ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

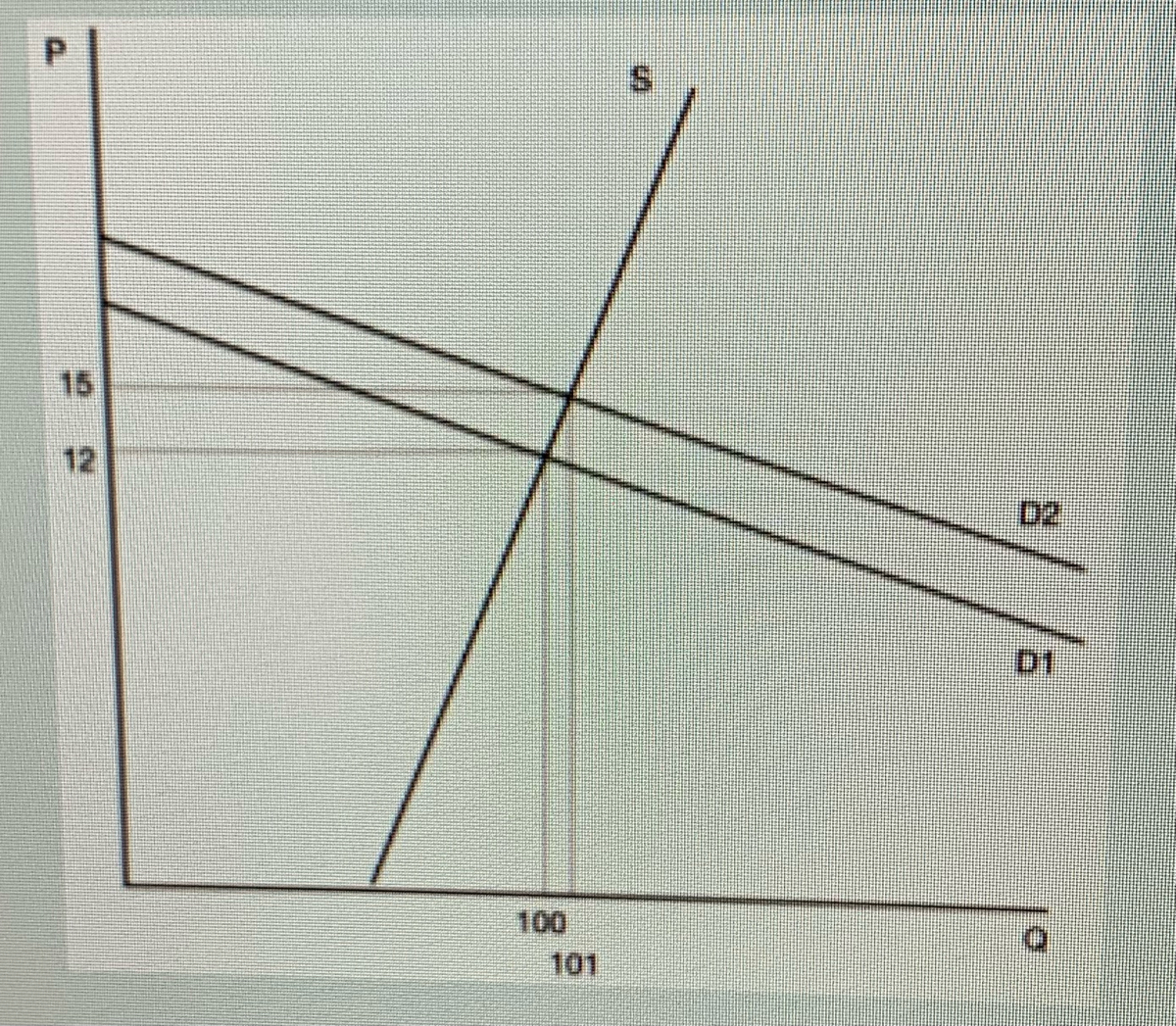

Transcribed Image Text:15

12

D2

100

101

Transcribed Image Text:Consider the supply and demand graph above showing a shift in demand from D1 to D2. Which of the following statements are true? (Select all that apply.)

O a The shift from D1 to D2 represents a tax

O b. The shift from D1 to D2 represents a subsidy.

O. A supply-side tax would have had the same effect on the market.

O d. Supply is inelastic.

O e. Producers will see a larger change in price than consumers.

O f. Supply is more elastic than demand.

Og. Demand is elastic.

Oh The amount of the tax/subsidy is $3

Oi Consumers will see a larger change in price than producers.

O, There is not enough information to determine the elasticity of demand.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 15) PA P3 $ P₂ P₁ 0 FIGURE 18-3 OE D E: A 93 B 92 Quantity 9/₁1 Demand Refer to Figure 18-3. Suppose that supply is perfectly elastic and the price of this good is initially in equilibrium at P1. If an excise tax raises the price from P1 to P2, the excess burden of the tax is area 15) A) P3AP4. B) P1FBP2. C) P1CBP2. D) BFC. E) P2BP3.arrow_forwardR C *F5 % Refer to Table 7-11. Both the demand curve and the supply curve are straight lines. At equilibrium, total surplus is O a. $72. O b. $56. OC. $44. O d. $96. 5 团 Price (Dollars per unit) 12.00 10.00 8.00 6.00 4.00 2.00 0.00 F6 F7 Y & Quantity Demanded Quantity Supplied (Units) 0 3 6 9 12 15 -18 Table 7-11 F8 * 8 ů F9 09 9 JUL F10 (Units) 36 30 24 18 12 6 O 0 ☀- F11 *+ F12 PrtScarrow_forwardSuppose a market has a downward sloping demand curve and a perfectly inelastic supply curve. The government wants to increase consumer surplus, which of the following policies could achieve this? O A minimum price A subsidy on purchases in the market A maximum price A tax on purchases in the market More than one of the abovearrow_forward

- i will 10 upvotes fastarrow_forwardTyped plz and Asap thanksarrow_forwardThe Market: SUVS (sports utility vehicles) The Market price: $50,000. The Scenario: A tax of $2,000 is placed on the producers of each new SUV produced because they block visibility for others on the freeway. Assume a standard upward-sloping supply and downward-sloping demand in this market. What price do you expect after this tax of $2.000 is placed on SUV producers in this market? O Between $50,000 and $52.000. O Less than $50,000. $52,000 exactly. $50,000 exactly. O More than $52,000.arrow_forward

- QUESTION 2 Andrea is willing to pay a maximum of $1000 for a 50 inches television. She was able to order the television online and earned a consumer surplus of 300. How much she would have paid for that TV? O a. $1,300. O b.$700. O. $300. O d. $1,000. QUESTION 3 In normal circumstances if the government doubles the tax on a product then the resulting deadweight loss will be O a. four times the previous deadweight loss. O b. double of the previous deadweight loss. O c. equals to the previous deadweight loss. O d. less than previous deadweight loss.arrow_forwardYour state legislature is considering increasing the sales tax on two different commodities: prescription drugs and restaurant meals. You estimate owm-price elasticity of demand for prescription drugs Lo be -0.08 and uwn-price elasticity of dermard for reslaurant meals lo be -0.95. If the legislaturc's primary gnal in incrcasing taxcs is to raiscmoncy most efficiontly (i.c., minimizing the resulting deadweight loss), it should tax bullıdrugs and restaurant meals equally. drugs bccausc domand is morc pricc inclastic. reslaurant meals Lecause lhey are nol a rnecessily. only thosc prescription drugs that arc not lifc saving. restaurant meals because demand is more price elastic.arrow_forwardConsider a market in which supply and demand are both unit elastic at the equilibrium (equals 1 in absolute value). Which of the following statements is true? a. Consumer and producer surplus are equal. O b. None of the other answers are correct. O c. Consumer surplus is larger than producer surplus. O d. Producer surplus is larger than consumer surplus.arrow_forward

- Air fares are generally lower on Tuesdays and Wednesdays each week. What is a likely explanation for this occurrence? O Supply is relatively variable, and lower demand on these days leads to a lower equilibrium price. O Demand is relatively variable, and lower supply leads to a lower equilibrium price. Lower levels of both supply and demand on these days lead to a lower equilibrium price. Supply is relatively fixed, and lower demand on these days leads to a lower equilibrium price. Demand is relatively fixed, and lower supply leads to a lower equilibrium price. OOarrow_forwardWhen the price elasticity of demand for a good equals: O a. 1, the demand curve is horizontal. O b. 0, the demand curve is horizontal. O . 0, the demand curve is vertical. O d. 1, the demand curve is vertical. If the government of a country determines a very low minimum wage it will lead to O a. More number of employed people but with poor standard of living O b. Export of goods O c. More number of unemployed people with better standard of living O d. None of thesearrow_forwardPrice $60 40 20 0 50 100 Quantity 150 O $60, resulting in a surplus of 100 units. O $60, resulting in a shortage of 100 units. $40, resulting in equilibrium. O $20, resulting in a shortage of 100 units. 200 Supply Demand Refer to the above diagram. A price floor could be established at:arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education