ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

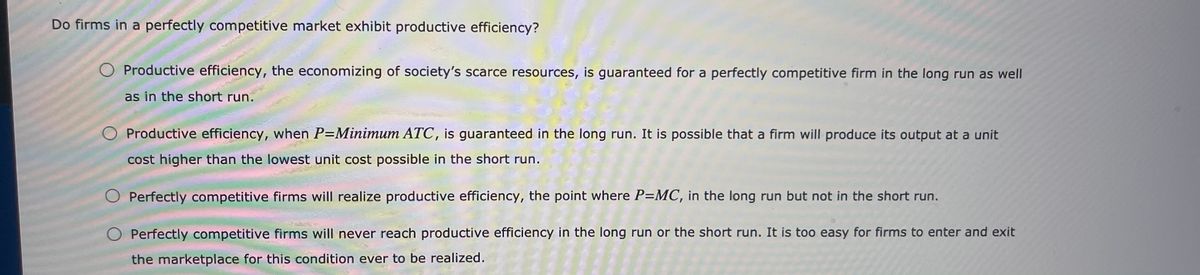

Transcribed Image Text:Do firms in a perfectly competitive market exhibit productive efficiency?

O Productive efficiency, the economizing of society's scarce resources, is guaranteed for a perfectly competitive firm in the long run as well

as in the short run.

Productive efficiency, when P=Minimum ATC, is guaranteed in the long run. It is possible that a firm will produce its output at a unit

cost higher than the lowest unit cost possible in the short run.

Perfectly competitive firms will realize productive efficiency, the point where P=MC, in the long run but not in the short run.

Perfectly competitive firms will never reach productive efficiency in the long run or the short run. It is too easy for firms to enter and exit

the marketplace for this condition ever to be realized.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The optimal output rule for a perfectly competitive firm is to produce that quantity where A. P = MC in the long run, but in the short run to produce that quantity where MC = %3D ATC. O B. MC = ATC in the short run. C. P = MC no matter what the time period, provided that price is greater than average variable cost. D. P = MC no matter what the time period, provided that price is greater than %3D average total cost.arrow_forward3arrow_forwardOnly typed answerarrow_forward

- please also do the graph and the choices for the first blank is 2000, 7500, 8000, 10000 and the choices for the second blank is profit or economic loss thank you!!!arrow_forwardImagine a firm in a competitive market comes up with a new production method, which halves its marginal cost at all levels of Q. Fixed costs are unaffected. Which of the following statements are true? O a. The firm's AC at all levels of Q would be lower. O b. The firm would extract an innovation rent from selling at the market price with lower costs. Oc. The firm's point of minimum AC would be a higher level of Q. O d. The innovation would immediately cause the market price to drop.arrow_forwardBecause perfectly competitive firms are price takers, a permanent increase in the market demand does not change the price of the product in either the short run or long run. O A. True O B. Falsearrow_forward

- Please see the attached23arrow_forwardA competitive firm produces a product using the function f(x1, x2) = 8xx. The factor prices are p1 = $2.50 and p2 = $4 and 1/21/2 the firm can purchase as much of either factor at the given prices. What is the firm's marginal cost? O a. $1.74 O b. $1.07 O . $2.32 O d. None of the abovearrow_forward7. You are economic consultant for Jack, who farms raw cotton in a perfectly competitive market. One day he gives you the following data at his present level of production: Output = 2000 pounds, market price = $5.00, total cost =$8000, fixed cost=$2000, marginal cost=$5. The minimum of AVC occurs at {1000 pounds at $2} and the minimum of ATC at {1500 pounds at $3.5}. Please help Jack with the following questions based on the above figures: a. Draw a graph for the raw cotton market and a graph for Jack’s farm current situation that includes MC, ATC, and AVC, labeling all relevant points on axes with numerical values. Is Jack maximizing the profit (minimizing the loss)? Why or why not? Label the total profit/loss area. b. Suppose more farmers enter the raw cotton market until the market price is $3.00 per pound. On the same graphs, show the effect of this change in the market place. Would you like to suggest Jack leaving the market in the short run? Explain your answearrow_forward

- Profit is the incentive that drives our market economy. Firms make production, pricing, andhiring decisions based on their quest for profit. But what happens when a firm discoversthat it can make dramatically higher profits by stopping production altogether? In December2000, due to wild swings in the market for electricity, Kaiser Aluminium faced just such adecision.Kaiser Aluminium had contracted with Bonneville power for all of its electricity needs andfound itself in the unique position of being an electricity consumer and, potentially, anelectricity reseller. By December 2000, Kaiser faced a difficult decision of continuing itscurrent aluminium production and profit levels, or closing the plant to dramatically increaseits profit by simply reselling its electricity.When making production decisions, firms must consider both their costs and revenues. Oneimportant concern for many firms is utility costs. In 1996, Kaiser Aluminium Corporation inSpokane, Washington, entered into a…arrow_forwardLooking to see how to resolvearrow_forwardWhich of the following best explains why a firm would not stop producing if the loss is less than its fixed costs? O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover ATC and some MC. O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover ATC and some FC. O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover AVC and some FC. O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover AVC and some MC.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education