ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

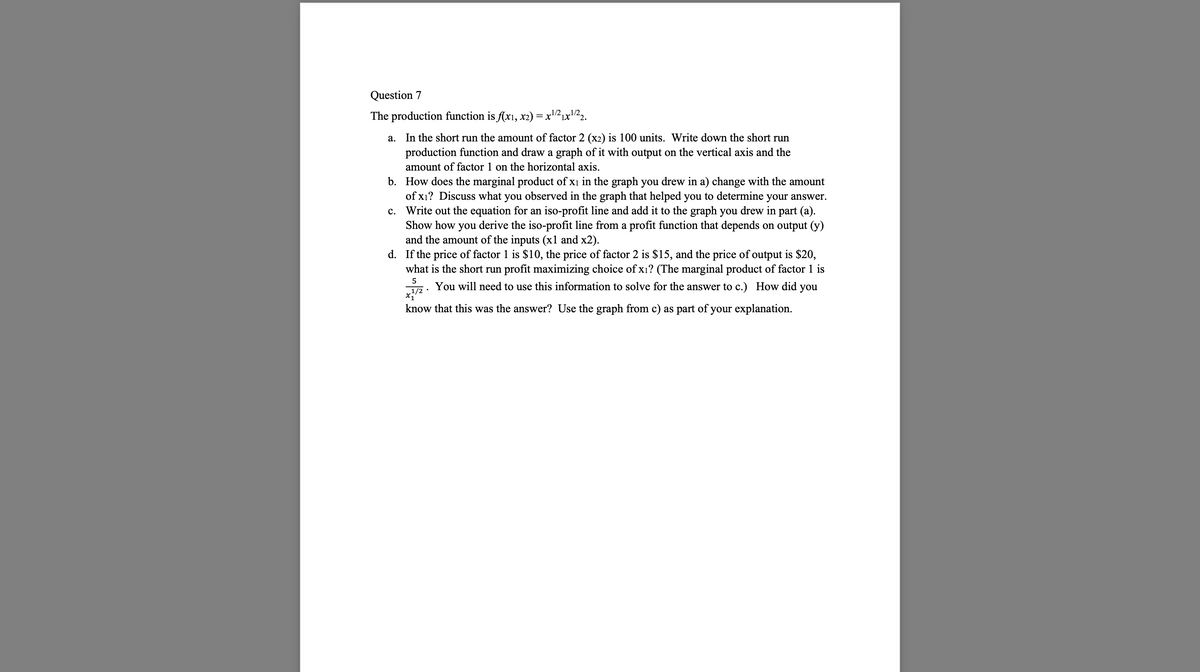

Transcribed Image Text:Question 7

The production function is f(x1, x2) = x¹/²₁x¹/22.

1X

a.

In the short run the amount of factor 2 (x2) is 100 units. Write down the short run

production function and draw a graph of it with output on the vertical axis and the

amount of factor 1 on the horizontal axis.

b. How does the marginal product of x1 in the graph you drew in a) change with the amount

of x₁? Discuss what you observed in the graph that helped you to determine your answer.

Write out the equation for an iso-profit line and add it to the graph you drew in part (a).

Show how you derive the iso-profit line from a profit function that depends on output (y)

and the amount of the inputs (x1 and x2).

d. If the price of factor 1 is $10, the price of factor 2 is $15, and the price of output is $20,

what is the short run profit maximizing choice of x₁? (The marginal product of factor 1 is

5

1/2

You will need to use this information to solve for the answer to c.) How did you

know that this was the answer? Use the graph from c) as part of your explanation.

C.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 13. Suppose you have a production technology given by f(x1, x2) = min{2x₁, x2} and you are producing at the point where x₁ = 10 and x₂ = 20. (a) Explain in words what we mean (generally) by the ‘marginal product' of an input in production. (b) For the production technology in this question and the initial point x₁ = 10 and x2 = 20, what is the marginal product of a small increase in input 1? (c) Suppose input 2 increases and you are now at the initial point x₁ = 10 and x2 = 30. Relative to your answer in part (b), does the marginal product of input 1 decrease, increase, or stay constant? Explain briefly.arrow_forwardProduction Total Product Total Fixed Cost Total variable cost Total Cost Average fixed cost Average variable cost Average Total Cost Marginal Cost 0 0 1 25 2 45 3 60 4 70 5 85 6 105 7 135 8 180 9 240 10 315 Assume that fixed costs are $50, labor is the only variable input and its costs are reflected completely in the costs above. Complete the table Graph AFC, AVC, ATC, and MC Explain how increasing returns and decreasing returns are depicted in your graph If the labor input increased by $10 at every unit of production, what would be the effect on your graphs?arrow_forwardI have graphed the isoquant line but I can’t figure out how to graph the isocost line? Could you verify my math and show the isoquant and isocost line graphed please?arrow_forward

- Grease Tech produces oil changes. The production of oil changes reles on both capital (K) and labor (L) and is combined in the following production function F (K, L) = KILL Take the derivative of this production function with respect to capital. What is the marginal product of capital evaluated at (le. just plug in the numbers) 64 units of capital used and 16 units of labor?arrow_forwardSubpart 4arrow_forwardCould you please help me with this question? Thank you!arrow_forward

- GM cuts jobs at its Australian manufacturing unit GM will cut 500 jobs, or about 12% of its workforce, at its Australian plant because of a sharp fall in demand for its locally-made "Cruze" small car. Source: The Wall Street Journal, April 8, 2013 As GM cuts its workforce, how will the marginal product and average product of a worker change in the short run? Suppose that before the cuts the marginal product of GM workers is below their average product. As the number of workers decreases, the marginal product of a GM worker and the average product of a GM worker in the short run. increases; decreases does not change; does not change decreases; decreases increases; increases decreases; increasesarrow_forwardanswer question d Q5. Jason is running a cleaning business, there are available labours (L) and machines (M) for Jason to use as inputs to produce cleaning service for his clients. a) Suppose Jason must use both labours and machines without any specific ratio to complete the service for his clients, please write down the general production function formula for Jason. hint: you could use any letter if you want] b) Under the function form of a), assume Jason's Marginal Rate of Technical Substitution (MRTSL, M) equals to 2, how do you interpret it? c) Assume Jason now can use only single input, either labour or machine to complete the service, please write down the general production function formula for Jason. hint: you could use any letter if you want] d) Under the function form of c), assume Jason's Marginal Rate of Technical Substitution (MRTSL, M) is always larger than the market price ratio between labour and machine (w/r), what should Jason do? why?arrow_forward6arrow_forward

- Sandwiches, a sandwich shop, has the following marginal product curve (labelled MP) for its hourly productions hourly production.arrow_forward2. Consider a Cobb-Douglas production function with three inputs. K is capital (the number of machines), L is labor (the number of workers), and H is human capital (the number of college degrees among the workers). The production function Y = K2/6 L3/6 H1/6 a) Derive an expression for the marginal product of labor. How does an increase in the amount of human capital affect the marginal product of labor? (Hint: The marginal product of labor MPL is found by differentiating the production function (Y) with respect to labor (L)) b) Derive an expression for the marginal product of capital. How does an increase in the amount of human capital affect the marginal product of capital? (Hint: The marginal product of capital MPK is found by differentiating the production function (Y) with respect to capital (K)).arrow_forward1. Suppose the production function is Q = 8L + 15K where Q is the quantity of output, L is the quantity of labor used in production, and K is the quantity of capital used in production. What can be said about this production function? It has Decreasing Returns to Scale It has Constant Returns to Scale It has Increasing Returns to Scale There isn’t enough information to determine the Returns to Scale for this production function 2. You’re dreaming of what to do during a nice summer day. You could mow the lawn which you would pay someone $15 to do for you. You could go for a walk which you value at $11. You could also take a nap and ignore everyone and everything else which you would pay $29 to do. If you to take a nap, what is your opportunity cost? Group of answer choices $29 $26 $15 $11arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education