ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

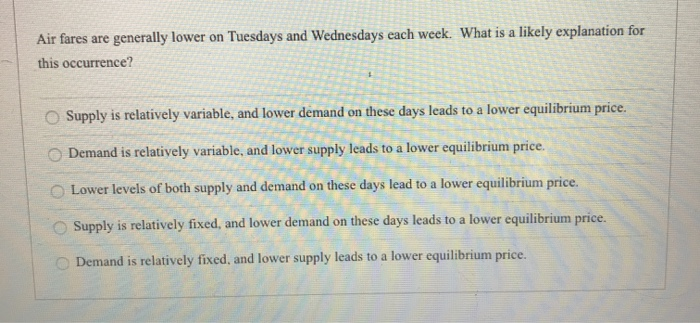

Transcribed Image Text:Air fares are generally lower on Tuesdays and Wednesdays each week. What is a likely explanation for

this occurrence?

O Supply is relatively variable, and lower demand on these days leads to a lower equilibrium price.

O Demand is relatively variable, and lower supply leads to a lower equilibrium price.

Lower levels of both supply and demand on these days lead to a lower equilibrium price.

Supply is relatively fixed, and lower demand on these days leads to a lower equilibrium price.

Demand is relatively fixed, and lower supply leads to a lower equilibrium price.

OO

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose an economic boom causes incomes to increase and, at the same time, drives up wages for the sales representatives who work for cell phone companies. Assume that smartphones are a normal good. This will cause the: O price of cell phones and the equilibrium quantity to rise. O price of cell phones to rise, but the change in the equilibrium quantity is unclear and depends on whether the shift in demand is larger or smaller than the shift in supply. O price of cell phones and the equilibrium quantity to fall. O quantity of cell phones to rise, but the change in the equilibrium price is unclear and depends on whether the shift in demand is larger or smaller than the shift in supply.arrow_forwardThe graph shows the market for concert tickets. Draw a horizontal line at a price at which there is a shortage of concert tickets. Label it Price. Draw an arrow that shows the amount of the shortage. When does a shortage occur? How does the price change to reach equilibrium? A shortage occurs at a given price when The price to reach equilibrium. O A. supply is greater than demand; falls B. the quantity demanded is greater than the quantity supplied; rises OC. demand is greater than supply, rises OD. the quantity supplied is greater than the quantity demanded; falls 600- 500- 400- 300- 200 100- 10- 0 Price (dollars per ticket) Quantity (millions of concert tickets per year) D (6,100) >>> Draw only the objects specified in the question. L Carrow_forwardSeveral advertisements announce that the price of hand sanitizer will be decreasing next month. At the same time, the price of rubbing alcohol, an ingredient used to make hand sanitizer has decreased. Given these two effects, what can we say about the current equilibrium price and quantity of hand sanitizer? → a. Equilibrium price will increase, equilibrium quantity will decrease. O b. Equilibrium quantity will decrease; the effect on price is ambiguous. O c. Equilibrium quantity will increase; the effect on price is ambiguous. O d. Equilibrium price will decrease; the effect on quantity is ambiguous.arrow_forward

- Can you please check my workarrow_forward27arrow_forwardWhy is the supply curve upward sloping for a particular good? Higher prices of the good make the good less profitable O Higher prices of the good incentivize firms to produce more of the good Higher prices of the good increase wages Higher prices of the good increase the demand for the goodarrow_forward

- The price of cereal, a complement good, has decreased. At the same time, a new and improved pasteurization process makes milk production more efficient. Given these two effects, what can we say about the equilibrium price and quantity of milk? O Equilibrium quantity will increase; the effect on price is ambiguous. Equilibrium price will increase; the effect on quantity is ambiguous. O Equilibrium price will decrease; the effect on quantity is ambiguous. O Equilibrium quantity will decrease, equilibrium price will increase.arrow_forwardRespond to the following matching statements with regard to the definition of supply. Match 1: The claim that other things being equal, the quantity supplied of a good increase when the price of that good rises. This matches the Law of Supply. Match 2: A graphical object showing the relationship between the price of a good and the amount that sellers are willing and able to supply at various prices. This matches the Supply curve. O Both matches are false O Match 2 is correct and Match 1 is false. O Both matches are correct. O Match 1 is correct and Match 2 is false. Next 1 Previousarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education