ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

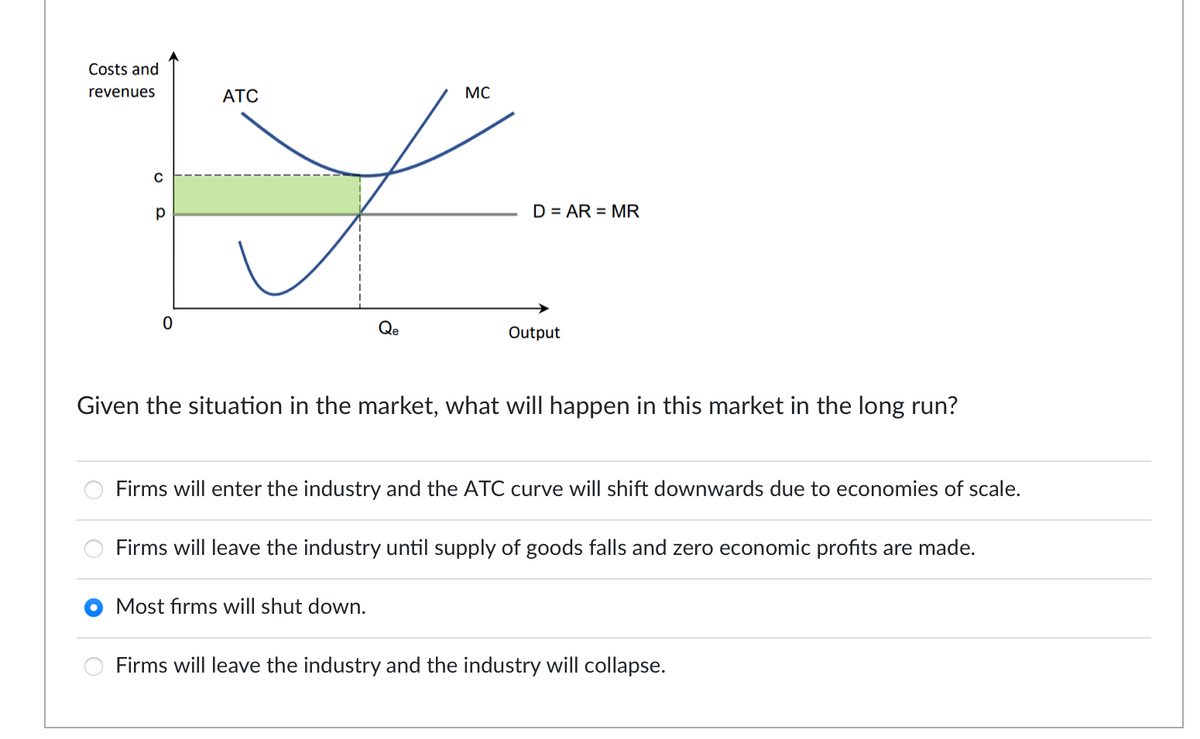

Transcribed Image Text:**Graph Explanation:**

The graph displays economic cost and revenue curves. The horizontal axis represents output, while the vertical axis shows costs and revenues. The key components of the graph are:

- **ATC (Average Total Cost)** curve: Represents the average total cost per unit of output.

- **MC (Marginal Cost)** curve: Illustrates the additional cost of producing one more unit of output.

- **D = AR = MR (Demand = Average Revenue = Marginal Revenue)** line: Indicates the market demand and revenue conditions. It is a horizontal line, denoting price 'p', and reflects perfect competition.

- **Point C**: The intersection of the MC and D = AR = MR lines.

- **Qe**: The equilibrium output level where firms maximize profit or minimize loss.

The shaded green area between the price line 'p' and the ATC curve above it shows economic losses, as the average total cost is greater than the price per unit.

**Question:**

Given the situation in the market, what will happen in this market in the long run?

- ◯ Firms will enter the industry and the ATC curve will shift downwards due to economies of scale.

- ◯ Firms will leave the industry until the supply of goods falls and zero economic profits are made.

- ● Most firms will shut down.

- ◯ Firms will leave the industry and the industry will collapse.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please write to text formet answer but don't copy paste the answerarrow_forwardManagers of perfectly competitive firms must be cautious when deciding to permanently expand (or contract) the scale of production. What factors should go into the decision to expand the scale of production if the market price of your product increases? (select all that apply) A. Whether your product has a complement in consumption B. If the scale expansion is appropriate and not in excess C. If other firms are likely to enter the market D. Whether the price change is temporary or permanentarrow_forwardAt P4, this firm will: A graphThe graph shows the supply curves for a firm. Multiple Choice produce 10 units and earn only a normal profit. produce 30 units and earn only a normal profit. shut down in the short run. produce 30 units and realize a loss. MCarrow_forward

- In the long run when a perfectly competitive firm experiences positive economic profits firms exit the industry, the market supply curve shilts leftward, and the market price rises. firms enter the Industry, the market supply curve shifts rightward, and the market price fals firms enter the industry, the macket supply curve shifts rightward, and the market price rises firms exit the industry, the market supply curve shifts rightward. and the market price fallsarrow_forwardIf there were 10 firms in this market, the short-run equilibrium price of steel would be $______per ton. At that price, firms in this industry would ______(shut down/operate at a loss/ earn a positive profit/ earn zero profit). Therefore, in the long run, firms would__________(enter/ exit/ neither enter nor exit) the steel market. Because you know that competitive firms earn______(zero/ negative/ positive) economic profit in the long run, you know the long-run equilibrium price must be $_____per ton. From the graph, you can see that this means there will be_____(10/20/30) firms operating in the steel industry in long-run equilibrium.arrow_forwardA profit-maximizing firm decides to shut-down production in the short-run. Its total fixed cost of production is $100, i.e. TFC = $100. Which of the following statements is true? a If the firm produced, the firm's revenues would have been lower than $100. bIf the firm produced, the firm's total variable cost must be lower than $100. cIf the firm produced, the firm's losses would have been higher than $100. dIf the firm produced, the firm's total variable cost would have been higher than $100.arrow_forward

- P P₂ B C Q₂ D MC Firm entry occurs. Output Quantity Refer to the above figures for the typical firm in a competitive market. If the market demand curve is D3, what happens in the long run? A Firm exit occurs. ATC Most firms do nothing. D₂ Some existing firms increase capital input. D₂ D₁ Quantityarrow_forwardThe graph shown displays the cost curves for a firm in a perfectly competitive market. If the market price is $100, which of the following statements is true?graph_q10 This firm will earn positive profits in the short run. In the long run, the market supply curve will increase. Profits for this firm will decrease in the long run. I only I and II I and III I, II and IIIarrow_forwardI need solution of a,b,carrow_forward

- 10 The industry in the figure given below on the left consists of many firms with identical cost structures, and the industry experiences constant returns to scale. a. Draw the short-run market supply curve up to 4,000 units of output. Instructions: Use the tool provided (SRMSC) to draw the short-run market supply curve. Plot three points total. b. Draw the long-run market supply curve from zero to 4,000 units of output. Instructions: Use the tool provided (LRMSC) tool to draw the long-run market supply curve. Plot only the endpoints across the entire output range (0 to 4,000). Price ($) 50 40 40 Typical Firm Market Price ($) 50 MC ATC 40 30 AVC 20 20 10 0 10 20 20 30 Quantity 40 40 50 50 30 20 20 10 0 D Tools / LRMSC SRMSC 1000 2000 3000 4000 5000 Quantityarrow_forwardIf the market price of a product is $10 that lie between the minimum average variable cost $8 (AVC) and minimum average total cost $15 (ATC) of a firm, that firm will:___________ a) always shut down. b) always continue to produce.c) produce in the short run but shut down in the long run. d) produce in the long run but shut down in the short run. e) make positive economic profits.arrow_forwardIn a perfectly competitive market... Group of answer choices It will eventually reach long-run equilibrium. Economic profits will be driven down to zero in the short run Firms will compete for business by setting different prices at or above the prevailing equilibrium price A few firms will dominate the market share.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education