Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

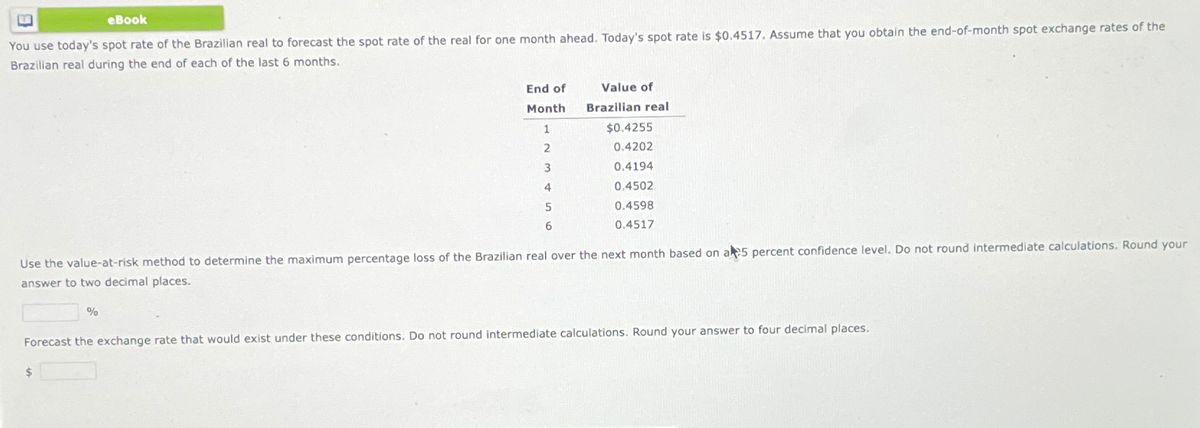

Transcribed Image Text:eBook

You use today's spot rate of the Brazilian real to forecast the spot rate of the real for one month ahead. Today's spot rate is $0.4517. Assume that you obtain the end-of-month spot exchange rates of the

Brazilian real during the end of each of the last 6 months.

End of

Value of

Month

Brazilian real

1

$0.4255

2

0.4202

3

0.4194

4

0.4502

5

6

0.4598

0.4517

Use the value-at-risk method to determine the maximum percentage loss of the Brazilian real over the next month based on a 5 percent confidence level. Do not round intermediate calculations. Round your

answer to two decimal places.

%

Forecast the exchange rate that would exist under these conditions. Do not round intermediate calculations. Round your answer to four decimal places.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose that 1 Danish krone could be purchased in the foreign exchange market today for $0.17. If the krone appreciated 7% tomorrow against the dollar, how many krones would a dollar buy tomorrow? Do not round intermediate calculations. Round your answer to four decimal places. ____ kronesarrow_forwardNonearrow_forwardHere are direct spot and forward markets quotes for EUR over three points in time: now (1/1/XX), one month later (2/1/XX), three months later (4/1/XX), and six months later (7/1/XX). 1/1/XX 2/1/XX 4/1/XX 7/1/XX EUR Spot 1.3075 1.3006 1.3605 1.3296 1 Month Forward 1.3271 1.3201 1.3809 1.3496 3 Month Forward 1.3470 1.3399 1.4016 1.3698 6 Month Forward 1.3672 1.3600 1.4226 1.3904 On 1/1/XX, Dell sold a 6 month forward contract of EUR 1,000,000 to Chase. As a result IBM will incur a when the contract expires: O Loss of $37,600 O Profit of $37,600 O Loss of $23,00 O Profit of $23,000arrow_forward

- Six-month T-bills have a nominal rate of 3%, while default-free Japanese bonds that mature in 6 months have a nominal rate of 1.50%. In the spot exchange market, 1 yen equals $0.008. If interest rate parity holds, what is the 6-month forward exchange rate? Do not round intermediate calculations. Round your answer to six decimal places. Aarrow_forwardYou travel to Cancun Mexico for spring break. The current exchange rate is 14 pesos to the dollar. When you arrive, you convert $3,100 into how many pesos? Multiple Choice 43,400 221 43,350 43,380arrow_forwardSuppose a German importer owes an Australian exporting company 150,000 AUD, due in three months. S_0 (EUR/AUD) 0.60 Se (EUR/AUD) 0.50 (0.3) and 0.65 (0.7) Premium on AUD call option R = EUR0.02 Exercise exchange rate E = 0.62 Time to expiry 3 months What is the expected value of payables in AUD under hedge Will the option to hedge be undertaken on the basis of expected spot rate? Explain.arrow_forward

- The $/€ spot exchange rate is $1.10/€ and the 120-day forward discount rate for the euro is 20%. Find the 120-day forward exchange rate for the Euro. $1.027. $0.9600. $1.320. $1.173. $1.100.arrow_forwardThe current U.S. dollar-yen spot rate is 150\/$. If the 90-day forward exchange rate is 148 ¥/$ then the yen is selling at a per annum of %. Reminder: Please use one decimal in your answer entry and dot as the decimal point.arrow_forwardPlease Help The Swiss Franc is trading at 1.1464 $/ SFr, the euro is trading at 1.0828 $/euro. If you can buy or sell SFr/euro at 0.9451, is there an arbitrage? If so, how much can you make with one round - trip using $1,000,000 ? Please Helparrow_forward

- The EUR/USD quotes 1.1295-1.1305 and you implement a long position for 100,000 €. 2 days later the EUR/USD shows 1.1431-1.1441. What is your P&L? a)1260 $ b)1460 $ c)1260 € d)1460 €arrow_forwardUse the information below to answer the following question. So($/€) F360 ($/€) Exchange Rate $ 1.45 € 1.00 = $ 1.48 = € 1.00 Interest Rate APR is i€ 4% 3% If you borrowed $1,000,000 for one year, how much money would you owe at maturity? Short Answer Toolbar navigation BIUS $1,524,400 A RN KEarrow_forwardUsing info in the table below calculate how many USD you would have to pay 2 months from now to buy EUR 10,000 if you lock into a 2 month forward contract now. 98) Settings. 10,966 11,394 11,044 14,895 1) G10 11) All G10 12) 13) 14) 15) 16) 17) 18) 19) 20) 21) 22) titokb US Euro Japan UK Canada Australia ON TN Spot SN 1W 1M Switzerland 2M Denmark 3M Norway 6M Sweden N. Zealand 90) FX Markets Overview 91) FX Forwards 92) FX Options and Volatility 93) Economics 30) Forward Term Structures - Points | XDSH >> EURUSD 2) Asia 3) Europe/Africa 4) Latin America 5) Middle East 6) Metals .60 .63 1.1005 .69 -2.06 4.78 -14.26 20.22 -63.47 38.90 -128.04 56.04 -189.12 100.88 -370.08 168.84 -698.24 1Y 40) Term Structure Chart - Outrights | XCRV >> Chart 136.000000- 134.000000 132.000000- 130.000000- 128.000000 126.000000- 124.835098 124.000000 Graph terms from TOD USDJPY GBPUSD USDCAD AUDUSD NZDUSD USDCHF USDDKK USDNOK USDSEK -11.01 .31 -.22 .22 -.07 -.94 -3.83 -5.55 -5.84 -2.04 .26 -.21 .17 -.02…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education