FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

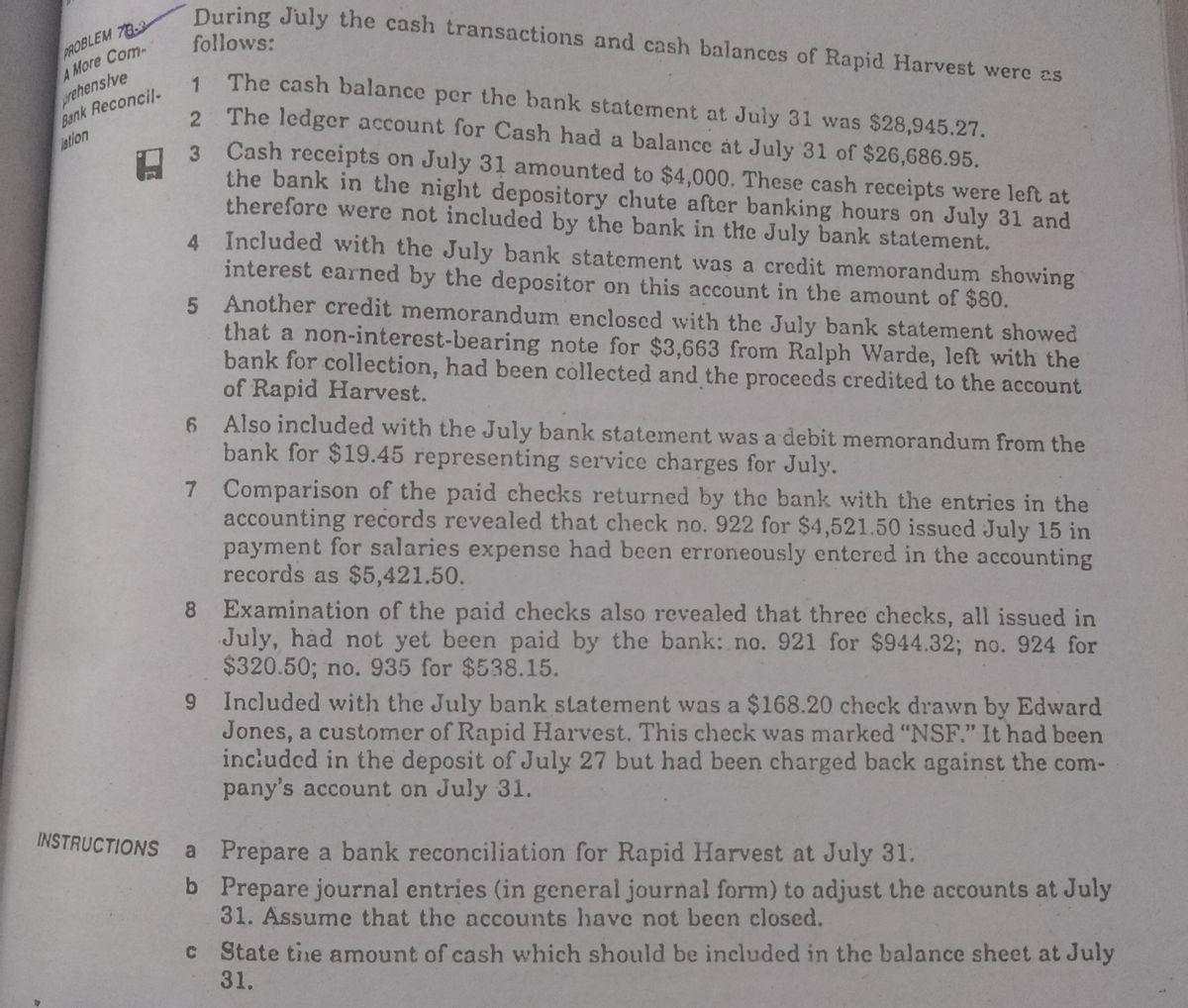

Transcribed Image Text:During July the cash transactions and cash balances of Rapid Harvest were as

PROBLEM 782

A More Com-

prehenstve

Bank Reconcil-

follows:

1. The cash balance per the bank statement at July 31 was $28,945.27.

2 The ledger account for Cash had a balance át July 31 of $26,686.95.

latlon

Cash receipts on July 31 amounted to $4,000. These cash receipts were left at

the bank in the night depository chute after banking hours on July 31 and

therefore were not included by the bank in the July bank statement.

4 Included with the July bank statement was a credit memorandum showing

interest earned by the depositor on this account in the amount of $80.

5 Another credit memorandum enclosed with the July bank statement showed

that a non-interest-bearing note for $3,663 from Ralph Warde, left with the

bank for collection, had been collected and the proceeds credited to the account

of Rapid Harvest.

6 Also included with the July bank statement was a debit memorandum from the

bank for $19.45 representing service charges for July.

7 Comparison of the paid checks returned by the bank with the entries in the

accounting records revealed that check no. 922 for $4,521.50 issued July 15 in

payment for salaries expense had been erroneously entcred in the accounting

records as $5,421.50.

8 Examination of the paid checks also revealed that three checks, all issued in

July, had not yet been paid by the bank: no. 921 for $944.32; no. 924 for

$320.50; no. 935 for $538.15.

9 Included with the July bank statement was a $168.20 check drawn by Edward

Jones, a customer of Rapid Harvest. This check was marked "NSF." It had been

included in the deposit of July 27 but had been charged back against the com-

pany's account on July 31.

INSTRUCTIONS a Prepare a bank reconciliation for Rapid Harvest at July 31.

b Prepare journal entries (in general journal form) to adjust the accounts at July

31. Assume that the accounts have not becn closed.

c State tihe amount of cash which should be included in the balance sheet at July

31.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The following data were accumulated for use in reconciling the bank account of Creative Design Co. for August 20Y6: Cash balance according to the company’s records at August 31, $42,920. Cash balance according to the bank statement at August 31, $56,300. Checks outstanding, $25,390. Deposit in transit not recorded by bank, $13,325. A check for $150 in payment of an account was erroneously recorded in the check register as $1,500. Bank debit memo for service charges, $35. Journalize the entries that should be made by the company that (a) increase cash and (b) decrease cash. If an amount box does not require an entry, leave it blank.arrow_forwardThe cash account for Pala Medical Co. at June 30, 20Y1, indicated a balance of $93,115. The bank statement indicated a balance of $125,800 on June 30, 20Y1. Comparing the bank statement and the accompanying canceled checks and memos with the records revealed the following reconciling items: a. Checks outstanding totaled $30,080. b. A deposit of $19,240, representing receipts of June 30, had been made too late to appear on the bank statement. c. The bank collected $24,075 on a $2,500 note, including interest of $1,575. d. A check for $1,800 returned with the statement had been incorrectly recorded by Pala Medical Co. as $180. The check was for the payment of an obligation to Skyline Supply Co. for a purchase on account. e. A check drawn for $390 had been erroneously charged by the bank as $930. f. Bank service charges for June amounted to $50. Instructions 1. Prepare a bank reconciliation. Refer to the Amount Descriptions list provided for the exact wording of the answer choices for…arrow_forwardThe following data were accumulated for use in reconciling the bank account of Mathers Co. for July: Cash balance according to the company's records at July 31 $14,720. Cash balance according to the bank statement at July 31, $15,730. Checks outstanding, $2,990. Deposit in transit, not recorded by bank, $2,400. A check for $270 in payment of an account was erroneously recorded in the check register as $720. Bank debit memo for service charges, $30. a. Prepare a bank reconciliation, using the format shown inarrow_forward

- The following data were accumulated for use in reconciling the bank account of Nakajima Co. for July: 1. Cash balance according to the company’s records at July 31, $49,910. 2. Cash balance according to the bank statement at July 31, $48,250. 3. Checks outstanding, $4,460. 4. Deposit in transit, not recorded by bank, $6,450. 5. A check for $590 issued in payment of an account was erroneously recorded in the check register as $950. 6. Bank debit memo for service charges, $30. Required: Journalize the entry or entries that should be made by the company. Refer to the chart of accounts for the exact wording of the account titles. CNOW journals do not use lines for journal explanations. Every line on a journal page is used for debit or credit entries. CNOW journals will automatically indent a credit entry when a credit amount is entered. CHART OF ACCOUNTSNakajima Co.General Ledger ASSETS 110 Cash 111 Petty Cash 120 Accounts Receivable 131 Notes…arrow_forwardHow would I input the formulas into excel to get those numbers for the statement of cash flowsarrow_forwardThe cash account for Coastal Bike Co. at October 1, 20Y9, indicated a balance of $32,991. During October, the total cash deposited was $139,960, and checks written totaled $137,747. The bank statement indicated a balance of $43,370 on October 31, 20Y9. Comparing the bank statement, the canceled checks, and the accompanying memos with the records revealed the following reconciling items: a. Checks outstanding totaled $6,476. b. A deposit of $1,779 representing receipts of October 31, had been made too late to appear on the bank statement. c. The bank had collected for Coastal Bike Co. $5,250 on a note left for collection. The face of the note was $5,000. d. A check for $580 returned with the statement had been incorrectly charged by the bank as $850. e. A check for $210 returned with the statement had been recorded by Coastal Bike Co. as $120. The check was for the payment of an obligation to Rack Pro Co. on account. f. Bank service charges for October amounted to $28. g. A check for…arrow_forward

- Peterson Company's general ledger shows a cash balance of $7,720 on May 31. May cash receipts of $1,340, included in the general ledger balance, are placed in the night depository at the bank on May 31 and processed by the bank on June 1. The bank statement dated May 31 shows an NSF check for $190 and a service fee of $60. The bank processes all checks written by the company by May 31 and lists them on the bank statement, except for one check totaling $1,710. The bank statement shows a balance of $7,840 on May 31. Prepare a bank reconciliation to calculate the correct ending balance of cash on May 31. (Amounts to be deducted should be indicated with a minus sign.) Bank's Cash Balance Before reconciliation After reconciliation PETERSON COMPANY Bank Reconciliation May 31 SA Company's Cash Balance Before reconciliation 0 After reconciliation SA 0arrow_forwardThe following information is available to reconcile Branch Company’s book balance of cash with its bank statement cash balance as of July 31. On July 31, the company’s Cash account has a $25,507 debit balance, but its July bank statement shows a $27,043 cash balance. Check No. 3031 for $1,180, Check No. 3065 for $366, and Check No. 3069 for $1,948 are outstanding checks as of July 31. Check No. 3056 for July rent expense was correctly written and drawn for $1,280 but was erroneously entered in the accounting records as $1,270. The July bank statement shows the bank collected $7,000 cash on a note for Branch. Branch had not recorded this event before receiving the statement. The bank statement shows an $805 NSF check. The check had been received from a customer, Evan Shaw. Branch has not yet recorded this check as NSF. The July statement shows a $11 bank service charge. It has not yet been recorded in miscellaneous expenses because no previous notification had been received.…arrow_forwardThe following information is available to reconcile Branch Company's book balance of cash with its bank statement cash balance as of July 31. a. On July 31, the company's Cash account has a $25,127 debit balance, but its July bank statement shows a $27,260 cash balance. b. Check Number 3031 for $1,420, Check Number 3065 for $486, and Check Number 3069 for $2,188 are outstanding checks as of July 31. c. Check Number 3056 for July rent expense was correctly written and drawn for $1,290 but was erroneously entered in the accounting records as $1,280. d. The July bank statement shows the bank collected $9,000 cash on a note for Branch. Branch had not recorded this event before receiving the statement. e. The bank statement shows an $805 NSF check. The check had been received from a customer, Evan Shaw. Branch has not yet recorded this check as NSF. f. The July statement shows a $14 bank service charge. It has not yet been recorded in miscellaneous expenses because no previous notification…arrow_forward

- Alaska Impressions Co. records all cash receipts on the basis of its cash register tapes. Alaska Impressions discovered during October 20Y3 that one of its sales clerks had stolen an undetermined amount of cash receipts by taking the daily deposits to the bank. The following data have been gathered for October: Line Item Description Amount Cash in bank according to the general ledger $11,680 Cash according to the October 31, 20Y3, bank statement 13,275 Outstanding checks as of October 31, 20Y3 3,670 Bank service charge for October 40 Note receivable, including interest collected by bank in October 2,100 No deposits were in transit on October 31. a. Determine the amount of cash receipts stolen by the sales clerk.fill in the blank 1 of 1$arrow_forwardMDB Company provided the following data pertaining to the cash transactions and bank account for the month of May: Cash balance per accounting record Cash balance per bank statement Bank service charge Bank Debit Memo Php 1,719,000 3,195,000 10,000 5,000 685,000 500,000 810,000 Outstanding checks Deposits made on May 30 and not yet reflected in the bank statement Collections made by the bank from a customer promissory note, the principal amount of Php800,000 with interest Check No. 1234 issued to a supplier entered in the accounting record as P210,000 but deducted in the bank statement at an erroneous amount of Customer check returned by the bank marked as NSF. No entry has been made to record the returned check 21,000 77,000 What is the adjusted cash in bank?arrow_forwardThe bank statement for Jeffrey Co. indicates a balance of $8,785 on October 31. After the journals for October had been posted, the cash account had a balance of $8,998. a. Cash sales of $945 had been erroneously recorded in the cash receipts journal as $495. b. Deposits in transit not recorded by bank, $778. c. Bank debit memo for service charges, $40. d. Bank credit memo for note collected by bank, $23,985 plus $885 interest. e. Bank debit memo for $756 NSF (not sufficient funds) check from Calin Sams, a customer. f. Checks outstanding, $1,860. Record the appropriate journal entries that would be necessary for Jeffrey Co. Record the entry that increases cash first. If an amount box does not require an entry, leave it blank.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education