ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

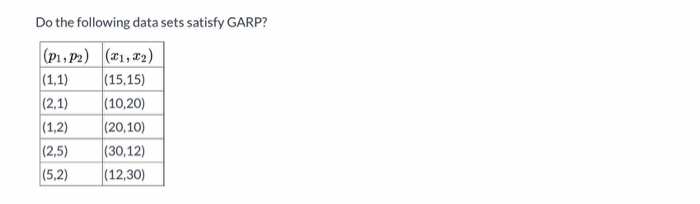

Does the following dataset satisfy GARP?

Transcribed Image Text:Do the following data sets satisfy GARP?

(P1, P2) (21, 22)

|(15,15)

|(10,20)

(20,10)

(30,12)

(12,30)

|(1,1)

(2,1)

(1,2)

(2,5)

|(5,2)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- q11-arrow_forwardYou estimated a regression with the following output. Source | SS df MS Number of obs = 335 -------------+---------------------------------- F(1, 333) = 69555.83 Model | 211169628 1 211169628 Prob > F = 0.0000 Residual | 1010979.01 333 3035.97301 R-squared = 0.9952 -------------+---------------------------------- Adj R-squared = 0.9952 Total | 212180607 334 635271.28 Root MSE = 55.1 ------------------------------------------------------------------------------ Y | Coef. Std. Err. t P>|t| [95% Conf. Interval] -------------+---------------------------------------------------------------- X | 44.15183 .1674102 263.73 0.000 43.82251 44.48114 _cons | 31.63715 16.49849 1.92 0.056 -.8172452 64.09155…arrow_forwardIn the linear model ,E (X*u) = a)X*u b) 0 c) u d) none of tha abovearrow_forward

- (e) Suppose you have been given the following ordinary least squares (OLS) regression result. Estimated Long Run Coefficients using the ARDL Approach ARDL (1,2,2,2,0,2) selected based on Akaike Information Criterion Dependent variable is LY 33 observations used for estimation from 1987 to 2019 T-Ratio [Prob.] 4.6671[0.000] 4.6678[0.051] 7.9897[0.043] -4.802[0.009] 2.3898[0.028] 1.0498[0.308] Regressor Coefficient Standard Error 0.36068 0.45447 LK 0.077280 LM 0.097363 0.48751 -0.41208 0.19057 0.52521 LE 0.061017 LF 0.085800 LT 0.079744 C 0.500320 where, Y = Economic growth K = Capital M = Employment E = Electricity consumption F = Foreign direct investment T= Technology (i) Write the regression equation. Interpret the estimated coefficients. (ii) Which explanatory variables are significant at the 1%, 5% and 10% level? Which variables are insignificant? Briefly explain.arrow_forwardYou are given the following data: The regression equation is: A. -0.66 B. -1.20 (X'X)*¹ C. 1.12 O D. 2.06 = 1.3 2.1 0.8 -1.4 1.9 2.1 -1.4 s² = 0.86. T = 103 The correlation between ₁ and 3 (i.e., corr(Â₁, Â3)) is: -1.6] 1.9 (X'y) = 2.9 3.4 0.8 Yt = B₁ + B₂X2+ + B3X3t + Ut.arrow_forwardYou estimated a regression with the following output. Source | SS df MS Number of obs = 268 -------------+---------------------------------- F(1, 266) = 23.48 Model | 668419.175 1 668419.175 Prob > F = 0.0000 Residual | 7572666.51 266 28468.6711 R-squared = 0.0811 -------------+---------------------------------- Adj R-squared = 0.0777 Total | 8241085.68 267 30865.4895 Root MSE = 168.73 ------------------------------------------------------------------------------ Y | Coef. Std. Err. t P>|t| [95% Conf. Interval] -------------+---------------------------------------------------------------- X | 1.014128 .2092916 4.85 0.000 .6020489 1.426207 _cons | 9.173163 21.13463 0.43 0.665 -32.43929 50.78561…arrow_forward

- In the model Y = Bo +B 1X 1 + B 2X 2 + 8, which of these parameters represents a coefficient of an independent variable? the Y the X1 the B1 the earrow_forwardBased on the following data, estimate the slope of the equation using OLS (3 significant digits in final answer): K=ẞ1+ B2J+ε Observation. 1 2 3 U 2 4 9 K 16 15 14 Answer:arrow_forwardYou estimated a regression with the following output. Source | SS df MS Number of obs = 223 -------------+---------------------------------- F(1, 221) = 17592.99 Model | 182392130 1 182392130 Prob > F = 0.0000 Residual | 2291176.96 221 10367.3166 R-squared = 0.9876 -------------+---------------------------------- Adj R-squared = 0.9875 Total | 184683307 222 831906.786 Root MSE = 101.82 ------------------------------------------------------------------------------ Y | Coef. Std. Err. t P>|t| [95% Conf. Interval] -------------+---------------------------------------------------------------- X | 11.97037 .0902481 132.64 0.000 11.79252 12.14823 _cons | 74.40159 10.96696 6.78 0.000 52.78839 96.01479…arrow_forward

- The models below have been estimated using monthly data for the period 2000: 1-2020: 12. The natural logarithm of the variables used in this model is taken and the transaction is made. D08 is the dummy variable that takes a value of 1 in 2008 and after and 0 in other periods. s.e. indicates the standard error. Comment on the coefficients of variables D08 and (X2t * D08) in the model (3) above.arrow_forwardA researcher investigating whether government expenditure crowds out investment estimates a regression on data for 30 countries. I-investment; G-government recurrent expenditure; Y=gross domestic product; all measured in $US billion. P= population measured in million. Standard errors are in parentheses. Î= 18.10 (7.79) R² = 0.99 1.07G + 36Y (0.14) (0.02) She suspects that countries with higher GDP may have more variability in their investment. She sorts the observations by increasing size of gdp per capita (Y)and estimates the regression again for the 11 countries with the lowest gdp(Y)and the 11 countries with the largest gdp(Y). The RSS1 from the first regression is 7186. The RSS2 from the second regresison is 28101. Perform a Goldfeld-Quandt Test at a 5% significance level. a. The test statistic for this test is 0.256 b. The critical value defining the rejection region for Ho is 3.18 c. Is there heterscedasticity? Yes=1 or No-0. The answer is 0arrow_forwardBureau of Economic Analysis in the USA is responsible for construction and maintenance of national income and product accounts (NIPA). Measurement began in the 1930s due to frustration of Roosevelt and Hoover trying to design policies to combat the Great Depression. Simon Kuznets (Nobel laureate) was commissioned to develop initial methodology and estimates. In 1947, the process became much more consistent. Methodologies have frequently been changed (improved?) as a result of advances in economics, accounting, and data collection. Past data are then revised to reflect new definitions. On the following information, calculate GNP at factor cost. Whether GNPFC derive from income method equivalent to expenditure method? S.No. Items Rs. (In Crores) 1 Private final consumption expenditure 1000 2 Net domestic capital formation (Investment) 200 3 Profit 400 4 Compensation of employers (Wages and salaries) 800 5 Rent 250 6 Government final consumption expenditure…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education