ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

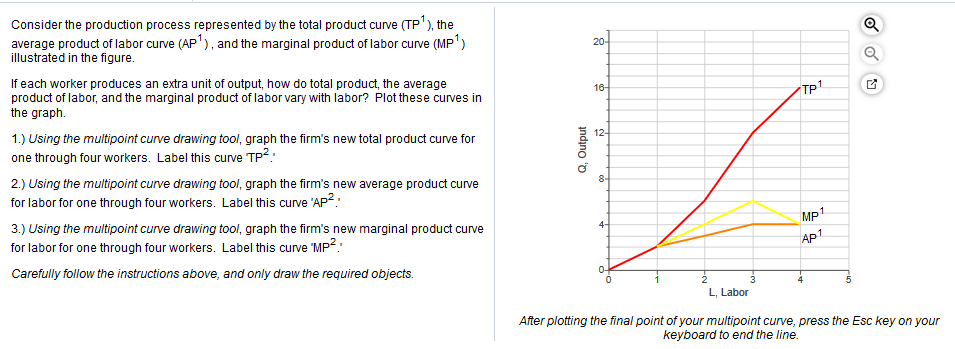

Transcribed Image Text:Consider the production process represented by the total product curve (TP'), the

average product of labor curve (AP'), and the marginal product of labor curve (MP')

illustrated in the figure.

20-

If each worker produces an extra unit of output, how do total product, the average

16-

TP1

product of labor, and the marginal product of labor vary with labor? Plot these curves in

the graph.

12-

1.) Using the multipoint curve drawing tool, graph the firm's new total product curve for

one through four workers. Label this curve TP2:

2.) Using the multipoint curve drawing tool, graph the firm's new average product curve

8-

for labor for one through four workers, Label this curve 'AP2:

MP1

4-

3.) Using the multipoint curve drawing tool, graph the firm's new marginal product curve

for labor for one through four workers. Label this curve 'MP.

AP1

Carefully follow the instructions above, and only draw the required objects.

0-

L, Labor

After plotting the final point of your multipoint curve, press the Esc key on your

keyboard to end the line.

Q, Output

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 3 images

Knowledge Booster

Similar questions

- Question 24 Consider the following production function when K is fixed. (This is a description of the figure: it shows a two-axis graph; in the horizontal axis we measure labor and in the vertical axis we measure output, in this case articles as in the production function of a newspaper; the graph of the production function, for the given level of capital K fixed, is composed of two line segments; the first goes from the origin to the point (10,30); the second, starting from 10 on, is a horizontal line; it is also shown that the production for five units of labor is 15). Can we say that the production function satisfies the law of decreasing marginal returns of labor?True Falsearrow_forward5. The following diagram displays isoquants for different combinations of labor and capital. To ensure that the production function is depicted correctly, provide the values for Q₁, Q2 and 23 on the graph so that the production displays (a) increasing returns to scale, (b) decreasing returns to scale, (c) constant returns to scale. Capital (K)| 1,000 100 10 0 10 100 Q₁ = 1,000 Q₂ Q35 Labor (L)arrow_forwardFor each of the following terms, provide a definition, a description of how this line looks on a graph, and any significant relationships between the term in question and other terms on this list. (If A is related to B, you only need to discuss the relationship once!) Average Product of Labor Marginal Product of Labor Average Variable Cost Average Fixed Cost Average Total Cost Marginal Costarrow_forward

- Let S represent the amount of steel produced (in tons). Steel production is related to the amount of labor used () and the amount of capital used () by the following function: S- 20 L0 C0.7 In this formula L represents the units of labor input and Cthe units of capital input. Each unit of labor costs $50, and each unit of capital costs $100. (a) Formulate an optimization problem that will determine how much labor and capital are needed in order to produce 50,000 tons of steel at minimum cost. If your answer is zere, enter "p" Min 40 120 s.t. 20 S0000 (b) Solve the optimization problem you formulated in part a. Hint: When using Excel Solver, start with an initial >oand C0 Do not round intermediate calculations. Round your answers to the nearest whole number 2991 2318 Cost S 397448 ide Feedbackarrow_forwardGiven the number of labor and the total product in the following table, 1- find the average product (APL) and marginal product (MPL) of labor. 2- Draw Total product (TP), average product (AP) and marginal product (MP) of labor curvesarrow_forwardI need all parts of the question answered, thank you.arrow_forward

- /arrow_forward5. A company that produces auto parts has a production function of Q = 300 L-75 K-5. %3D If L= 250 and K= 25, what is the output of auto parts? If L increases to 350, what is the output of auto parts? What does the change in output show regarding labor as a factor of production?arrow_forward13. Suppose you have a production technology given by f(x1, x2) = min{2x₁, x2} and you are producing at the point where x₁ = 10 and x₂ = 20. (a) Explain in words what we mean (generally) by the ‘marginal product' of an input in production. (b) For the production technology in this question and the initial point x₁ = 10 and x2 = 20, what is the marginal product of a small increase in input 1? (c) Suppose input 2 increases and you are now at the initial point x₁ = 10 and x2 = 30. Relative to your answer in part (b), does the marginal product of input 1 decrease, increase, or stay constant? Explain briefly.arrow_forward

- Assume instead that pharmacists and robots dispense prescriptions according to the following production function: Y = 10*KO.8L0.2 where Y is the number of prescriptions dispensed; L is the number pharmacist hours, and K is the number of robot hours. In addition, $10 worth of materials is used for each prescription. a. What is this type of production function called, and what are we assuming about the relationship between robots and pharmacists by using this production function? b. Derive the cost - minimizing demands for K and L as a function of output, the wage rate and the rental rate of capital. c. Use these results to derive the total cost function: costs as a function of y, r, w, and the $10 materials cost. d. Pharmacists earn $32 per hour. The rental rate for robots is $64 per hour. What are total costs as a function of Y? e. Does this technology exhibit decreasing, constant, or increasing returns to scale?f. The pharmacy plans to produce 40,000 prescriptions per week. At the…arrow_forwardQUESTION 1 For the production function Qs = K0.6L0.7 find the returns to scale, recall that a doubling of inputs that doulbes output is a CONSTANT returns to scale = 1.0 Please enter your response as a positive number with 1 decimal and 5/4 rounding (e.g. 1.15 = 1.2, 1.14 = 1.1).arrow_forwardd. Calculate the marginal product of capital MPK. e. Calculate the marginal product of labor (MPL).arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education