that the long-run average total cost (LRATC) curve is much flatter than the short-run average total cost (SRATC) curve. This is because firms can be more flexible in the long run-they can choose which short-run cost curve they want to operate along, by choosing their plant scale. But they cannot do this in the short run, during which they are stuck with their existing short-run cost curve. That is, in the short run, the firm operates with the short-run curve it has based on past decisions. However, in the lang run, the firm is able to choose the short-run curve it wants to use. In Exhibit 1 above, explain why the curve between A and B looks different than the curve from A to C. Provide an example of how a firm could opt to follow the…arrow_forwardips Under decreasing returns to scale, average cost cost curve. as the quantity produced increases. Over this range of output, the marginal cost curve is Grade It Now the average Save & Continuearrow_forwardCosts and Profit Maximization: Work It Out 1 Suppose Margie decides to lease a photocopier and open up a black-and-white photocopying service in her dorm room for use by faculty and students. Her total cost, as a function of the number of copies she produces per month, is given in the table. Number of Photocopies Per Month Total Cost Fixed Cost Variable Cost Total Revenue Profit 0 $100 1,000 $110 2,000 $125 3,000 $145 4,000 $175 5,000 $215 6,000 $285 a. Fill in the missing numbers in the table, assuming that Margie can charge 6 cents per black-and-white copy. Margie's fixed cost is: $ Variable cost, 0 photocopies/month: $ Variable cost, 1,000 photocopies/month: $ Variable cost, 2,000 photocopies/month: $ Variable cost, 3,000 photocopies/month: $ Variable cost, 4,000 photocopies/month: $…arrow_forward

- shows the long-run average costs for Inmode, a manufacturer of Internet modems. Quantity per Day Average Cost ($) a) At what output is minimum efficient scale achieved? Output: b) with what output do diseconomies of scale begin? Output: 1 95 2 85 3 75 4 70 5 65 6 65 7 75 8 100arrow_forwardsolution plzarrow_forwardWhich of the following statements about average and marginal cost is INCORRECT? (2)(1) The marginal cost curve cuts both the average cost and average variable costcurves at their minimum points;(2) The marginal cost curve cuts both the average fixed cost and average variablecost curves at their minimum points;(3) The marginal cost curve lies below the average cost curve when average costis decreasing;(4) Marginal cost is the change in total cost when one extra unit of output isproduced.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education